2:05 pm

SPX is approaching a minor support near 4380.00. You may see a bounce back to 4400.00. Otherwise, the decline continues for another possible two weeks. Short gamma is getting even shorter.

ZeroHedge remarks, “Bonds and stocks are trading heavy again today, continuing the recent trend (and reversing the high correlation regime of the prior three months)…

And, if Nomura’s Charlie McElligott is right, that trend could accelerate in the days ahead.

First, in bond-land, the UST long-end has struggled mightily now for a month-and-a-half.”

8:10 am

Good Morning!

SPX futures rose to 4415.90 this morning after yesterday’s sell-off. The most likely buyer(s) may be Japanese, as the SPX denominated in Yen is still above the 50-day Moving Average, although a reversal from the peak occurred on August 1. In the US, options gamma and dealer gamma are both negative for the first time, suggesting selling still has a way to go. The Cycles Model suggests selling may continue to the end of August.

Today’s op-ex shows options in a very tight spot with Max Pain at 4430.00. Long gamma starts at 4435.00 while short gamma begins at 4425.00. All it takes is a hiccup to start the selling.

ZeroHedge observes, “Yesterday, when looking at the key levels across the systematic universe, we warned our subs that we are “On The Verge Of A Systematic Dump” and that “a Drop > 1% Sees Good Size Selling, A Move >2% Is Gonna Be A Mess“. And judging by today’s slide, which broke below all key support levels…

… and closed at the lows, that was indeed the case, with stocks sliding another 0.7% after yesterday’s late session dump with the Fed’s hawkish minutes only adding fuel to the selloff.”

This morning ZeroHedge reports, “S&P futures reversed earlier losses that brought them perilously close to the 4400 support level, as global govt bond yields extended their recent surge to the highest levels since the financial crisis after Fed minutes showed the central bank remains worried about persistent inflation and signaled the possibility of further rate hikes while stubbornly resilient US economic data – one might say purposefully manipulated for political purposes and boosted by massive deficit spending – challenges the view that central banks rates are peaking.

As of 7:30am ET, S&P futures were up 0.2%, reversing a similar drop earlier in the session. Nasdaq 100 futures also rose 0.2% The USD reversed an earlier gain and trade near session lows, helping commodities catch a bid. Sentiment was hammered around the globe: European stocks slumped for a third day with Spain outperforming on the move lower (UKX -0.3%, SX5E -0.5%, SXXP -0.4%, DAX -0.2%.) while Asian stocks dropped to their lowest level since March amid further signs of weakness in China and mounting concerns over elevated interest rates in the US. Today’s macro/micro focus is on jobless claims, the Leading Index, and AMAT/WMT earnings.”

VIX futures eased back down to 16.61 in a slight retracement. The Cycles Model suggests a further probe higher, possibly into next week.

Next Wednesday’s op-ex still shows Max Pain for investors at 17.00. Short gamma shrank considerable while long gamma starts at 20.00 and currently runs to 33.00.

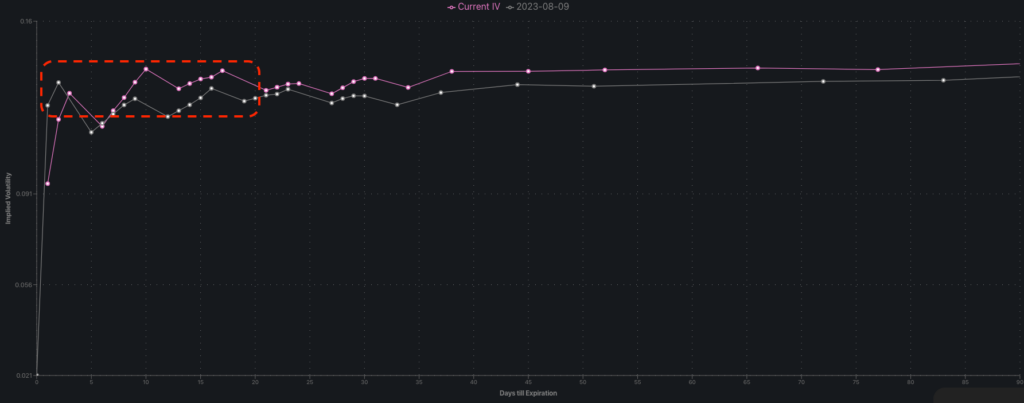

ZeroHedge remarks, “Despite the 3% decline in the S&P 500 over the month of August, both S&P 500 realized volatility and implied volatility has remained muted.

“Market down, volatility down/flat” is NOT something we are used to seeing!

This lack of shift in implied volatility is exhibited by the SPX term structure, shown below.

What about VIX?

If the reduction of options positions with expiration leads the SPX to break below 4,400, we may see a meaningful increase in volatility, with the VIX quickly moving to 20.

The other surprising factor when reviewing this expiration is the low level of implied volatility present in most stocks.”

10-year Treasury bond yield futures reached 43.18 this morning, fast approaching the October 21, 2022 high at 43.33. TNX may end the week on a higher note, as trending strength peaks over the weekend, per the Cycles Model. The rally may continue to mid-September after the potential breakout to new highs. The Head & Shoulders formation may have been completed by then.

Investing.com remarks, “Did you know that 2022 was the WORST year for US Treasuries in American history?

The benchmark 10-year Treasury fell nearly 18%, and the United States 30-Year Treasury collapsed by over 39%. Many other bonds did even worse.

Even if you go back 250 years, you can’t find a worse year for Treasuries, the foundation of the colossal global bond market.

It should forever end the ridiculous—yet pervasive—delusion that Treasuries are “risk-free.”

Many people and almost every financial institution have long thoughtlessly accepted this trope.”

USD futures declined to 102.96, testing the mid-Cycle support at 102.90 after testing the upper trendline at 103.50 and 200-day Moving Average at 103.32. Should we see a breakdown, the Cycles Model allows a decline to a new low by the end of the month.

Crude oil futures hit a low of 78.95, just above the trendline at 78.00. The Cycles Model calls for the decline to continue for about two more weeks. A likely short-term target for the decline may be the 50-day Moving Average at 75.20. However, the Cycles Model suggests a lower target later this fall near the 61.8% retracement of the 2020-2022 rally at 53.97

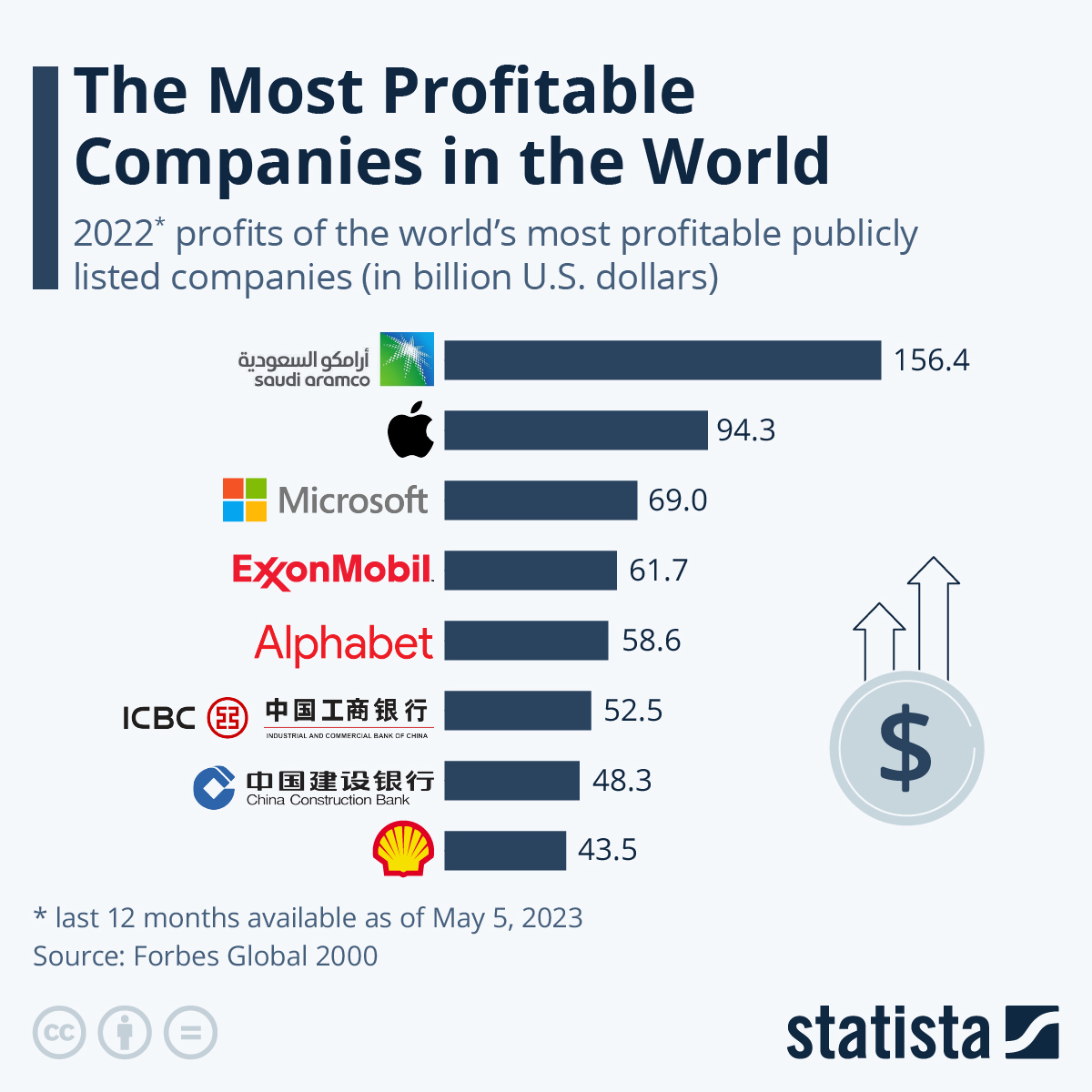

ZeroHedge notes, “According to the Forbes Global 2000, Saudi state oil enterprise Saudi Aramco is once again the world’s most profitable company – this time with a big lead over second-placed Apple as oil and gas prices skyrocketed as part of the global energy crisis in the aftermath of the Russian invasion of Ukraine.

As Statista’s Katharina Buchholz reports, there are now three oil and gas giants among the top 8 most profitable companies in the world – up from just one in 2019.

You will find more infographics at Statista

Saudi Aramco had already been touted as the most profitable company in the world before going public in late 2019.”

Gold futures declined to 1919.30, challenging the mid-Cycle support at 1921.26. Gold has bounced to 1933.25, but it may not last. The Cycles Model suggests trending strength may increase as the decline moves beneath critical support. The next visible support may be at 1810.00, followed by the Cycle Bottom at 1765.97. The decline may extend to mid-September.