8:00 am

Good Morning!

NDX futures rose to 17862.50 in the overnight session, a 68% retracement. Today is a make-or-break day, as the direction of the market from here may dictate the tone of the outlook for the year. The Cycle Top support is at 17530.00, beneath which we find an aggressive sell signal.

Today’s options Chain shows Maximum Investor Pain at 17690.00 Long gamma begins at 17700.00 and is heavily weighed while short gamma begins at 17600.00. Investors are chasing the bull through the options market.

ZeroHedge remarks, “3rd spot secured

The day after surpassing the market value of Amazon, the chip giant has now overtaken Alphabet as well.

Source: Bloomberg

NVDA coming for the number 1 spot

1. NVDA would need to hit ~$1,150 to surpass Apple in market cap.

2. It would need to hit ~$1230 to surpass MSFT and take over as the largest stock in the world.

3. NVDA is currently 60% above its 200-day moving average. If it would reach the same level of overbought that TSLA reached in end 2020/early 2021 of 120% above it would be the largest company in the world.”

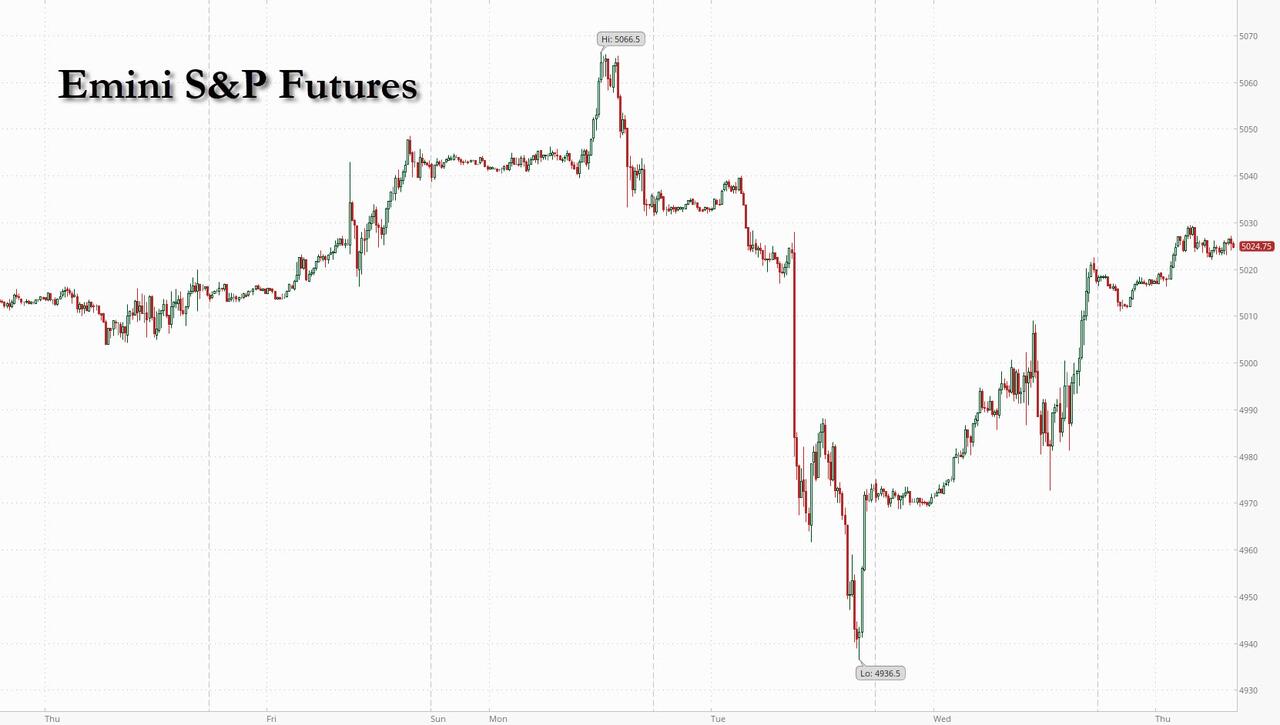

SPX futures have risen to 5014.40, a 73% retracement, but has not been able to fill the gap left on Tuesday at 5021.84. Sentiment is riding high as “blue sky” beckons retail investors after 15 weeks of (nearly) unbroken rally. Has it gone too far? Those who know the history of the market claim the stock market is skating on very thin ice. The Cycle Top support and Diagonal trendline lie at 4932.80, beneath which we find an aggressive sell signal. The Sell signal is confirmed beneath Intermediate support and the 1987 trendline at 4932.80.

Today’s op-ex shows Max Pain at 4980.00-4985.00. Long gamma kicks in above 5000.00. Short gamma reigns beneath 4975.00.

ZeroHedge reports, “Tuesday’s post-hot CPI dump now seems like a distant bad dream as US equity futures continued their rebound, following a tech fueled rally on Wednesday that drove the S&P 500 back above 5,000. As of 8:05am, S&P 500 futures were up 0.1%, also approaching pre-CPI levels; Nasdaq futures were as usual even stronger, rising 0.2% Europe’s Stoxx 600 index surged to the highest in more than a month. WTI crude oil futures are down 0.8% on heels of 1.6% drop Wednesday, following a bearish report by the IEA which predicts lower demand growth than supply growth in 2024. Today’s macro focus is on Retail Sales and Jobless data amid the barrage of data which includes import/export price indexes, Empire State manufacturing and Philadelphia Fed business outlook surveys, January industrial production, December business inventories, February NAHB housing market index and December TIC flows. A weaker print in retail sales – which our preview suggested is coming – and claims may continue the rally in bonds, potentially pushing the Equity rotation that began last week (paused with CPI) farther. There are also three Fed speakers today.”

VIX futures did not exceed yesterday’s low, but consolidated beneath the mid-Cycle resistance at 14.89.

Next Wednesday’s op-ex show that virtually all of the short gamma has rolled of in yesterday’s expiration. Long gamma starts at 14.00 and remains strong to 40.00.

ZeroHedge comments, “VIX seasonality

We are just at the point in time in the calendar when VIX tends to spike.

Source: Equity Clock

Just in time

Second half of February is bad for stocks.”

TNX has pulled back to test support at the mid-Cycle line at 41.82. It may seek the 200-day Moving Average at 41.32 or possibly the trendline at 41.00 to complete the correction in the next day or two. The Cycles Model suggests a resurgence of trending strength may arrive early next week. TNX is on a buy signal and this pullback offers a “buy the dip” opportunity.

USD futures have declined to a low of 104.22 as it corrects the most resent probe higher. The correction may only last to the weekend, as trending strength comes back to the USD next week.