1:15 pm

“Depositors Have Finally Awoken”: The Second Wave Of The Bank Run Has Begun, Barclays Warns

It may seem like an eternity ago, now that we stuff a month’s worth of trading and newsflow in a day, but it was exactly one week ago that Bill Ackman – who may or may not be long regional banks and/or commercial real estate – took to Twitter to bash Janet Yellen for restarting the bank run that defined much of the middle of March, when she unexpectedly told Congress that the Treasury was not considering a broad increase in deposit insurance, a line which promptly sent stocks tumbling.

And while it is no secret that Ackman enjoys hyperbole every now and then, he may have been onto something.”

10:33 am

The Ag Index may be making its Master Cycle high today, on day 251. This is not what I had hoped for. Last week I suggested the Cycles might allow a quick resolution to the downside, with a recovery in food prices to follow. Time is running out for that scenario. Instead, GKX may test the next level of support near 380.00. Higher seed and fertilizer prices coupled with diminishing loan capability may hobble farmers at planting time. Proper use of fertilizers may increase crop yields by as much as 40%.

FarmProgress reports, “As we approach the March 31 Prospective Plantings report from USDA, let’s take a look at one of the most significant factors playing into corn and soybean markets over the past year or so – fertilizer expenses.

In our March 2023 Farm Futures survey, nearly 80% of farmer respondents expect this year’s profits will be lower than last year’s. For those growers bracing for lower profits this year, 35% of respondents cite higher input costs as the primary cause.”

ZeroHedge remarks, “We all lose from the global war on farmers…

France is in flames. Israel is erupting. America is facing a second January 6.

In the Netherlands, however, the political establishment is reeling from an entirely different type of protest — one that, perhaps more than any other raging today, threatens to destabilise the global order.”

9:59 am

BKX may have finished its correction this morning on day 259 in a very irregular correction. This is the canary in the coal mine, folks. The inability to bounce communicates weakness beyond our worst fears.

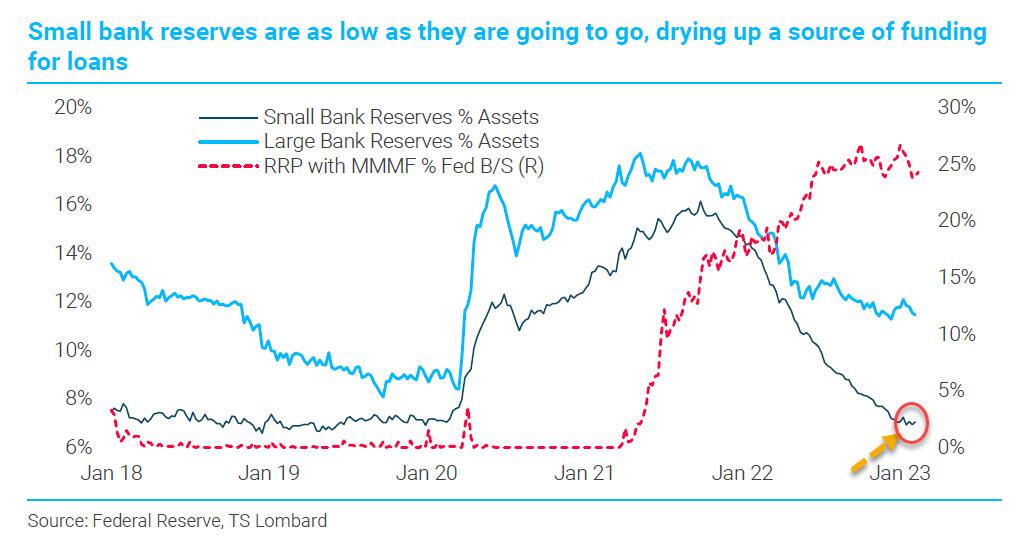

To make matters worse, alternate forms of savings (MMFs) are attracting depositors away from banks. Businesses are begging the Fed and FDIC not to crash the market. Should today be the high, we may see two months of decline in the banking sector, with knock-on effects to most businesses.

ZeroHedge reports, “While any group of three Wall Street analysts will have at least three opinions about when the next recession will strike, there appears to be uniform agreement about one thing: the current bank crisis will lead to a severe credit crunch as a result of the deposit runs and reserve shortages across small banks…

… which in turn will lead to an even sharper tightening in credit standards, which is a problem because as we reported in February, well before the current bank crisis, “Fed Loan Officers Paints Dire Picture: Loan Standards Approaching Record Tightness As Loan Demand Plummets.”

8:00 am

Good Morning!

NDX futures are higher, reaching a morning high of 12917.50 but straining against resistance at the 38.2% retracement level. The March 22 high may not be exceeded. NDX has gone higher thanthe February 2 Pivot high, but the other indices may honor the earlier high and go no further. Measuring this retracement against the 2022 decline tells us that the NDX has lost much of its prior strength, but investors are only looking at the past quarter and not the bigger picture. The fact is, the NDX and the blue chips are totally dependent on the tech generals for this rally.

Today’s NDX op-ex is bullish above 12800.00, with long gamma beginning at 12850.00.

QQQ (312.72) options expiration shows Max Pain at 310.00 with Long gamma at 312.00 and short gamma starting at 303.00.

ZeroHedge remarks, “Fab Five

Five big tough guys can do wonders when it comes to change overall sentiment….S&P 5 vs. S&P 495 YTD”

SPX futures are also in rarified air, reaching for the 61.8% retracement value at 4059.37. The February 2 Pivot remains the high point in this Cycle. The trend is down, although not yet recognized. A sell signal resides beneath the 50-day Moving Average at 4013.38. The Cycles Model suggests that the decline may reassert itself early next week.

In today’s op-ex , the 4000.00 strike is hotly contested by both puts and calls. Long gamma begins at 4030.00, while short gamma starts at 3950.00.

ZeroHedge reports, “US index futures extended their gains for a third day, approaching 4,100 – the highest level in over a month – amid easing concerns around the banking crisis and as investors weighed the likelihood that a peak in interest rates is nearing. As of 730am ET, S&P 500 futures were up 0.5% near session highs of 4,080 while the Nasdaq rose 0.6%. The tech-heavy index is set for its best quarter since 2020, pushing into a bull market Wednesday and closing at the highest level since August in a sign investors are preparing for the Fed to end its interest rate hiking cycle and potentially pivot to looser policy later this year. On Wednesday, the gauge entered a new bull market, rising more than 20% from December lows. The yield curve steepened as the 10Y yield dipped 2bps to 3.54%, while the DXY has resumed its selloff and remains below its 50, 100, and 200dma. Commodities are stronger with all 3 complexes stronger.”

VIX futures reached a new retracement low of 18.85 this morning. Most investors see this as an indication of risk off. On the contrary. We are witnessing the wind-up for the largest VIX move since 2020. he Cycles Model suggests a burst of trending strength starting on Monday with a double dose of trending strength a week later. The Master Cycle winds up with another double dose of strength in the last week of April.

In next Wednesday’s op-ex, put love is waning, with Max Pain at 20.00. The massive put interest expired in yesterday’s op-ex. Long gamma begins at 25.00 and extends to 42.50 thus far…

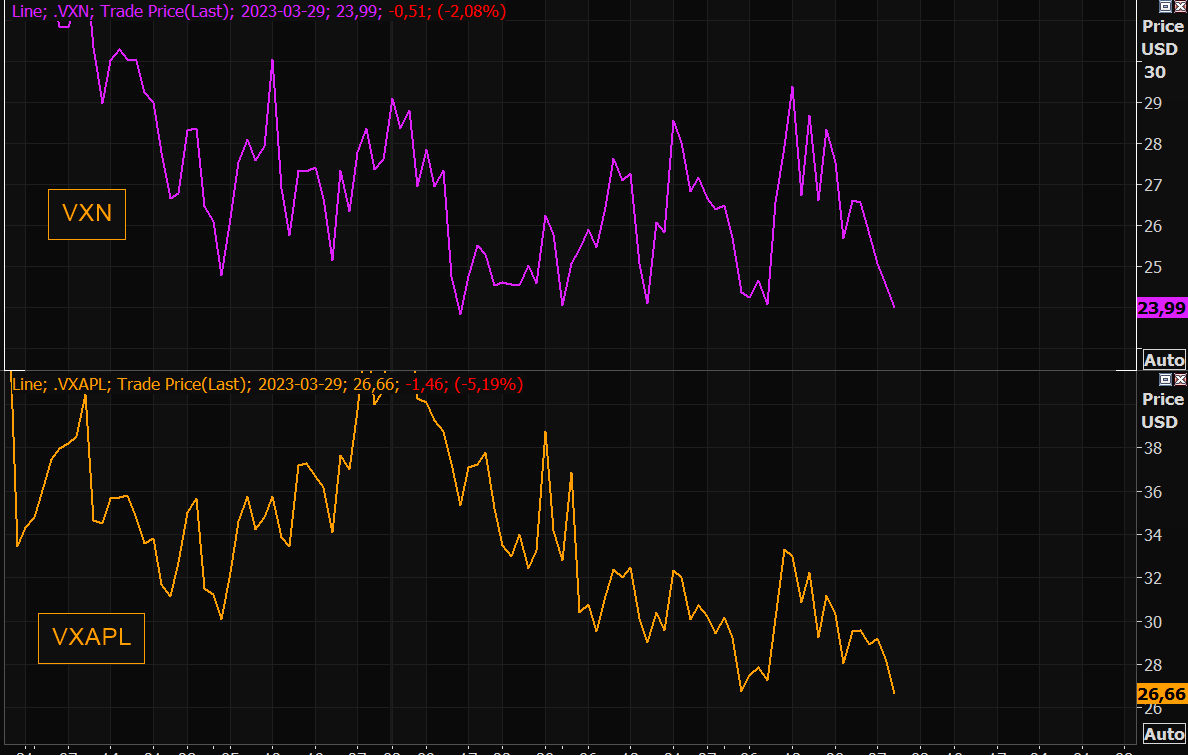

ZeroHedge observes, “Fading (big tech) fear

VXN and Apple “VIX” (VXAPL) in full implosion mode, both trading at/below lowest levels in a very long time.

Source: Refinitiv

and it’s back

Put hate is back, and the crowd managed doing it again, loving puts at local market lows. Let’s see if we get the inverse soon?”

TNX is consolidating after yesterday’s rally. The next resistance is at the trendline and 50-day Moving Average at 36.61. The Cycles Model suggests a steady rise in the TNX with a burst of strength on April 10.

ZeroHedge reports, “After a dismal 2Y auction and a solid 5Y, moments ago the Treasury concluded the week’s coupon issuance when it sold $35BN in 7 paper in a passable auction.

The high yield of 3.626% was down sharply from the 4.062% in February if above January’s 3.517%; it also tailed the When Issued 3.615% by 1.1 basis points; this was the 5th tailing 7Y auction in the past 6.

The bid to cover of 2.394 was the lowest since November and was on the lower end of the range from the past year; it was certainly below the six-auction average of 2.49.”

USD futures have corrected down to 101.80 as it consolidates before moving higher. The Cycles Model suggests the return of the uptrend with a large boost of energy on or around April 10.

Crude oil futures may have made its Master Cycle high yesterday, on day 258. It also challenged its Broadening Wedge trendline in a pullback after activating the Broadening Wedge. Crude is on a sell signal beneath the 50-day Moving Average and may remain so for the next two months.

OilPrice.com comments, ” Following a 10% slump in two weeks, oil prices jumped by 5% on Monday as concerns about the banking sector eased and 400,000 bpd of crude exports from Kurdistan were shut in.

The move lower in oil prices this month was driven by broader market jitters amid a liquidity scare in the banking sector, which saw two U.S. banks fold and Swiss giant Credit Suisse taken over by domestic rival UBS. Speculative liquidation of long positions in oil also contributed to the plunge in oil futures prices.”