1:41 pm

BKX, our liquidity proxy, is hovering at the 50-day Moving Average at 92.97, waiting for the trigger to be pulled. The resumption of the decline may be unstoppable. The banking system as we know it may be totally changed in a mater of months. Individuals can prepare by having cash on hand as the banking pressures rise. The problems from last March were not solved, They were simply postponed.

ZeroHedge remarks, “Don’t look now, but it seems that the regional banking crisis is beginning to reemerge after almost a year of hibernation.

Last February brought with it the failure of Silicon Valley Bank, First Regional and Signature Bank. At the time, the crisis was quickly spreading and the Fed was forced to step in with an emergency facility known as the Bank Term Funding Program (BTFP), which allowed banks to turn in underwater treasuries in return for cash equivalent to the par value of the treasuries at a very low interest rate. The BTFP is structured as a 1-year loan and Jerome Powell and company announced that they will not be extending the BTFP due to the fact that banks were taking the cash and dumping it into higher yielding facilities at the Fed to take advantage of an arbitrage opportunity that the BTFP opened up, which hindered the Fed’s balance sheet.”

8:00 am

Good Morning!

NDX futures have eased down from their new all-time high at 17784.17, to a morning low at 17719.50. Critical support lies at 17374.13, where an aggressive sell signal may be made. A confirmed sell signal lies beneath the Ending Diagonal trendline and Intermediate support at 17025.30. The Cycles Model infers a decline in the making to the end of February or early March. Meanwhile, sentiment is euphoric as stocks may be about tomake gains 14 out of 15 past weeks.

Today’s options chain shows Maximum Investor Pain at 17800.00. Long gamma is sparse, but short gamma begins at 17790.00.

ZeroHedge remarks, “The equity world is wonderful right now, but sometimes even winners need to pause. We do believe equities will be lower over the next few weeks. Miss Market might even teach us a masterclass in humility. Here are the reasons why.”

SPX futures are consolidating beneath their new high made yesterday. Today is day 34 (a Fibonacci unit) from the January low. The bullish structure is all but complete. Critical support lies at the Cycle Top at 4891.39. Equities are out on a limb that may snap at any time.

Today’s op-ex shows Max Pain at 4965.00. While long gamma may begin at 4975.00, short gamma resides beneath 4950.00.

ZeroHedge reports, “US equity futures dropped on Thursday after hitting a fresh all time high in the previous session, and bond yields rose as investors analyze a slew of earnings reports and also prepared for the sale of 30Y treassuries. As of 8:00am ET, S&P futures were down 0.2%, but even with the decline the S&P remains within striking distance of the 5,000 level and a small gain of just 5 points would take it there today. The MSCI World Index of developed-market stocks also rose to a record. The Stoxx 600 traded flat on the busiest day of the European earnings season. The dollar gains after the yen tumbled following dovish comments from BOJ Deputy governor Uchida who said the BOJ won’t aggressively hike rates even after ending negative rates (unclear who expected the BOJ to unleash a hiking spree). Commodities are the standout pre-mkt as the energy complex leads the group higher and strength across metals. It’s another busy day for earnings: the lineup in the US today includes Expedia, Philip Morris, ConocoPhillips, S&P Global and cereal maker Kellanova. On the macro side we get jobless claims and wholesale trade and inventories.”

VIX futures have risen from yesterday’s low at 12.81, which may have been a Master Cycle low at day 259.The two-month low readings in the VIX may offer a surprise in the opposite direction once the new Master Cycle has begun.

The Shanghai Composite Index rallied again today to Intermediate resistance at 2867.47. It is now due for a pullback totest the low. The correction may take up to a month. However, it is unlikely that the Shanghai Index will make new lows at this time.

ZeroHedge notes, “China has appointed capital markets veteran Wu Qing to head the nation’s securities regulator just one day after the country’s sovereign wealth fund said it would ramp up buying shares in the open market amid a three-year rout that has wiped out a staggering $7 trillion in value off stock markets in Hong Kong and China.”

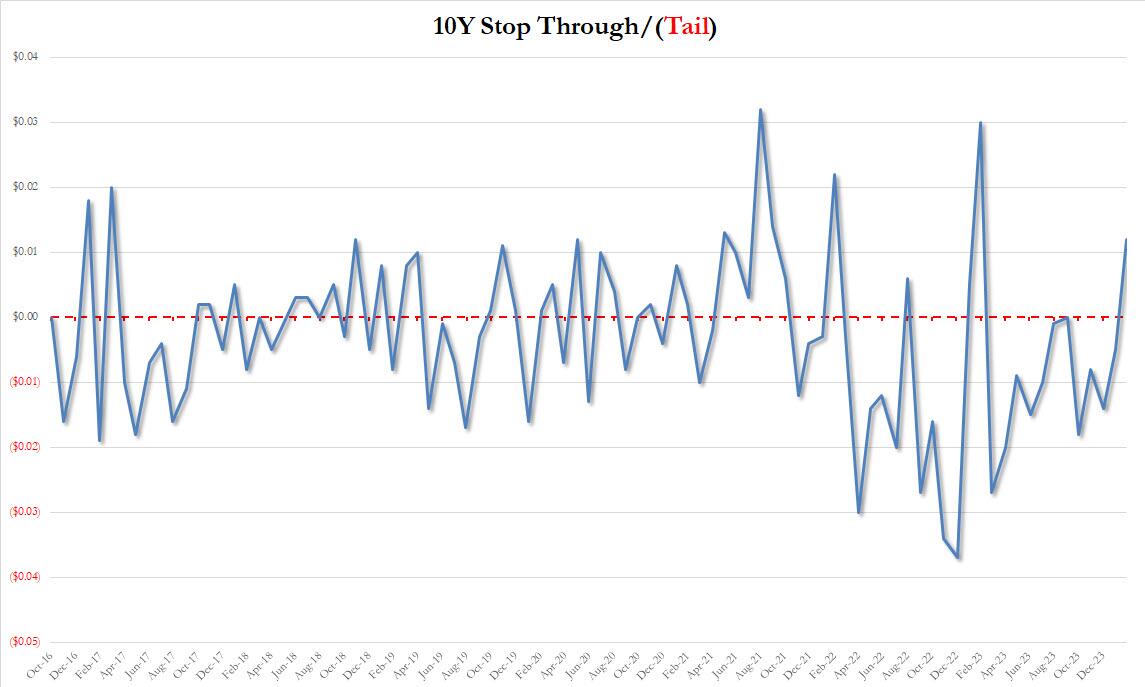

TNX rose to test mid-Cycle resistance at 41.65 this morning. Tension is mounting over the auction of $25 billion of 30-year Bonds this afternoon and the offering of $185 billion in T-bills, despite the blow-out 10-year Note auction yesterday. The Cycles model suggests heightened volatility today, for good reason. The Cycles Model suggests that yields may rise through late April.

ZeroHedge observes, “Today’s 10Y auction was set to make history: the February refunding auction would sell $42BN in debt maturing on Feb 15, 2034, the largest amount ever for a 10 Year auction…

… and after yesterday’s mediocre 3Y refunding, there were some concerns that the sheer size of today’s issuance could lead to severe market indigestion.”