9:47 am

BKX remains on a confirmed sell signal as it hovers above the 50-day Moving Average at 92.26. Beneath that level is a commonly recognized sell signal. The Cycles Model suggests the decline may continue through the end of February with volatility/;intensity picking up this weekend.

ZeroHedge observes, “After two weeks of outflows, money market funds saw $42BN of inflows last week, sending the total assets above $6TN for the first time ever..

Source: Bloomberg

Not exactly a bullish sign for stocks as investors are choosing super safe money markets, where six-month bills yield about 5.17%, as the Fed sticks to its higher-for-longer policy.”

7:30 am

Please note: February 20 may be the last day of this blog until the end of March. I will be on an extended trip during that time, with very limited access to the internet. I have not yet determined my commitment to the blog after April 1. Suffice it to say that it will be in God’s hands.

Good Morning!

NDX futures made a weekend low of 17571.60, well above the Cycle Top support at 17294.69, where an aggressive sell signal may be had. Further confirmation lies at the trendline and Intermediate support at 16935.60, where a confirmed sell signal awaits. Today may be a half-Trading Cycle high followed by a half-0Trading Cycle (approximately 30 days) decline. The Strength of the decline may determine whether stocks move on to greater highs. The 1987 trendline may hold the answer.

Today’s options chain shows no Max Pain, no long gamma. Short gamma begins at 17700.00. Remember that the NDX is the domain for institutional investors.

ZeroHedge remarks, “Price

US money market fund assets hit a record high of $6trln this week. Gov’t debt hit record highs too. As did US equities, in general. Gold is near a record, US home prices too. In a highly financialized fiat monetary system, many drivers work to influence valuations. Cash flows, earnings, leverage, interest rates, money supply, its velocity, tax rates, optimism, pessimism, uncertainty, confidence, stability, volatility, and expectations about how all such things will change. Investors search for fair market value, but for a trader there’s no such thing, only price.”

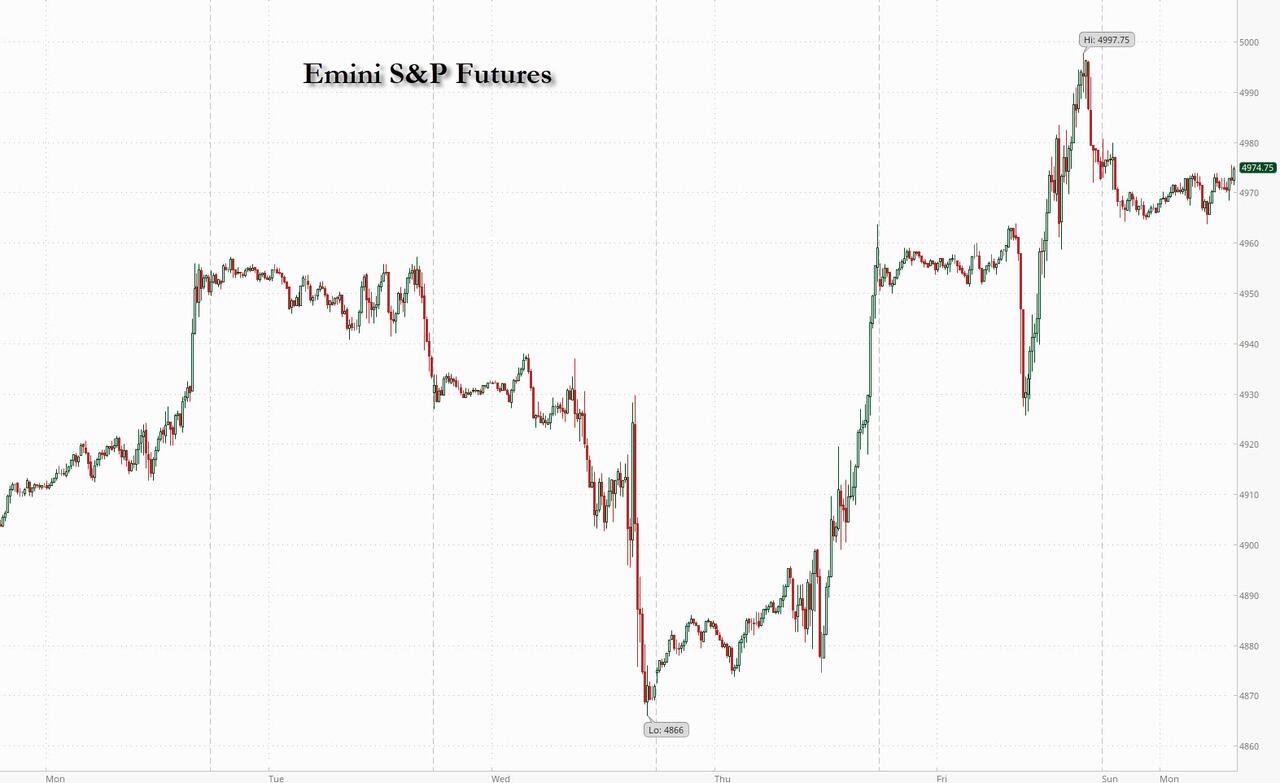

SPX futures declined to 4942.40 over the weekend, but have recovered near the flat line this morning. Just to reiterate, SPX is also at a half-Trading Cycle high. It has to the end of February to prove whether or not it has entered the bear market. The trendline at 4200.00 may offer some insight. The Cycle Top support lies at 4868.03 where an aggressive sell signal may be obtained. The Ending Diagonal trendline and Intermediate support lie at 4794.59 where a confirmed sell signal awaits.

Today’s options chain shows Maximum Investor Pain at 4900.00. Long gamma may begin at 4950.00 while short gamma lies under 4890.00.

ZeroHedge reports, “S equity futures and bonds fell while the dollar rose after Fed Chair Jerome Powell again pushed back against any hopes of lower interest rates during his 60 Minutes interview, saying it’s “not likely” the Fed would cut in March (which was to be expected after Friday’s blowout jobs number). As of 7:40am ET S&P futures dropped 0.1% after closing at an all time high on Friday when they rose as high as 4998. Meanwhile, European shares edged higher, supported by strong earnings from Italian lender UniCredit SpA while Asia closed red after a rollercoaster session in China which first plunged then saw another stabilization bid from the plunge protection team. 10-year Treasury yields climbed nine basis points to 4.11%, extending a move that started after Friday’s blockbuster jobs report as yields on debt from Australia to Germany rose. Meanwhile, the Bloomberg Dollar Index traded near a two-month high and oil and gold prices retreated, and bitcoin reversed a weekend selloff.”

VIX futures surged to 14.44 over the weekend, then pulled back, remaining above 14.00 thus far. It is nearing the end of the current Master Cycle that may happen in a matter of days, if not hours. Should VIX rise above the mid-Cycle resistance, it may follow through to the Cycle Top at 19.44.

Wednesday’s options chain shows Max Pain at 14.00 There is a slug of short gamma at 13.00. Long gamma may begin at 15.00, but only goes to 25.00. This week’s op-ex may offer a clear change in trend that has been lacking until now.

ZeroHedge observes, “The VIX, often referred to as ‘Wall Street’s fear gauge,‘ is currently portraying a sense of calm among investors, registering well below the 20 level.

For those not acquainted, the VIX draws its value from S&P index options with near-term expiration dates, providing a 30-day projection of volatility.

While the VIX isn’t a precision instrument, it serves as a barometer of market sentiment.”

The Shanghai Composite Index undershot its target at 2650.00 to a low of 2635.09 today. It has bounced to 2700.00 where it lies beneath the bottom trendline at 2730.00. Today is day 256 of the Master Cycle, suggesting a few more days of bottoming before a rally takes hold. An aggressive buy signal may be had above the lower trendline at 2730.00.

ZeroHedge observes, “Last week’s dead cat bounce in Chinese stocks – after Beijing did everything but launch a multi-trillion fiscal stimmy bazooka (something it will do, later if not sooner) – is a distant memory, and as Asian markets open for trading in the news week, Chinese markets are cratering with the Shanghai Composite plunging as much as 3.1% to a fresh five-year low..

… while the broader CSI 1,000 Index is also in free-fall and also on pace to re-test the 2018 lows with as many as 990 of the 1000 companies of the index in the red.”

TNX leaped above the trendline at 41.00 to challenge the 200-day Moving Average at 41.04 and the mid-Cycle resistance at 41.55. This is sending alarms to the investment community. TNX may be on a confirmed sell signal. The Cycles Model infers rising rates may dominate until mid-April. Yellen’s lowball estimate of new treasuries coming to the market were DOA as a record $10 billion may hit the market in 2024.

ZeroHedge remarks, “Interest-rate traders have managed to shake off the extreme conviction they had before the start of the year that the Fed would cut rates as soon as March.

Now, they are starting to ponder whether the central bank will have sufficient incentive to loosen policy in May.

While Jerome Powell reiterated his stance that a rate cut in the winter is unlikely in his much-anticipated CBS interview, anchor Scott Pelley remarked that the Fed Chair suggested the first cut could happen in the middle of the year — even though it wasn’t to be found in the transcript of the interview.”

USD futures rose to a new high at 104.28 this morning as it new trend may extend to the end of March.

Crude oil futures are consolidating beneath its Intermediate resistance at 73.57. The Cycles Model suggests that, once the consolidation is finished, it may continue its decline to mid-April. Volatility may pick up this week in oil.

ZeroHedge reports, “One wouldn’t know it from their stock price today, which has been slammed by tech bros shorting anything that does not mention AI at least 100 times in its press release/conference so they can fund their purchase of META 20% higher on the day, but in a time when two-thirds of US companies do not generate any GAAP profits, two of America’s cash flow titans – ExxonMobil and Chevron – reported their second-biggest annual profits in a decade thanks to surging oil production which offset a slide in prices that tempered earnings from the records hit in 2022.

At a time when OPEC+ and Saudi Arabia has been hurting due to a flood of oil by US companies, America’s oil supermajors increased output sharply in their own backyard in 2023, pursuing a strategy of doubling down on oil and gas that has prompted blowback over their commitment to cutting emissions .”

OilPrice.com reports, “Strong buying from China and India at the end of last year pushed Asia’s crude oil imports in January 2024 to the highest level in eight months, data compiled by LSEG Oil Research showed on Thursday.

Crude cargo arrivals in Asia, the prized oil-importing region and the world’s biggest rose to 28.57 million barrels per day (bpd) in January 2024, up from 27.03 million bpd in December 2023, per the data reported by Reuters columnist Clyde Russell. ”