9:45 am

BKX, our liquidity proxy, is still hovering in no-man’s land. It appears unable to rally as the window for that opportunity appears to be closing on day 270. This may be the last chance to rally to the Cycle Bottom at 84.72. BKX remains on a sell signal that may not change until the middle of June. This may have the makings of a waterfall event. Things may be going from bad to worse. Much worse.

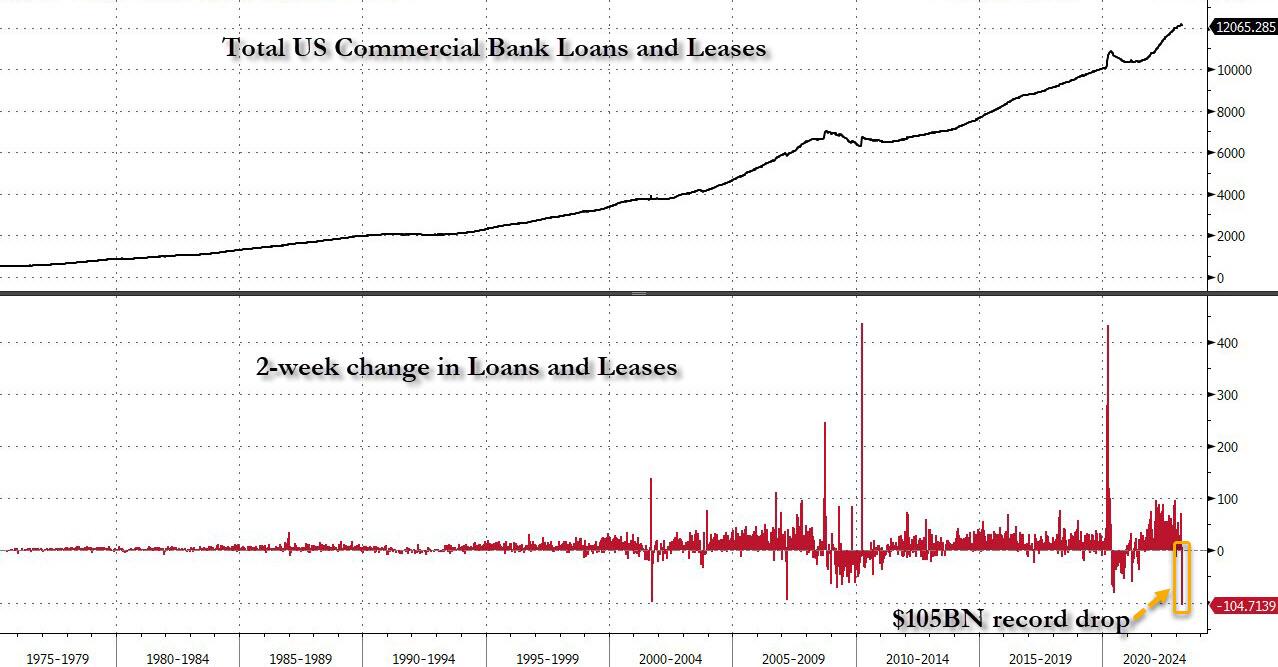

ZeroHedge reports, “Those who peeked below the surface of the latest H.8 statement which, as discussed previously, saw the biggest drop on record in bank loans and leases in the last two weeks of March…

… found another, perhaps even bigger surprise. As we detailed over the weekend when breaking down the weekly change in small bank loans and leases by their subcomponents, we found that whereas in the first week after the bank crisis (the one ending March 15) the bulk of the collapse in loans was in the traditionally volatile C&I space, the latest week was a surprise: that’s because while the plunge in C&I loans moderated substantially to just $6.9BN from $25BN the week before, the biggest slide was in one of the anchor pillars of the small bank sector: real estate loans.”

ZeroHedge observes, “Today, there is at least $7 trillion in uninsured bank deposits in America.

This dollar value is roughly three times that of Apple’s market capitalization, or about equal to 30% of U.S. GDP. Uninsured deposits are ones that exceed the $250,000 limit insured by the Federal Deposit Insurance Corporation (FDIC), which was actually increased from $100,000 after the Global Financial Crisis. They account for roughly 40% of all bank deposits.

In the wake of the Silicon Valley Bank (SVB) fallout, Visual Capitalist’s Dorothy Neufeld and Sabrina Lam look at the 30 U.S. banks with the highest percentage of uninsured deposits, using data from S&P Global.”

ZeroHedge adds, “Earlier this week, when looking at a critical real-time indicator of US loan activity – the Dallas Fed’s latest Banking Conditions Survey – which provides an early glimpse into loan supply and demand at least until the next SLOOS is released in early May, we warned that loan demand had collapsed, while credit standards had tightened to the point where there was virtually no new credit supply for broad swaths of the economy. Here is the key quote from the survey:

Loan demand declined for the fifth period in a row as bankers in the March survey reported worsening business activity. Loan volumes fell, driven largely by a sharp contraction in consumer loans…. Credit standards and terms continued to tighten sharply, and marked rises in loan pricing were also noted over the reporting period. Banking outlooks continued to deteriorate, with contacts expecting a contraction in loan demand and business activity and an increase in nonperforming loans over the next six months. Some contacts cited waning consumer confidence from recent financial instability as a concern.”

8:20 am

Good Morning!

NDX futures are testing Thursday’s low at 12846.03 this morning. While February 2 was the turning point for the blue chips, Friday, March 31 may have been the turning point for the NDX as a first quarter push to a record gain may have ended.

In today’s op-ex, Maximum Pain for options investors is at 12875. Long gamma begins at 13000.00, while short gamma appears nonexistent. Virtually no one is short the NDX.

ZeroHedge comments, “A tightness in my chest…a bad feeling….something wicked this way comes. Or not. The markets have become very unkind. From week to week we have to deal with something else. Whether it be banking crises and bankruptcies, rates volatility, funding pressures and then a broader volatility spike, basis blow out and de-grossing that caught all and sundry. Then, without much reason or rationale we revert to mean. Equity vol abates, we see a week long rally and if headline indices were to be believed, it is as if nothing happened at all.

So in summary another head scratching week. Focus remains on US regional banking space and whether we are at the end or the beginning as well as growing concerns around the economy.

It increasingly feels like equities are caught in a channel. One that most believe (and are positioned) to see break on the downside and yet never seemingly does. Tony Pasquariello pointed out that the S&P spent Q1 in a 10% trading range – 3808 to 4180 – for the tightest bad since Q3 2021. On top of the usual debates around rates/inflation and the consumer….we worry about US regional banks, systemic and contagion risks, geo-political shifts, volatility in rates and fx, corporate earnings and margins, commercial real estate and leverage beneath the surface…and increasingly worry also about recession. There was a time where bad news was good news in the sense that bad news meant more stimulus, more liquidity and more backstop. Now it feels like bad news may just be that…..bad news. For now however, we muddle through. Last week the latest round of a gradual and steady rally for no discernible reason.”

SPX futures dipped to 4069.96, still within Thursday’s trading range. The European market remains closed for Easter, so there is no directionality from that part of the world. The Cycles Model suggests the decline may continue in the Blue Chips, as the rally did not succeed in making a new high. The next Master Cycle Pivot occurs in early May.

Today’s op-ex sows Max Pain at 4115.00. Long gamma starts at 4150.00, while short gamma begins at 4050.00. The April 21 (monthly) op-ex shows 4000.00 as a hotly contested strike for both puts and calls. with over 80,000 contracts on either side.

ZeroHedge reports, “With much of Asia and Europe still closed for Easter Monday, US stock futures, already painfully illiquid, were trading in a narrow range for much of the session, before losing all of their post-payrolls gains as investors assessed the path of Federal Reserve monetary policy following Friday’s jobs report. Contracts on the S&P 500 dipped 0.2% at 7:30am while Nasdaq 100 futures dipped 0.4% as the dollar spiked to session highs on the back of yen weakness following the latest comments from the BOJ’s new head Ueda.”

VIX futures rallied this morning to a new high at 19.91 after Thursday’s surprise Master Cycle low. Please read Thursday’s blog for a complete explanation. Should that analysis be correct, the VIX may rally through the end of May. A breakout occurs above 20.08.

In Wednesday’s op-ex, calls now dominate VIX options from 18.00 to 35.00. Sentiment has turned dramatically.

TNX has turned up in strength, as predicted last week. The Master Cycle has stretched in the case of TNX, where it has shortened in the VIX to match an important turning point in the markets. The Cycles Model suggests the new Master Cycle may have as little as a week to perform. However, should the strength of the new trend persist, it may last through the end of April.

USD futures have risen to a morning high of 102.35, establishing the swing low made on Wednesday. The current Master Cycle is due to make its Pivot at the end of April, suggesting new highs may be in the offing. The cries for the collapse of the USD are getting louder. However, as bad as things are, they are much worse in the rest of the world.