7:45 am

Good Morning!

It’s time to review the bluest of the blue chips as a contrast my previous reporting. While the NDX is making new retracement highs, the DJIA may have already put in the high in December and is finishing a secondary retracement this week. There may be a final probe to 34300.00, which has been the high since January. In other words, all of the major indices are scheduled to reverse down tis week.

NDX futures are trading in a flat range this morning in a consolidation just beneath yesterday’s high. It has accomplished its Fibonacci target at a 61.8% of the 2022 decline at 14324.71. The turn date target for NDX is tomorrow. However, it may have already put in the high.

In today’s op-ex, Maximum investor Pain in options is at 14560.00. Long gamma begins at 14650.00 while short gamma starts at 14500.00. The bulls may be losing their risk off impulse.

ZeroHedge observes, “Overbought

NASDAQ and NYFANG at very overbought levels, but people tend to forget we can stay at overbought levels for longer than most can “endure”.

Source: Refinitiv

Apple – zoom out…

…and you will see there is no trend in the world’s number one stock. Getting excited about break outs, both ways, has been an expensive strategy since late 2021, vision pro or not.”

SPX futures are also consolidating beneath yesterday’s high. The SPX 17.2-month Cycle ends on Friday, but may reverse at any time. It is fascinating to see the different Cycles of the three major indices all back on the same page…

Today’s op-ex shows Max Pain at 4265.00. Long gamma may start at 4285.00, while short gamma may begin at 4260.00. Not a lot of conviction on either side…

ZeroHedge reports, “US equity futures are flat, bond yields are lower, the dollar is higher, and commodities (ex-Ags) are weaker as the excitement over the Saudi 1mmb/d production cut fizzles and as hedge fund shorts once again take the upper hand. Ags are higher led by wheat on headlines from Ukraine, where a dam was damaged in an explosion.

As of 7:45am ET, S&P futures were unchanged with the Nasdaq fractionally in the red as well, with Apple down 0.4% in premarket trading on concern the ludicrous price ($3500) of its much-anticipated mixed-reality headset will crater demand. European semiconductor firms slid after Taiwan Semiconductor — the main chipmaker to Apple — said capital spending will be at the lower end of its guidance range. Overall, there appears to be a mild risk-off tone pre-market, With the S&P 500 on the edge of a new bull market, there’s a sense among traders that markets have run up too fast on the hype for artificial intelligence. The balance of the week is light on macro data points so markets may trade in a tight range into CPI/Fed next week.”

VIX futures are flat, but may show trending strength as early as today. That suggests the trendline and the 50-day Moving Average at 17.82 may be challenged. An aggressive buy signal may be warranted due to the change in Cycles. Confirmation may occur above the 50-day.

In tomorrow’s op-ex, the 16.00 strike is hotly contested. However, there is no short gamma follow-through. On the other hand, long gamma starts at 17.00 and runs hot to 47.50.

ZeroHedge remarks, “As discussed yesterday, the VIX may be getting close to a bottom after hitting the lowest level in more than three years.

As Bloomberg’s Akshay Chinchalkar writes, the VIX collapsed by ~19% last week, the largest drop this year, as the debt-ceiling standoff was resolved and the mixed payrolls data for May diluted the odds of a rate hike this month.

The retreat means the VIX is more than 34% below its widely-followed 200-DMA. Such a significant divergence has typically marked a trough.”

TNX tested its mid-Cycle support at 36.79 this morning and may now be moving higher. It has just reached a midpoint in the current Master Cycle and has another month to go. The rest of the week may be a consolidation, according to the Cycles Model, with trending strength returning over the weekend.

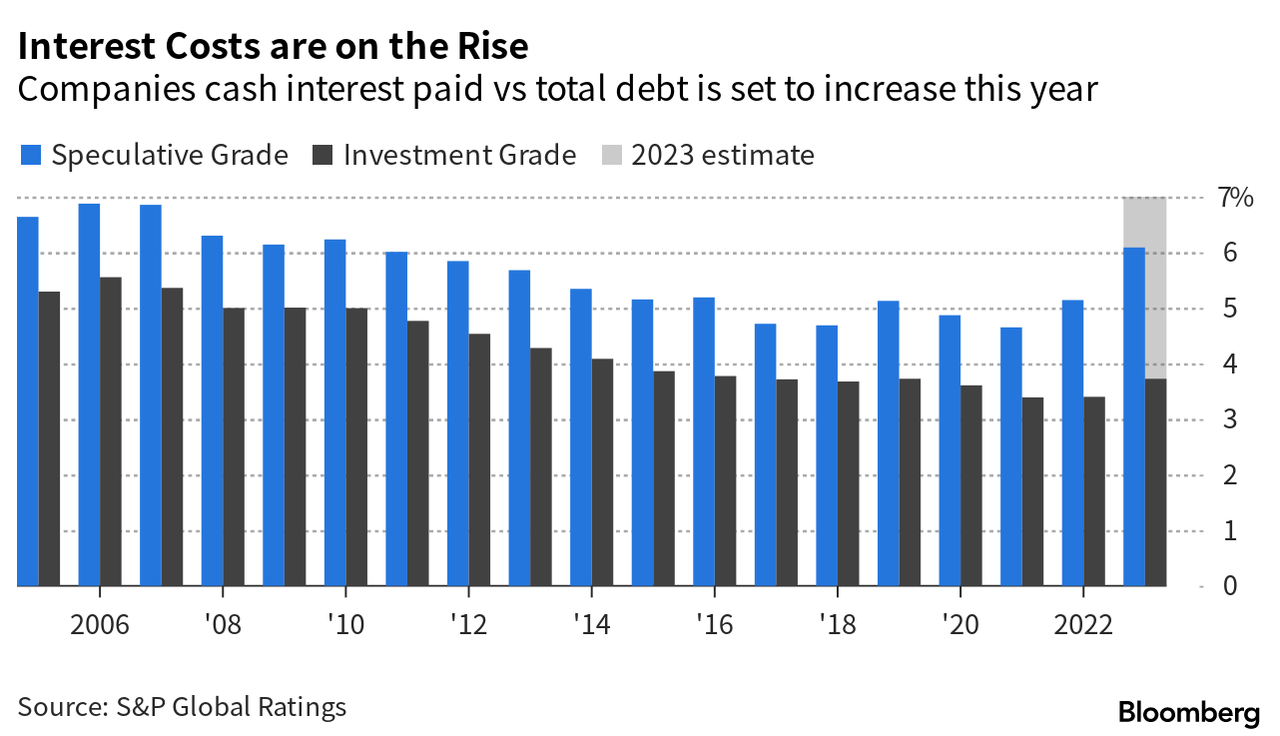

ZeroHedge observes, “For corporations with junk credit ratings, the cost of debt servicing has skyrocketed, reaching levels not seen in over a decade. This surge can be attributed to the Federal Reserve’s rate-raising campaign. And it might force some companies to reevaluate capital structures.

Bloomberg cited an S&P Global Ratings report that outlined junk-rated firms are paying an effective rate of 6.1% on debt, up from 5.1% last year. The 6.1% rate is the highest interest on debt since 2010.