2:25 pm

SPX has now fallen beneath the Cycle Top, the Diagonal trendline and short-term support at 4961.00, giving a sell signal.

815 am I am leaving on a tour until the end of March. I may only have limited time, if any, to write this blog until April.

Good Morning!

NDX futures declined to 17427.00 this morning and are hovering near their lows. NDX is on a sell signal with several supports left beneath it. The first is Intermediate support at 17251.87, which confirms the sell. The 50-day Moving Average is at 16995.70 where most analysts would agree that the move is bearish. The Cycles Model suggests the decline may last until the end of February, with a possible 4-day extension into the first week of March. Volatility may pick up over the weekend with the largest moves starting next week. All eyes are on Nvidia this morning.

Today’s options chain shows Maximum Investor Pain at 17600.00. Long gamma picks up at 17650.00 while short gamma begins with a bang at 17580.00. Any negative news may put short gamma into play.

SPX futures morning low was 4959.80, hovering above yesterday’s low at 4955.00 where the CycleTop support and 4-month trendline lay. Beneath 4955.00 is a sell signal for SPX. The Cycles Model implies that the Master Cycle low may come at the end of February. However, outside forces may extend the low into the first week of March.

Today’s op-ex shows Max Pain at 4985.00. Long gamma may begin at 5000.00, but short gamma starts at 4975.00.

ZeroHedge reports, “US futures extended their slide, bucking a strong Asian session with European stocks mixed, ahead of what Goldman trader Scott Rubner called “the most important stock on planet earth” – that would be Nvidia for anyone who has been living in a cave the past year – reports after the close facing sky-high expectations, and where another Goldman trader, Peter Callahan, said that the tactical debate is whether this print will be a local top or a ‘break-out’ moment for the stock and for the AI trade (from where he sits, this “feels like consensus is learning more towards the former“). And with options implying the stock may move about 11% in either direction, i.e., a whopping $200BN in market cap may be gained or lost for a company that recently surpassed GOOGL and AMZN in market cap, it’s not surprising why the market is on edge. With that preamble out of the way, S&P 500 futures dropped 0.2% as of 7:40am and Nasdaq contracts lost about 0.5%, suggesting Wall Street may be in for a third day of declines. Bond yields are lower, the 10Y dropping 2bps, with steepening across most of the curve; the USD is flat and commodities are weaker. The macro data focus is on Fed Minutes this afternoon; while possible to see a dovish surprise regarding QT this most likely comes at the March 20 Fed meeting where we may see a reduction in the pace of QT.”

VIX futures shot up to 16.12, above yesterday’s high. The Cycles Model shows rising trending strength going into the weekend. The Master Cycle high in VIX may be anticipated in the first week of March. This may very well be a slingshot move beyond market expectations.

Today’s op-ex shows Max Pain near 15.00. Short gamma runs from 13.00 to 15.00. Long gamma starts with a bang at 16.00 and runs hot to 40.00.

TNX eased down to 42.60 (futures to 42.51) this morning. The Cycles Model suggest trending strength may prevail through the end of the week.

ZeroHedge pithily remarks, “…

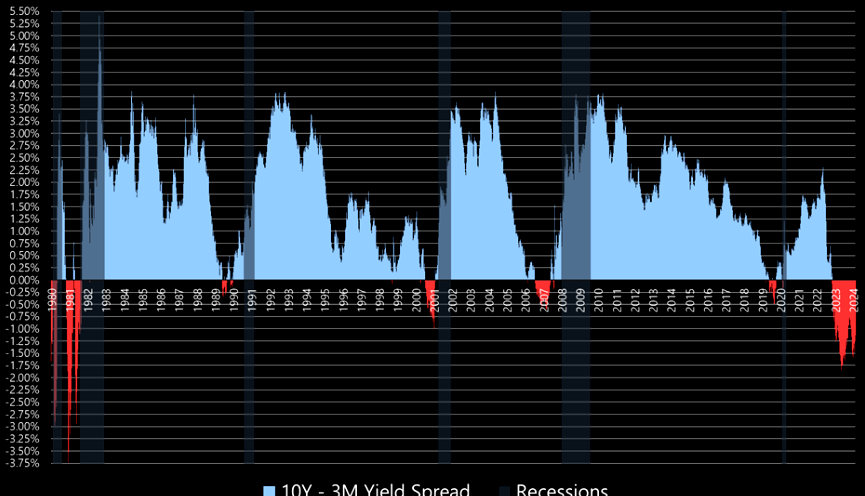

Source: Jefferies

The worst average equity performance occurs when the 10Y-3M yield spread is negative and rising – as it is now. What is going on here? Either the bond market expects a recession or the bond market expects more inflation. Neither one seems to be what equities are suggesting.”

The Shanghai Composite Index rose to a high of 2994.61 today, on its way to the mid-Cycle resistance at 3081.81. The current Master Cycle has two more weeks left to termination. Whether it exceeds its target is still to be determined.

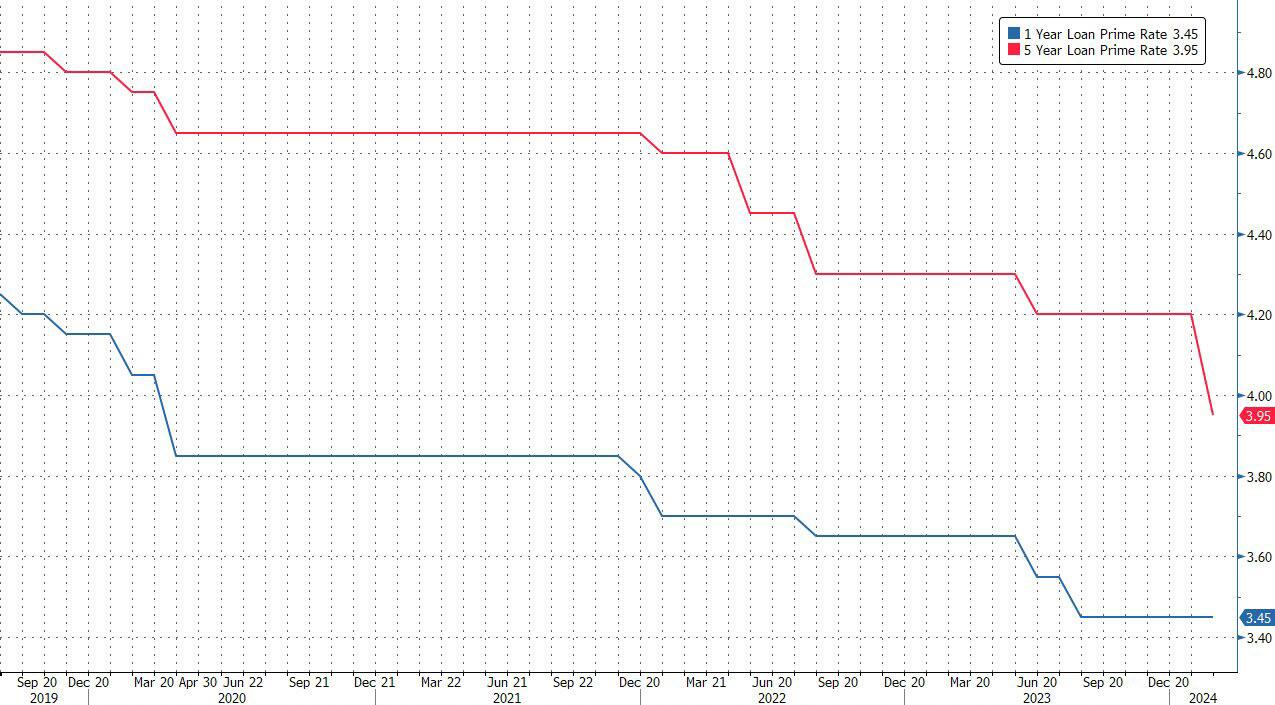

Zerohedge observes, “After the relentless jawboning in recent days, many were expecting some further easing today from the PBOC, and Beijing did not disappoint when China cut the 5-year loan prime rate (LPR) – which influences mortgage rate pricing – and is also known as China’s Libor (or rather SOFR since Libor no longer exists) by 25bp to to 3.95% on Tuesday, while holding the 1-year rate at 3.45%. The LPR cut is the largest since China revamped its loan pricing mechanism in 2019. China last trimmed the 5y LPR by 10bp in June 2023.”