8:00 am

Good Morning!

NDX futures rose to 17474.80 this morning after making its All-tim closing high yesterday. The All-time intraday high was made on Wednesday. Levels to watch for are the Cycle Top, at 17166.88, where an aggressive sell signal lies. The second level is at 16712.51, where we see the Ending Diagonal trendline and Intermediate support. The two lower levels confirm the sell signal.

today’s options chain shows Maximum Investor Pain at 17600.00. Long gamma may start at 17650.00. Short gamma may begin at 17550.00.

ZeroHedge remarks, “The merger wave starts now

Our banker friends are more busy than any other time in the past 3 years. We are hearing more and more chatter about willingness to actually commit to M&A. This is natural in this stage of the economic cycle and equity bull market. We have very high conviction that the M&A wave starts now and it will obviously matter for stock selection. We see a decent chance that this wave morphs into a merger mania tsunami, and then it will matter for the overall market. Stay tuned. And do not short take-out candidates.

The strong case for M&A

Rising interest costs have brought M&A activity to a standstill over the past two years…”

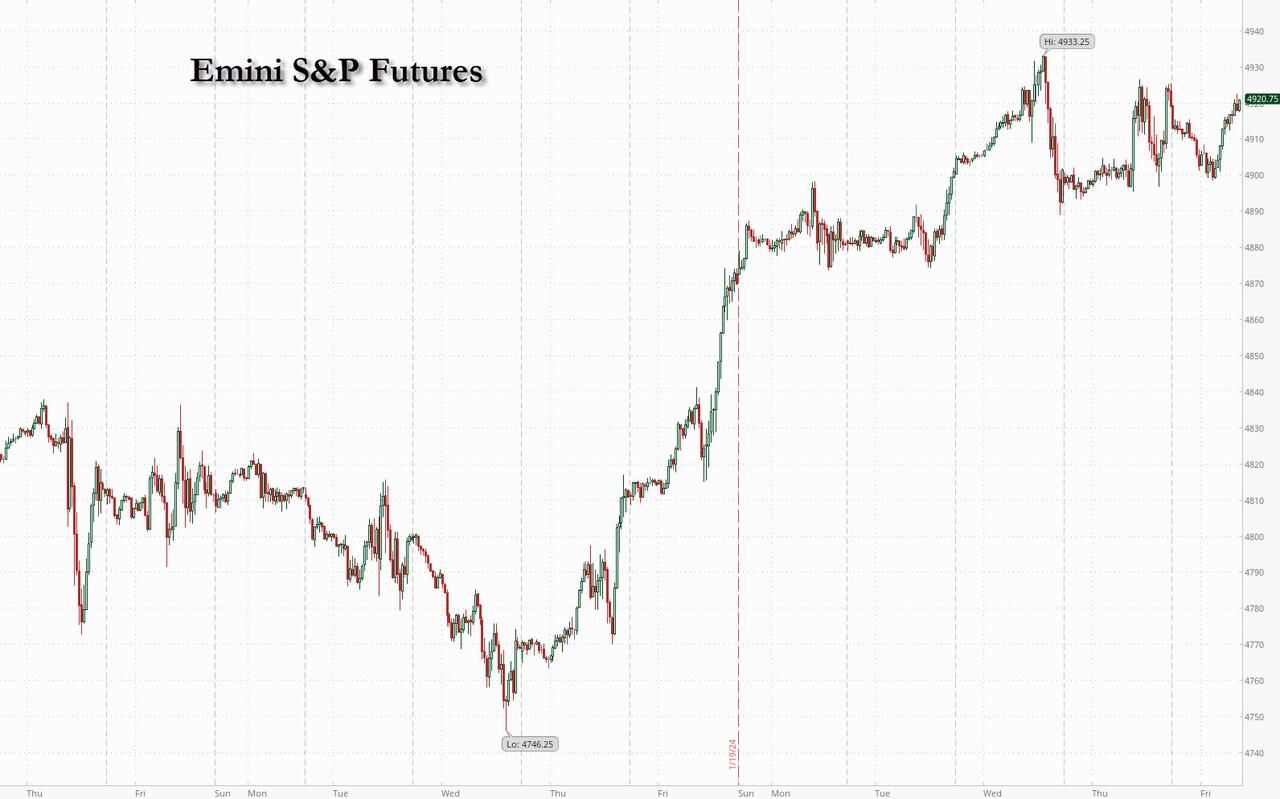

SPX futures rose to an 9vernight high at 4894.80 where it may be consolidating. Today is day 275 in the (former) Master Cycle. SPX is in throw-over and may reversa as quickly as it rose to this level. Once the decline starts, it may proceed to the end of February.

Today’s options chain shows Max Pain at 4885.00. Long gamma may start at 4890.00, while short gamma may begin at 4880.00. A very tightly coiled spring that may go in either direction.

ZeroHedge reports, “After hitting a record high for 5 consecutive days, the daily tech-led meltup is in peril after Intel reported solid earnings but disappointed consensus with weak guidance, sending the stock tumbling 11%, and putting pressure on the Nasdaq which is down 0.2% as disappointing guidance from KLA also hit semiconductor stocks; AMD and Nvidia also retreated. S&P futures are also lower on the day, if well above session lows, while Europe is higher 1% to a 2 year-high led by luxury stocks after LVMH gave reassuring results. Asian stocks closed lower, snapping a six-day win streak, as tech shares stumbled and the China rally halted amid some skepticism over the impact of market rescue measures. 10Y yields inched modestly higher, rising 2bps to 4.12% after earlier falling below 4.10%. The US dollar dropped, also reversing an earlier move in the opposite direction. Oil dipped after surging on Thursday and bitcoin recovered recent losses, trading above $41000.”

VIX futures rose to a morning high at 14.10. It is in a period of strength that may last up to two weeks. It is above the 50-day Moving Average at 13.11, giving it a buy signal that may be unrecognized by most analysts. VIX may get more recognition once it rises above the mid-Cycle resistance at 15.17.

The January 31 op-ex has virtually no short gamma. Long gamma kicks in at 15.00 and runs to 39.00.

TNX appears to be consolidating between the trendline at 41.00 and the 50-day Moving Average at 41.47. It is at a half Trading Cycle which may allow a short-term decline to the 200-day Moving Average at 40.89, or possibly Intermediate support at 40.19. All of next week’s Treasury auctions will be in bills (no notes or bonds) to keep longer-term Treasury yields down.

Yesterday ZeroHedge noted, “After yesterday’s catastrophic 5Y auction, there were concerns that today’s traditionally weaker 7Y “belly” auction would send yields into the stratosphere. And despite a modest tail, that did not happen because today’s sale of $41BN in 7Y notes went off without a hitch.”

ZeroHedge follows up with this comment, “A continued bear steepening in the yield curve may deter the Treasury from significantly increasing auction sizes in longer-term debt at its quarterly refunding announcement next Wednesday.

If proof were needed that the lines between fiscal and monetary policy are becoming ever more blurred, and that total central-bank independence is – de facto – a thing of the past, then the market’s heightened attention to Treasury refunding announcements is it.

Both of the last two were market-moving events. The next one may be too, but that will depend on by how much auction sizes of different maturities are expected to rise, and the behavior of yields and the curve in the run-up to the announcement.”

The Shanghai Composite Index rose through Intermediate resistance at 2909.64 only to lose momentum beneath the 50-day Moving Average at 2950.03, stopping its ascent at 2924.31. There is a descending trendline just above it that also indicates the decline has not been overcome. It seems that foreign buyers have taken an interest, but Chinese investors may be more willing to sell rather than buy this market. The “quasi-bazooka” of stabilizing measures by the Chinese authorities may be set up for another failure..