10:15 am

Last week I have warned of a possible short squeeze in bank stocks lasting through the rest of this week. A combination of “good news” and the lack of bad news may aid in this analysis, however short lived it may be.

ZeroHedge remarks, “Despite an ongoing “banking crisis,” investors continue to chase stocks triggering several bullish buy signals. As noted in this past weekend’s newsletter, two primary reasons exist for this current dichotomy. The first is psychological, and the second is purely technical.

The psychological component of the recent disregard of underlying financial and economic risk is the “Pavlovian” response to Central Bank interventions. To wit:

“Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g., food) becomes paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when he introduced the neutral stimulus, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must get followed by the “potent stimulus” for the “pairing” to complete. For investors, as the Fed introduced each round of “Quantitative Easing,” the “neutral stimulus,” the stock market rose, the “potent stimulus.”

8:15 am

Good Morning!

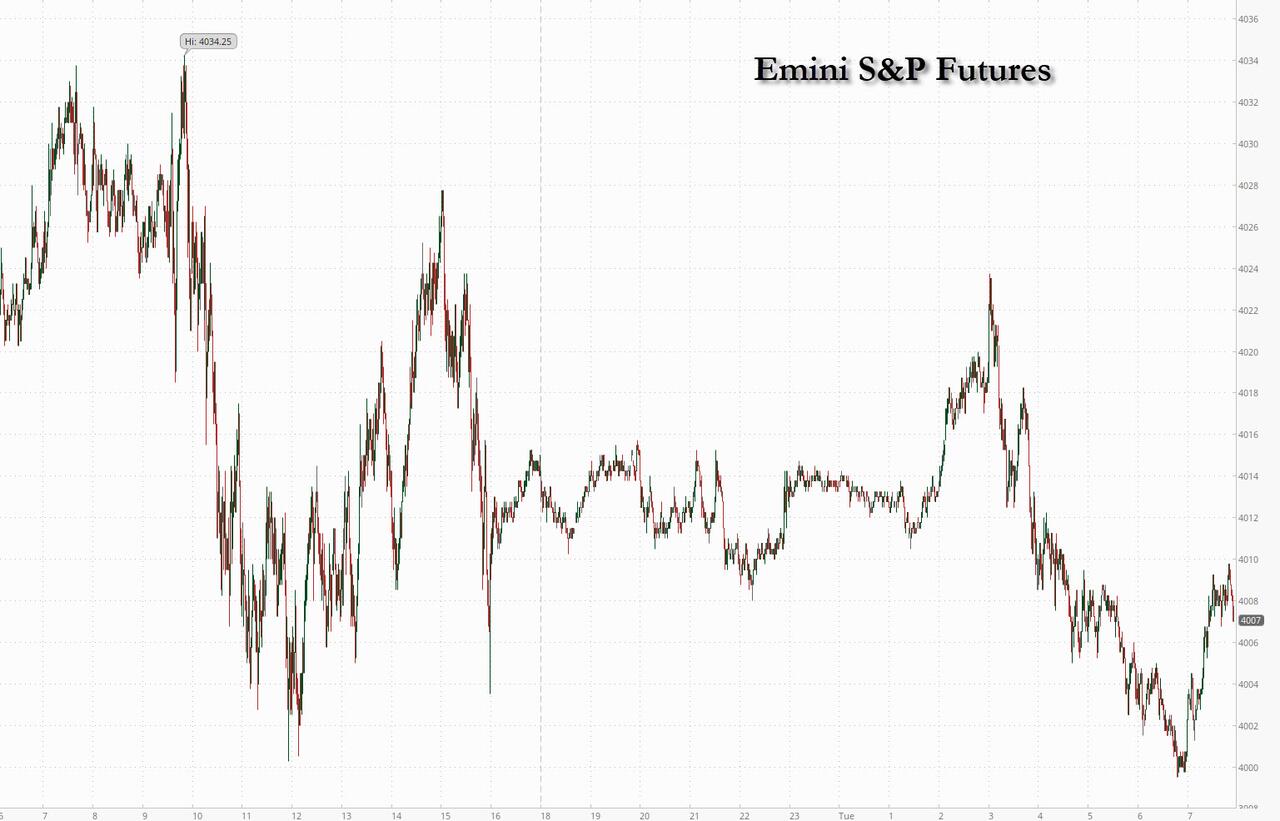

SPX futures are flat this morning, just under resistance at the 50-day Moving average at 4012.59. Support is at the mid-Cycle line at 3941.90. SPX remains on a sell signal. The appropriate behavior is to sell the bounce. There may be attempts to keep the SPX above 3839.50, the December 30 close, until the end of the month. The Cycles Model indicates trending weakness beginning next week.

In today’s options expiration, Maximum Pain for options investors is at 3980.00. Long gamma begins at 4000.00, while sort gamma starts at 3955.00.

ZeroHedge reports, “US futures are flat with bond yields reversing an overnight drop, lifted by the belly of the curve; the USD weaker for 8 of the past 9 days, and commodities mostly higher as investors shift their focus back to concerns about inflation and potential further monetary tightening from the recent banking-industry chaos; after all, a bank hasn’t failed in at least a few days. WTI has soared 5.6% this week.

S&P 500 contracts were little changed as of 7:45 a.m. ET, after earlier gaining as much as 0.4% and closing 0.2% higher on Monday. Nasdaq 100 futures slid 0.2% after the tech-heavy benchmark lost 0.7% on Monday following strong gains over the previous two weeks. European stocks advanced along with Asian equities and the dollar traded lower as fears of broader contagion from the banking turmoil eased.”

VIX futures are slightly elevated as the new (up)trend finds support at the 50-day Moving Average at 20.71. The Cycles Model shows a potential burst of strength beginning next week and lasting through the month of April. VIX may be due to emerge above its Triangle pattern in the next week.

Tomorrow’s op-ex shows Max Pain at 20.00 with virtually no substantial puts beneath it. On the other hand, long gamma starts at 25.00 with substantial long interest up to 55.00. The April 19th monthly expiration shows long gamma starting at 24.00 and long interest up to 75.00.

ZeroHedge comments, “One of the most frequent laments on Wall Street these days – where sentiment has turned from mere “doom and gloom” to outright “apocalyptic” and according to the latest BofA fund manager survey the majority of Wall Street professionals now expects a “systematic credit event” emerging unexpectedly out of the shadow banking sector – is how is it possible that after everything that has happened, are stock not only not lower but actually rallying?”

TNX has risen above the mid-Cycle resistance at 35.25 and is now on a buy signal. The Cycles Model suggests a possible three more weeks of rally, giving TNX the chance to break out above its March 2 high at 40.91. The market is still bullish on bonds, possibly leading to a trap for investors as yields surge higher. Fundamental analysis may not work in the bond market, as forces beyond the domestic purview gain ascendancy. The developing war in the Ukraine may have a greater effect on bond yields that what is being calculated. The White House has sent more than $75 billion in aid to the Ukraine in the past year in an undeclared war. This figure may actually be low, since the US has also been sending military aid to Poland and other neighboring countries near the Ukraine. But no money for Ohio….

ZeroHedge remarks, “The labor market, the yield curve, inflation and a stock-market selloff are poised to force the Federal Reserve into a rate cut sooner than the market is currently pricing.

In markets, it pays to remember that things take longer to happen than you think they will, and then they happen much faster than you thought they ever could. It was only two weeks ago that the market was expecting up to another four rate hikes. Now it’s effectively pricing the end of the rate-hike cycle, and the first cut by the end of the third quarter.”

USD futures are lower this morning, but may be poised for a surge higher after the quarter end. Although not discernible yet, the trend is higher through the end of April.

ZeroHedge remarks, “The dollar is at risk from further deterioration in the Fed’s balance sheet as it moves to stabilize the US banking system.

Markets are taking a breather this morning after the histrionics of last week. Nonetheless, problems remain, with several smaller US banks still at risk after the decimation of sentiment in the wake of SVB’s collapse.

The calm is being aided by reports that one particularly beleaguered lender, First Republic, will receive more support from the Fed. The central bank is expected to extend its lending programs to help banks in First’s position.”

Crude oil futures are hovering near the 50% retracement level and Broadening Wedge trigger line as the Master Cycle appears to be wrapping up on day 257. There is a sell signal beneath the 50-day Moving “Average at 76.26. The Cycles Model suggests a month of decline ahead, after which accumulation of shares may be de rigeur.

OilPrice.com reports, “Russia has succeeded in redirecting its crude oil and fuel exports after the EU embargoes and the price cap set by the West, Russian Energy Minister Nikolai Shulginov said on Tuesday.

Russia hasn’t reduced its sales of crude and petroleum products, the minister was quoted as saying by Russian news agency TASS.

“As far as sanctions are concerned, it is important to not only keep the production and refining volumes but exports, too, and thus the revenues for the federal budget,” Shulginov was quoted as saying.”

Gold futures have another week to wrap up its Master Cycle with a new high. It may end up with an expanded flat correction with a target near 2078.00. The all-time high thus far has been 2089.20 in August 2020. Thereafter, a decline may be anticipated, lasting through the end of July. The Cup with Handle formation may be engaged.