1:42 pm

BKX is making its final probe toward the 61.8% Fibonacci retracement value nine months after its last waterfall event. Today is day 271 from the day of its panic low on May 4, 2023. A new panic event may be about to start imminently. The chart foretells that the banking system as we know it may disappear by the end of the year.

ZeroHedge warns, “Last Thursday, Bloomberg reported that federal regulators are preparing a proposal to force US banks to utilize the Federal Reserve’s discount window in preparation for future bank crises. The aim, notes Katanga Johnson, is to remove the stigma around tapping into this financial lifeline, part of the continuing fallout from the failures of several significant regional banks last year.

This new policy is reminiscent of the Fed’s actions during the 2007 financial crisis, where financial authorities encouraged large banks to tap into the discount window, taking loans directly from the Federal Reserve, to make it easier for distressed banks to do the same. The hesitancy from financial institutions to tap into this source of liquidity is justified. If the public believes a bank needs support from the Fed, it is rational for depositors to flee the bank. The Fed’s explicit aim is to provide cover from at-risk banks, trying to hold off bank runs that are an inherent risk in our modern fractional reserve banking system.”

7:45 am

Good Morning!

NDX futures rose to an overnight high at 17622.70, then pulled back. It has not been able to overtake the January 24 high at 17665.26. I mentioned earlier that the NDX would be the most likely to lead the stock indices down from the high. This may be a good indicator of that possibility. NDX is in throw-over above its Cycle Top at 17215.32 where an aggressive sell signal may await. The Ending Diagonal trendline and Intermediate support lie at 16806.82, beneath which lies a confirmed sell signal. This is a possibly explosive week for the stock indices.

Today’s options chain is upside-down with 120 call contracts at 17525.00 while there are 159 put contracts at 17620.00. Dealers own many of these puts as they take the opposite side of retail investors.

ZeroHedge comments, “Last summer, I was having lunch with a friend at a plain vanilla shop, who kept checking his phone and muttering, “this NVIDIA is killing me.”

After the third time in five minutes, I had to ask:

Me: You run a long-only fund. You don’t short. How is NVIDIA killing you?

Him: Kuppy, you don’t get it. You do your own thing. I’m benchmarked. I’m underweight NVIDIA and trailing massively. There are guys at my firm who are 500bps overweight. One guy is even 700bps overweight. They’re killing it.

Me: Who cares?? Just buy something else.

Him: NVIDIA goes up every day. Clients keep asking about it. I feel like an idiot to be underweight.

Me: So, then why don’t you buy some if it’s worrying you so much?

Him: I keep waiting for a pullback. Damn thing is up another 3% today. It never pulls back. I’m getting further and further behind. Not sure what I’m going to do. NVIDIA is killing my year…”

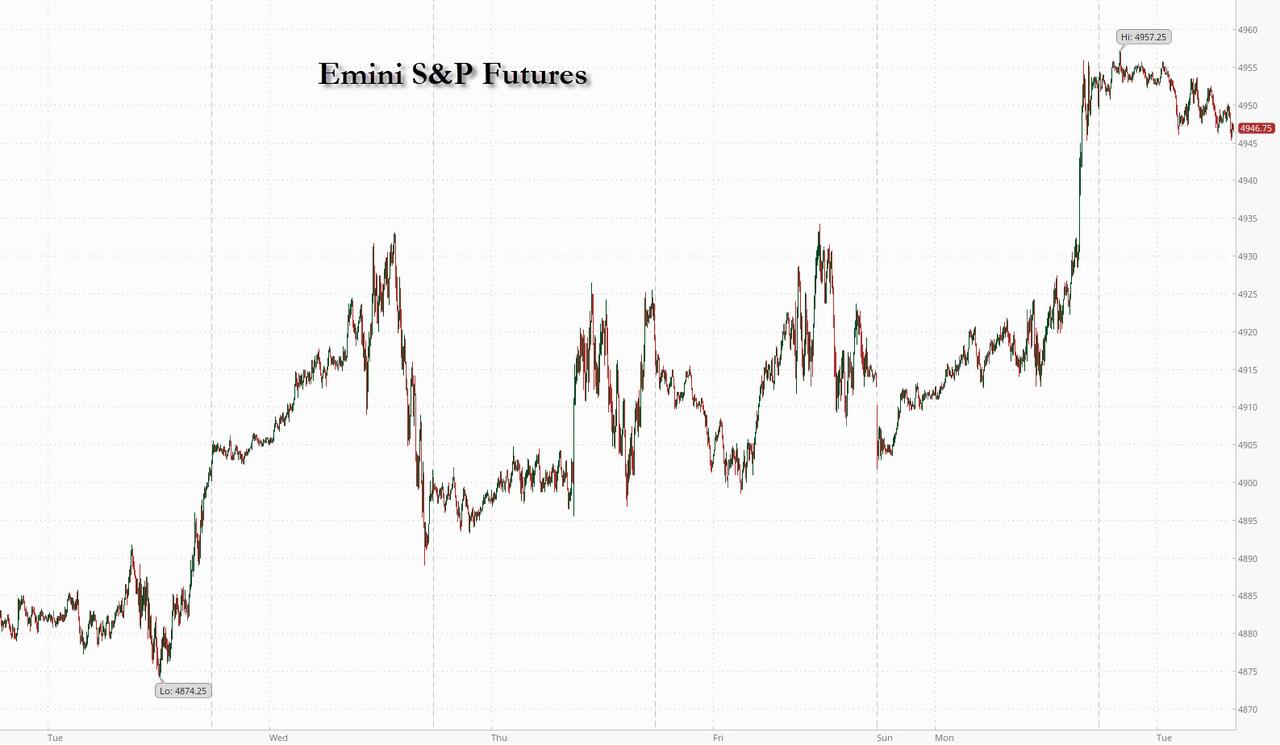

SPX futures reached an overnight high at 4930.70, in a nosebleed high, before pulling back. This rally puts SPX in the 99th percentile for rallies in the first month of the year. Today is day 279 in the current Master Cycle. SPX is in throw-over in both time and price. The Cycle Top support is at 4841.72, beneath which an aggressive sell signal lies. The Ending Diagonal trendline and Intermediate support lie at 4763.48, beneath which lies a confirmed sell signal.

Today’s op-ex shows a highly contested Max Pain level at 4900.00. Above are calls and beneath it puts have the majority.

ZeroHedge reports, “After yesterday’s late day meltup, sparked by an overly optimistic forecast of Treasury supply, which sent stocks to a new all time high, US equity futures drifted lower in a tight range as investors looked ahead to the flood of tech earnings (Alphabet and Microsoft are due after the close) for insights on whether the record-breaking rally in equities can continue, while bracing for key announcements from the Fed and Labor department. Monday’s latest record close pushed the S&P 500’s gains this month to 3.3%, while the Nasdaq 100 has surged 4.6%. Europe’s Stoxx 600 index crept to a new two-year high as autos and banking stocks led gains. Bitcoin is on course to advance for a fifth straight month, after rising 2% in January; The last time the largest digital asset managed a winning streak like this was the October 2020 to March 2021 stretch oiled by pandemic-era easy money. As stocks dropped, both 10Y TSY yields and the US dollar traded largely unchanged. Oil dipped as Biden refuses to retaliate against Iranian proxies, terrified any escalation will send gas prices soaring and crush his reelection chances.”

VIX futures rose to 13.71 after pulling back from a near-breakout at 15.35 yesterday. VIX is on a buy signal as it closed above the 50-day Moving Average at 13.07. There is approximately a week left in the current Master Cycle. There is a strong likelihood that the VIX may power its way up to the Cycle Top at 19.51 by then. It is recognized that the VIX is being suppressed.

Tomorrow’s options chain shows friction among the puts and calls between 13.00 and 14.00. Long gamma begins at 15.00 and becomes earnest from 17.00 to 25.00.

The Shanghai Composite Index reversed back beneath its Cycle Bottom support at 2843.58. Motivated sellers stepped in before the Shanghai Composite could reach the 50-day Moving Average at 2943.33. There is another possible week of decline to reach the next Master Cycle terminus. If so, a possible target may be in the vicinity of 2650.00.

ZeroHedge remarks, “Just local problems?

The China bear is seen as a local problem still. We saw a similar type of reasoning during the 1997 Asian crisis, but local issues went global. Don’t forget that China is an important macro asset.

Source: Refinitiv

Previous big China fades

Recall the 2015 China frenzy and the subsequent crash of Chinese equities that spilled over to SPX? Big China fades should not be dismissed.”

TNX has pulled back to 40.35 in the overnight session. You may recall that I had featured the 50-day Moving Average at 40.19 as a pullback target. There may be another day or so of decline or consolidation before resuming the uptrend.

ZeroHedge remarks, “After two very “eventful” quarterly refunding announcements by the Treasury, the first of which sent yields soaring to decade highs, when the Treasury forecast higher than expected coupon issuance in July, followed by a mirror image in October, when the Treasury surprised with slightly lower coupon issuance (offset by a surge in Bill issuance)…

… moments ago the Treasury published the first part of this week’s closely watched Quarterly Refunding Announcement, when at 3pm ET it released the estimates borrowing estimates (and overall sources and uses of Treasury debt and cash) for calendar Q1 and Q2, both of which came in well below estimates.”

ZeroHedge comments, “Born in the 90s and tested to destruction during the Great Financial Crisis, modern-day central bank independence is effectively over in all but name. Persistently large government deficits, central banks with trillions of dollars of sovereign debt and the political toxicity of elevated inflation make it impossible any longer for the Federal Reserve, ECB et al to set monetary policy fully independently from their government overseers.”

USD futures have declined beneath the 200-day Moving Average at 103.31. The Cycles Model may treat this as a possible Trading Cycle low that may test the 50-day Moving Average at 102.77. USD may show trending strength appearing next week.