9:52 am

BKX, our liquidity proxy, has a probable day left in its correction mode. Intermediate-term resistance is at 110.30, while the 38.2 % Fibonacci retracement is at 110..70. While it could go higher, time is running out for this move. The Cycles Model suggests the decline may extend to the end of March.

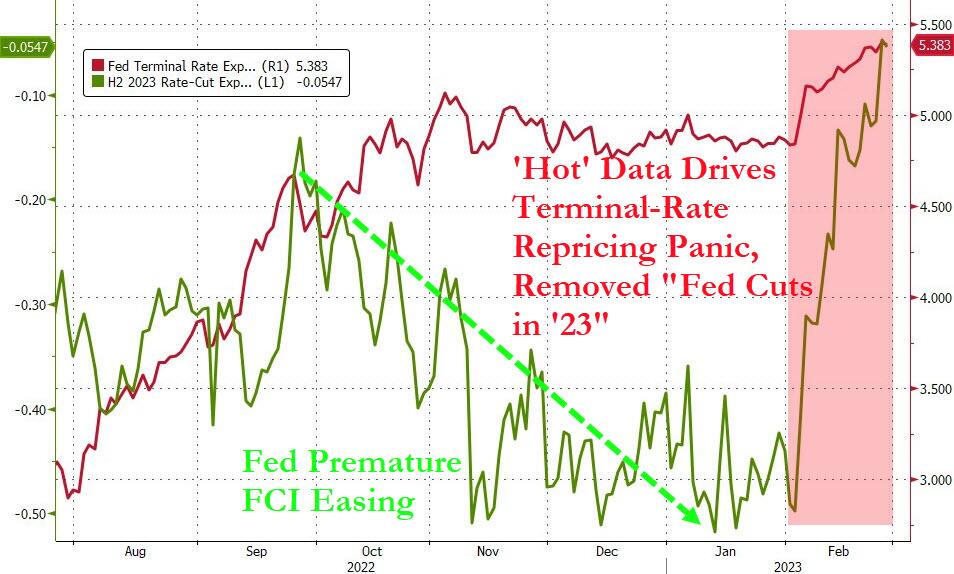

ZeroHedge remarks, “Nomura’s Charlie McElligott notes that the market has rightfully “trued-up” Fed terminal rate expectations in-line with spectacularly resilient growth data both domestically and internationally, following the FOMC’s multi-month “premature FCI easing” blunder which allowed for a reacceleration of “animal spirits” across inflation-, retail / consumption-, labor- and even survey- / “soft-” (particularly within Services sector) data, pouring gasoline on a still too robust economy, relative to their purported inflation-fighting aspirations.

Source: Bloomberg

The market had to reassess a ton of “mis-pricing” in Rates – needing to effectively remove the probability distribution which then implied the potential for Fed EASING later in 2023 – and we got it, with U3 / Z3 smashed lower, upper left Vols reaccelerating, a monster “de-inversion” in M3-Z3, and a power flattening in cash UST curves…”

8:20 am

I am planning on doing a final post tomorrow, but may be cut short due to scheduling issues. I have a 3-week tour of the mid-West starting tomorrow and lasting through the 21st.

SPX futures have bounced back above the 50-day Moving Average at 3979.19 to a morning high at 4003.00 thus far. The bounce may go to 4020.00-4040.00 and last through the morning. The earliest we may see a low is Wednesday March 1. However, the Wave structure is far from complete, leaving the current Master Cycle to extend at least to Friday or the following mid-week. The reason for this extension is the jobs report on Friday, which may cause a chaotic reaction.

Today’s options chain shows Max Pain at 3975.00. Calls eke out an advance at 3995, while puts show short gamma starting at 3950.00. Short interest is gathering steam and only needs a push to dominate the Cycle.

ZeroHedge reports, “US index futures jumped after suffering their worst weekly drop of 2023, as traders looked for fresh opportunities to buy stocks while assessing the outlook for growth. S&P 500 futures rose 0.5%, rising just shy of 4,000 by 7:45 a.m. ET after the underlying benchmark fell 1.1% in the last trading session. Nasdaq 100 futures rose by about 0.6% after the tech-heavy gauge tumbled 1.7% at the end of last week. European and Asian stocks also rose; the Bloomberg Dollar Spot Index turned red after retreating from the day’s highs, lifting most Group-of-10 currencies. Treasuries edged lower, mirroring moves in global bond markets. Gold was little changed, oil fell and bitcoin resumed losses after gains overnight.”

VIX futures are consolidating near the lower end of Friday’s trading range. There is a strong likelihood of extending its pullback to the 50-day at 20.53 or slightly lower today to 20.15, its 61,8% Fibonacci relationship. That leaves another 4.3 to 6.45 market days for a panic spike higher.

Wednesday’s op-ex shows Max Pain at 23.00. Short gamma is strong at 21.00 with over 11,000 contracts at that level. Meanwhile long gamma kicks in at 25.00. Next Tuesday’s op-ex (March 7) is early due to International Women’s Day on March 8. Max Pain is also 23.00, but long gamma begins at 24.00.

MarketWatch remarks, “The stock market’s fear gauge jumped suddenly this week, with volatility returning to equities amid heightened concern the Federal Reserve may raise interest rates higher than investors had been expecting, according to DataTrek Research.

“Equity vol is back,” said Nicholas Colas, co-founder of DataTrek, in a note Wednesday. “We are back in ‘2022 mode’, where it pays to watch the VIX.”

TNX has pulled back this morning to 39.04, but the Cycles Model suggests a possible spike in yields in the next 24 hours. The Cycles Model suggests the trend may peak the week of March 20. The following week may be chaotic, but it is not clear whether the uptrend extends or not.

ZeroHedge observes, “Longer-term bond yields continue to reflect an environment where inflation eventually comes back to target, and are not adequately pricing the likelihood it remains elevated and unstable.

PCE deflator data for the US is released today and we will find out how intact the current disinflationary trend is.

The trend looks set to end sooner than expected, with global inflationary forces picking back up as China recovers, reinforcing already sticky domestic inflation. If bond holders start to demand more premium to reflect a higher-inflationary world, yields will rise.”

USD futures have pulled back, but still within Friday’s trading range. Today is day 257 of the current Master Cycle, suggesting a high is in the making. Today’s reading still shows strength, suggesting a final trip to mid-Cycle resistance or the 200-day near 106.59.The corrective phase of the new Cycle may test the 50-day Moving Average at 103.56 or Intermediate-term support at 102.8. The behavior at that point may indicate a resumption of the rally through the end of April.