10:35 am

SPX is pausing near the late January low at 3949.06. Should there be a significant bounce (at least to the 50-day Moving Average), this formation may be activated with a target date of March 1.

As an alternative, there is the possibility of a bounce nearer to the mid-January low at 3885.54. The target for the lower Head & Shoulders would be 3575.00 after a bounce (again to the 50-day). Since the H&S target may be a minimum, we could see the SPX at the October low by the end of next week.

Remember, these are simply speculations based on the sxtent of today’s decline.

8:45 am

Good Morning!

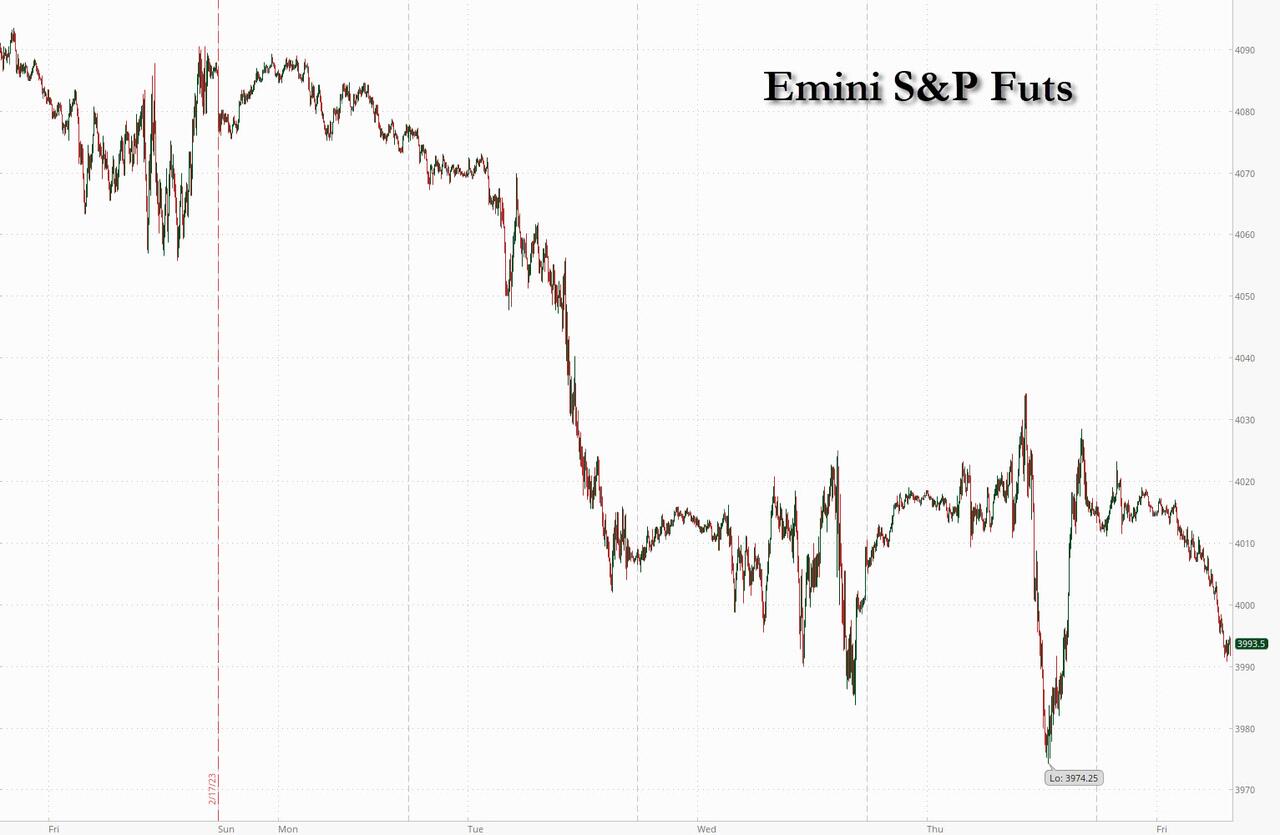

SPX futures dropped through the 50-day Moving Average at 3979.86, making a morning low of 3958.00. It may have broken through the descending trendline at 3965.00 and is likely to challenge the 200-day Moving Average at 3946.23. The Cycles Model calls for another 3-5 days of decline to its next Master Cycle low.

Today’s op-ex shows short gamma beginning at 4000.00. The longs have a toehold at 4005.00, but appear to be losing the battle for dominance.

ZeroHedge reports, “US index futures reversed Thursday’s rebound, and dropped as investors braced for data that may show accelerating inflation in the world’s largest economy. European stocks erased an earlier gain, while Asian equities fell on a quiet day for global markets. Contracts on the S&P 500 slipped 0.6% while those on the Nasdaq 100 fell 0.7% by 7:45a.m. ET. Friday sees the release of the personal consumption expenditures index, the Fed’s preferred price gauge, which is expected to show acceleration amid robust income and spending growth. The dollar rose amid concern over disappointing earnings and geopolitical tensions, and as the Yen tumbled after the confirmation hearing of Ueda’s proved to be far less hawkish than some expected.”

9:00 am

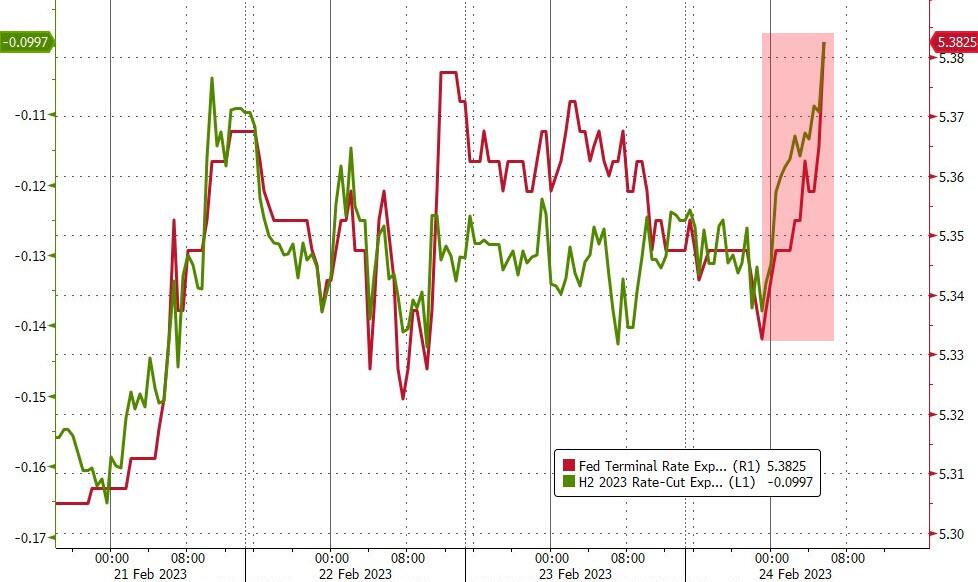

ZeroHedge remarks, “A much hotter than expected Core PCE print has sparked a dramatic hawkish response across markets.

Expectations for The Fed’s terminal rate has spiked to 5.39% and H2 2023 rate-cut expectations have dwindled to single-digits (just 9bps priced in)…

Source: Bloomberg

The market is now fully pricing in 3 x 25bps rate-hikes at the next three FOMC meetings…”

VIX futures jumped to a high of 22.55, but short of the lower Triangle trendline. VIX remains in flux whether the Master Cycle lo has already been made on February 15 (day 252) or may register a high sometime next week.

Wednesday’s op-ex shows Max Pain at 22.00. While sort sentiment is weakening, long gamma kicks in at 25.00 and remains strong up to 42.50.

TNX may be consolidating after yesterday’s breakout. The Cycles Model suggests the rally may continue to the week of March 20 with increased trending strength next week.

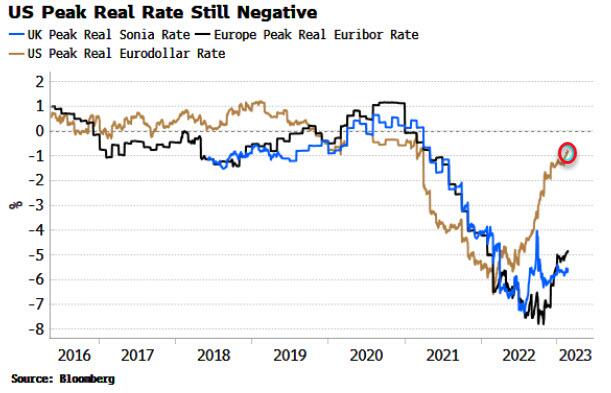

ZeroHedge remarks, ” The peak expected real Fed rate has risen but remains negative, while it remains considerably higher than peak real rates in the UK and Europe.

The Fed minutes on Wednesday underscored the bank’s intention to keep raising rates, with the market’s expectations of the peak Fed rate rising about 50 bps since the beginning of February.

However, this has still not been enough to take the peak real rate (based off CPI) to positive territory. Core PCE data just released for 4Q22, which was revised up to 4.3% from 3.9%, highlights the Fed’s challenge.

CPI fixing swaps see the real rate going positive in May, based on the implied rates from Fed Funds futures. But this assumes the Fed is able to hike as much as the market expects (55 bps across the next two meetings in March and May).”

USD futures are continuing to make new highs at 105.23 this morning. However, the Master Cycle may come to an end by mid-week. This is a puzzle, as TNX may continue its rally for another three weeks. It is possible that aversion to the USD may increase due to political errors being made.