10:10 am

The Ag Index continues in a (more or less) flat correction that may last another two weeks. Thus far, the Cycle Bottom has held, but may give way to a quick plunge to 400.00-430.00 in its final days, making a potential flat correction. The bottom may be a volatile one, with a sharp recovery. The reversal may launch one of the largest rallies since the recovery out of the 2020 low. Be prepared.

FoodBusinessNews reports, “Recap for March 22

- Traders liquidated long positions starting before the Federal Reserve announced the latest interest rate hike, leaving wheat and soy complex futures lower for the day and corn futures mixed. The most-active soybean contract touched a 15-week low in the session. More pressure on the wheat complex came from beneficial, timely rains in France and elsewhere in western Europe. The renewal of the Black Sea grain initiative weighed on wheat and deferred corn prices. May corn added 3½¢ to close at $6.33½ a bu, but later months were mixed. Chicago May wheat dropped 19¾¢ to close at $6.63½ a bu. Kansas City May wheat lost 9¢ to settle at $8.11¼ a bu. Minneapolis May wheat lost 12¢ to close at $8.33¾ a bu. May soybean futures were down 18½¢ to close at $14.48½ a bu. May soybean meal shed $9 to close at $451.60 per ton. May soybean oil dropped 1.60¢ to close at 54.64¢ a lb.”

9:36 am

Despite all the headwinds, BKX may be poised for a technical bounce back to its Cycle Bottom resistance at 90.83. Today is day 252 in the current Master Cycle, leaving another week for it to bounce. An alternate view may take the bounce to the neckline at 96.00. The bounce may be another shorting opportunity, as the decline Cycle is not yet over. In fact, the next phase of the decline may take up to three months to the low. We are not just talking about a higher risk for smaller banks. There is a systemic risk of asset mismatches across the board. In addition, WOKE investing has left portfolios with large segments of non-performing assets.

ZeroHedge reports, “Over the past weekend, it was determined that the Federal Deposit Insurance Corporation (FDIC) would break up Silicon Valley Bank into two separate auctions. But now, the auction for SVB’s wealth-management unit has been delayed.

FDIC was set to receive bids for Silicon Valley Private Bank, successor to Boston Private, which SVB acquired in 2021 at 2000 ET Wednesday. However, without any reasoning, government regulators shifted the auction until Friday, according to Bloomberg, citing people familiar with the matter.”

(Could this be the turning point?)

ZeroHedge observes, “Amid the justifiably shocked outcry from Credit Suisse junior debtors, who saw their entire AT1 debt tranche wiped out before the equity was fully impaired, violating every conventional liquidation waterfall, on Thursday Swiss financial regulator Finma has defended its decision to wipe out a huge swath of risky subordinated bonds as part of the Credit Suisse rescue deal even as an army of bondholders is preparing to sue the Swiss government.”

ZeroHedge adds this observation, “The cascade of defaulted regional US banks is blowing out the circulating inventory of distressed debt which expanded by about $65.9 billion last week as US insolvency courts saw six new, large bankruptcy filings, according to data compiled by Bloomberg.

The heap of dollar-denominated corporate bonds and loans in the Americas trading at distressed levels rose to $295.4 billion in the week ended Friday, a 28.7% increase from $229.5 billion a week earlier, Bloomberg-compiled data show.”

8:30 am

Good Morning!

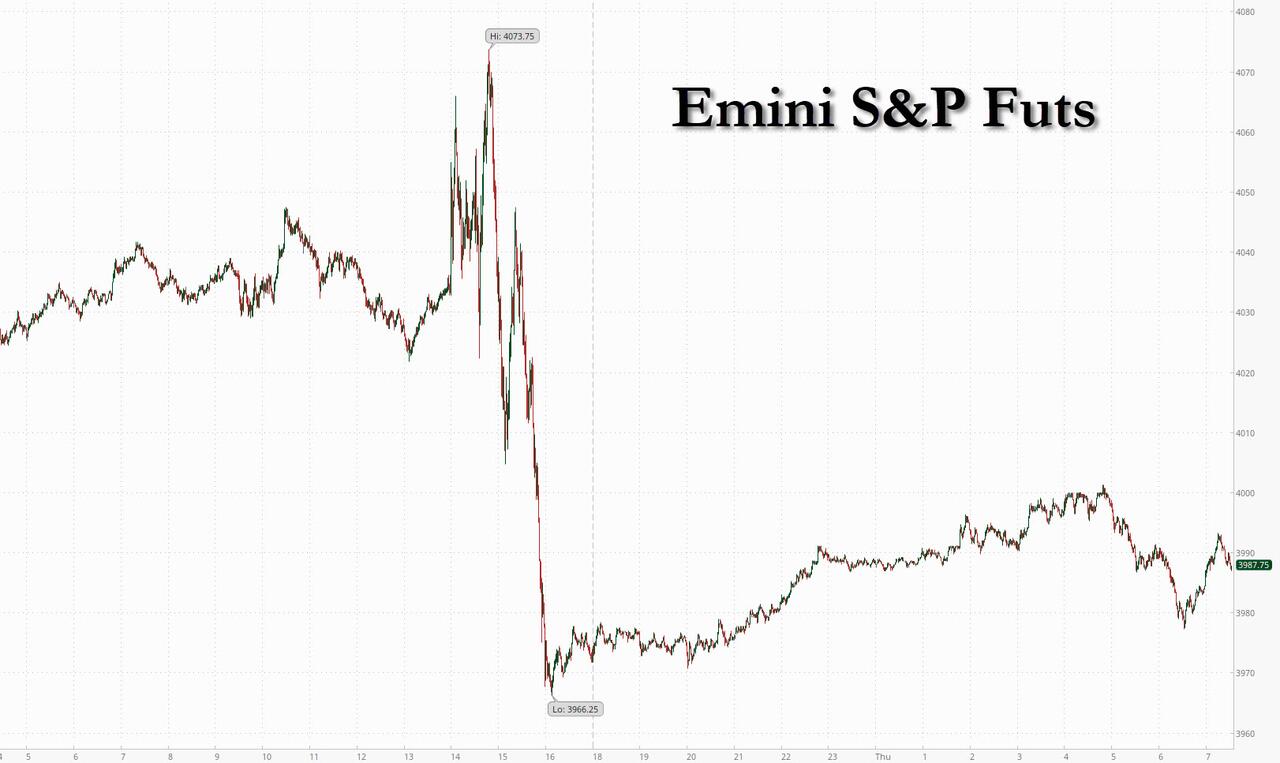

SPX futures bounced this morning to 3968.10, remaining beneath the 50-day Moving Average at 4008.97, where it remains on a sell signal. The final straw may be the crossing of the 200-day Moving Average at 3934.28.

Today’s op-ex shows Maximum Pain for options investors at 3965.00. Long gamma begins at 4000.00, while short gamma resides at 3950.00. Dealers may take a hit today.

ZeroHedge reports, “After 76 year old treasury secretary Janet Yellen blew up the market yesterday with her post-FOMC comments that regulators aren’t looking to provide “blanket” deposit insurance to stabilize the US banking system, stock futures have rebounded modestly on Thursday, while paring some earlier gains. S&P 500 futures were up 0.5% at 3990 at 7:45 a.m. ET while Nasdaq 100 futures rose 0.9%. Both underlying indexes fell the most in two weeks yesterday. The tech-heavy Nasdaq index flirted with a bull market yesterday after briefly rising 20% from its December low. US government bond yields have edged up after falling sharply on Wednesday when the Fed raised rates 25bps but also opened the door to a pause, while WTI crude futures are down 0.6% in early US session. The Stoxx Europe 600 Index slid 0.8%, falling for the first time this week before a rates decision from the Bank of England.

VIX futures pulled back to a morning low of 20.89, but have stabilized above 21.00. VIX is now on a buy signal with further confirmation above the mid-Cycle resistance and Triangle trendline at 23.72. VIX is scheduled to make its all-time high this year. The options investors speculating on a high of 180.00-200.00 may not be far off the mark.

Next week’s options expiration shows Max Pain at 21.00, while long gamma begins at 22.00. Short gamma is in short supply, as speculators become more bearish. Open interest is long up to 55.00.

ZeroHedge remarks, “When it comes to the Morgan Stanley house view, it’s not just Michael Wilson that is borderline apocalyptic, most recently warning on Monday of a “vicious” end to the bear market, one which drags stocks to fresh cycle lows: it appears that the bank’s global head of research, Katy Hubary, is not too far behind.

In her latest weekly closely read “Charts that Caught my Eye” report (available to pro subs here), she writes that there has been a lot of market debate over the past year about whether yield curve inversion, which historically has been a precursor of US recessions, meant that a recession was inevitable this time, in light of key idiosyncrasies in the current environment.

She then points to an “interesting section” of the bank’s Cross-Asset Strategy team’s latest dispatch which examines the confluence of five macro developments that, like inversion, are consistent with a strong economy that is starting to slow and leads to a sharp drop in risk assets:

- S&P 500 forward earnings are declining relative to three months ago;

- The yield curve is inverted (or has been over the last 12 months);

- Unemployment is below average;

- US Manufacturing PMIs are below 50; and

- More than 40% of US banks, on net, are tightening lending standards.

Pointing to the chart below, which shows that these five events tend to cluster just before major market crises (2007, 2001) that “all five are in place today, which is rare”

TNX futures are lower this morning as it attempts a retest of the Master Cycle low. The Cycles Model suggests window for a new low is closing, as today is day 260.00. The pullback still has the chance of matching the low at 33.69 over the next couple of days. The Model also shows that trending strength is due for a big comeback as early as this weekend with new highs possible through mid-April.

USD futures may have made their corrective low this morning at 101.55. The uptrend may be about to resume. The potential is for the USD to hit new highs by mid-April with the new trend extending to the end of April. Analysts are calling for an end to the USD (see below), but miss two important points. First, the US balance sheet is the cleanest on the clothesline. And second, war brewing on the European front may send capital to the US for safety.

ZeroHedge remarks, “A full guarantee of all bank deposits would spell the end of moral hazard and mark the final chapter of the dollar’s multi-decade debasement.

It’s said the cover-up is worse than the crime. With the latest banking crisis in the US, it’s the clean-up that could end up doing far more lasting damage. The failure of SVB et al prompted the FDIC to guarantee that all depositors will be made whole, whether insured or not.

The precedent is being set, with Treasury Secretary Janet Yellen commenting on Tuesday that the US could repeat its actions if other banks became imperiled. She was referring to smaller lenders, and denied the next day that insurance would be “blanket”, but given the regulatory direction of travel over the last forty years, this will inevitability apply to any lender when push comes to shove.

This marks the end of moral hazard and, ultimately, the final desecration of the Fed’s balance sheet.

The dollar is a liability of the central bank; therefore, this would mean further erosion of its real value, compounding the decimation of its purchasing power seen over the last century.”