2:23 pm

SPX may have given us an actionable formation at the descending trendline (and Cycle Top in the 2-hour chart). There is a clear Head & Shoulders formation where the left and right shoulders are nearly identical in size, giving us multiple confirmations of the validity of the formation.

ZeroHedge opines, “Until today’s unexpectedly dismal JOLTs report which confirmed what we had known for months – namely that the BLS was purposefully showing an artificially strong picture of the US labor market for months to make the admin looks good in a time when everything else as bad – markets were on a tear, with the S&P rising four days in a row on the back of a furious technical rally and short squeeze, which allowed the S&P to enter April with momentum coming off of a strong rally into the end of March when the SPX finishing Q1 up 7%. But is that momentum now at risk of reversing.”

1:55 pm

The Ag Index may have made its Master Cycle high yesterday, on day 256. I am concerned and hopeful that an even higher high may be made in the next week to give the Wave structure more clarity. A high nearer to the Cycle Top resistance at 488.08 (or at least above 477.11) would clearly establish a new uptrend. Otherwise, remaining beneath the mid-cycle resistance may confirm lower lows until mid-July. There may be a spike of energy to elevate GKX by the end of the week that may clarify the dilemma..

ZeroHedge observes, “California’s vast amount of agricultural land is facing a significant issue due to a series of atmospheric rivers in recent months, which have saturated fields to the point where planting crops has become difficult.

“It’s just too damn messy and muddy to create a quality pack. You don’t want a bunch of mud on the produce,” Christopher Valdez, president of the Grower-Shipper Association of Central California, told USA Today.

More than a dozen powerful storms later, 78 trillion gallons of water has been dumped on California, reversing a multi-year drought in a matter of months. Now the agricultural powerhouse state, producing about a third of the country’s vegetables and three-quarters of its fruits and nuts, faces planting delays due to washed-out fields.

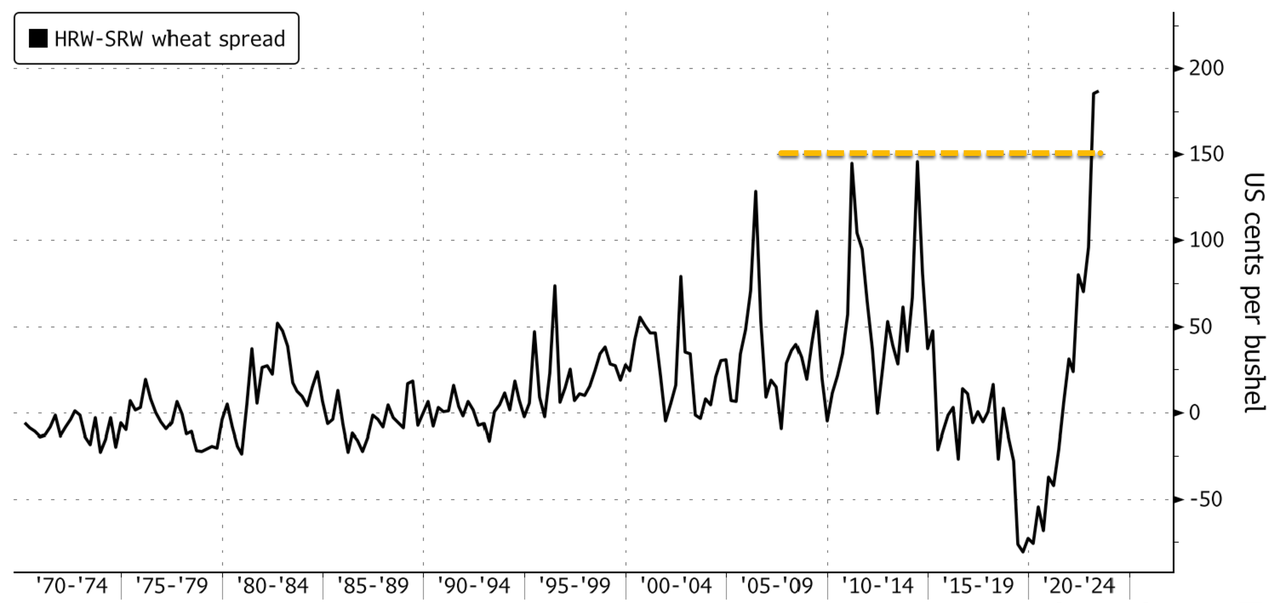

ZeroHedge reports, “The spread between hard-red winter wheat and soft-red winter wheat has blown out to a record high as drought threatens crop yields across the Midwest and other major farming regions.

Hard-red winter wheat’s premium over soft-red winter wheat is $1.72 a bushel in Chicago on Tuesday morning, surpassing the 2011 record.

James Bolesworth, managing director at CRM AgriCommodities, told Bloomberg the widening spread is “a factor of the drought in the US Plains which is detrimentally impacting crop conditions.”

1:28 pm

BKX appears to be breaking down from its March 30 Master Cycle high, but has not exceeded its low. Should it exceed the low at 76.20 we may see bank stocks tumble through mid-June. This is serious enough to warn that people should have cash in hand, not just in the bank. This isn’t just a domestic threat. We are observing a world-wide systemic failure.

ZeroHedge observes, “Credit Suisse Group AG Chairman Axel Lehmann told a room of shareholders that he was “truly sorry” the Swiss bank imploded and for the controversial takeover by UBS.

“It is a sad day for you and for us too. I can understand the bitterness, the anger, and the shock of all those who are disappointed, overwhelmed, and affected by the developments,” Lehmann said in remarks prepared for the bank’s annual shareholder meeting in Zurich.

“I apologize that we were no longer able to stem the loss of trust that had accumulated over the years, and for disappointing you,” he said. “

ZeroHedge comments further, “Having correctly forecasted the “unprecedented” risks from the combination of inflation, war, and COVID in last year’s letter, JPMorgan CEO Jamie Dimon offers only a very dim silver lining for the way forward (current consumer strength and AI opportunities) while warning that the banking crisis is “not over yet”, fearing an “overreaction” by regulators,

“As I write this letter, the current crisis is not yet over, and even when it is behind us, there will be repercussions from it for years to come. But importantly, recent events are nothing like what occurred during the 2008 global financial crisis.”

Dimon is quick to point the finger of blame at the regulators…

“Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements,” Dimon said.

“Even worse,” he added, the Federal Reserve didn’t stress-test banks on what would happen as rates jumped.”

TheEpochTimes reports, “The month of March witnessed the fastest withdrawal of funds from commercial banks in U.S. history.

According to data released by the Federal Reserve, a staggering $360 billion was withdrawn from banks across the country in the past month alone. To put this into context, not a single monthly decline in 2008 exceeded $100 billion. The recent withdrawals have dwarfed those of the past, bringing total bank deposits down by almost $1 trillion since the highs in April 2022.”

7:30 am

Good Morning!

NDX futures have declined to 12086.52 this morning, having met both time and price targets for this correction. It may lead the decline into the end of April. Should the short squeeze go higher, overhead resistance is at the Cycle Top at 13391.00.

In today’s op-ex, Maximum Pain for investors appears at 13050.00. Long gamma begins at 13100.00, while short gamma starts at 13020.00. Speculators are chasing the long side with 13200.00 being te most favored strike.

ZeroHedge suggests, “Imagine seasonality kicks in

We are here…

Source: Equity Clock

The CTA flip

All thresholds in positive now: short term 3998, medium term 4006 and long term 4108. CTA projected flows by GS:

1 week: flat buy 29bn, up big 31 bn to buy, down big almost 8bn to buy

1 month: flat buy 40bn, up big 43 to buy, down big sell almost 9bn

Upside convexity is the stronger force here…The projections above are for SPX only.

Long/short still depressed

Imagine if/when hedge funds start reversing this trend?

Source: GS

Must buy

Not overly surprising, but the most recent squeeze has forced the crowd into buying this market. GS prime book notes: “… largest notional net buying since Sep ‘19, driven by risk on flows with long buys outpacing short sales ~2.5 to 1.” They have bought, but could be forced into buying even more…”

SPX futures rose to a high of 411.40, challenging the 2-hour Cycle Top at 4133.26. Should it pull back beneath the Cycle Top, a reversal may be underway, as SPX may have fulfilled both time and price targets.

Today’s op-ex reveals Max Pain at 4115.00. Long gamma begins at 4165 and peaks at 4200.00. Short gamma begins at 4110.00 with short interest rising to 4025.00.

Zerohedge reports, “US futures extended gains for a 5th straight day as investors weighed the outlook for the Fed’s rate hiking path following weak US manufacturing data against inflation concerns from OPEC+’s plan to cut oil output to assess the path of interest rate increases, and after the Australian central bank officially paused its rate hike campaign overnight when it kept its rate unchanged at 3.6%. S&P 500 contracts rose 0.3% on Tuesday as 7:30 am ET after the underlying benchmark reached its highest level since mid-February on Monday. Nasdaq 100 futures were 0.6% higher, extending their bull market 20% rally while a gauge of volatility held near this year’s lows helping a benchmark for world stocks advance for a seventh day, its longest streak since Jan. 16. Europe’s Estoxx50 advanced 0.8% as Asia dipped; the US dollar reversed an overnight drop and traded modestly green while TSY yields rose, pushing the rate on the 10Y to 3.46%. Oil built on the largest gain in a year after OPEC+ set out to punish short sellers with a surprise production cut; WTI was near $81 a barrel after closing more than 6% higher on Monday.”

VIX futures appear to be consolidating above its Cycle low, made last Friday. The optimum window for adding VIX ETFs and options may be closing. Buy when you can, not when you must. Yesterday’s reversal came with strength that may continue this week. The Cycles Model indicates the uptrend may resume through the end of April.

Next Wednesday’s op-ex shows Max Pain at 20.00. Short gamma starts at 19.00 and only eextends to 18.00, while long gamma starts at 21.00 and extends to 42.50.

TNX retested its trendline at 34.00 yesterday and may now be rising to challenge mid-Cycle resistance at 35.40. The reversal from the March 24 low has remained unrecognized, but may soon change with a breakout above the 50-day Moving Average at 36.02. The Fed’s tightening is regarded as a policy error by most domestic analysts. Unfortunately, rates may continue to rise, dragging the Fed into further tightening.

TheEpochTimes reports, “The Federal Reserve’s year-long aggressive monetary tightening efforts could turn out to be one of the most significant policy errors in the last several decades, according to renowned economist Mohamed El-Erian.

El-Erian shared excerpts from the Peterson Institute for International Economics (PIIE) and the Financial Times that reinforced his view that the U.S. central bank is committing egregious policy missteps.

“As first mentioned almost a year ago, I fear that this may well end up being the biggest Fed policy mistake in several decades,” the chief economic adviser at Allianz tweeted on Monday.”