8:30 am

Good Morning!

SPX futures have made an anemic bounce to 4013.00, and have since receded. The decline may continue, at least to test the 50-day Moving Average at 3977.20. The downside momentum is still palpable, though it may wait until the FOMC announcement at 2:00 pm. The Cycles Model suggests another week of decline, followed by a spirited bu choppy bounce perhaps lasting two weeks.

Today’s op-ex shows Max Pain at 4050.00, a level that is hotly contested by both puts and calls. Long gamma reigns above 4100.00, while short gamma becomes strong at 4000.00.

ZeroHedge reports, “After suffering their biggest one-day drop of 2023, US futures rebounded in muted trading on Wednesday, boosted by a drop in rates (the 10Y just hit a session low of 3.92% after rising as high as 3.97%) and weakness in the dollar, even as investors awaited further clues on the direction of monetary policy from the Federal Reserve’s minutes due out at 2pm today. S&P 500 and Nasdaq futures rose 0.3% and 0.4%, respectively, at 7:45am ET; sentiment was boosted by a CNBC appearance of the Fed’s “trial balloon” speaker, St Louis Fed president James Bullard, who was hawkish – saying he favors hiking rates to 5.375% as fast as possible, but not as hawkish as some had feared, leading to a sharp bounce in futures just after 7am. Yields dropped, as did the dollar, while oil, gold and crypto erased earlier losses.”

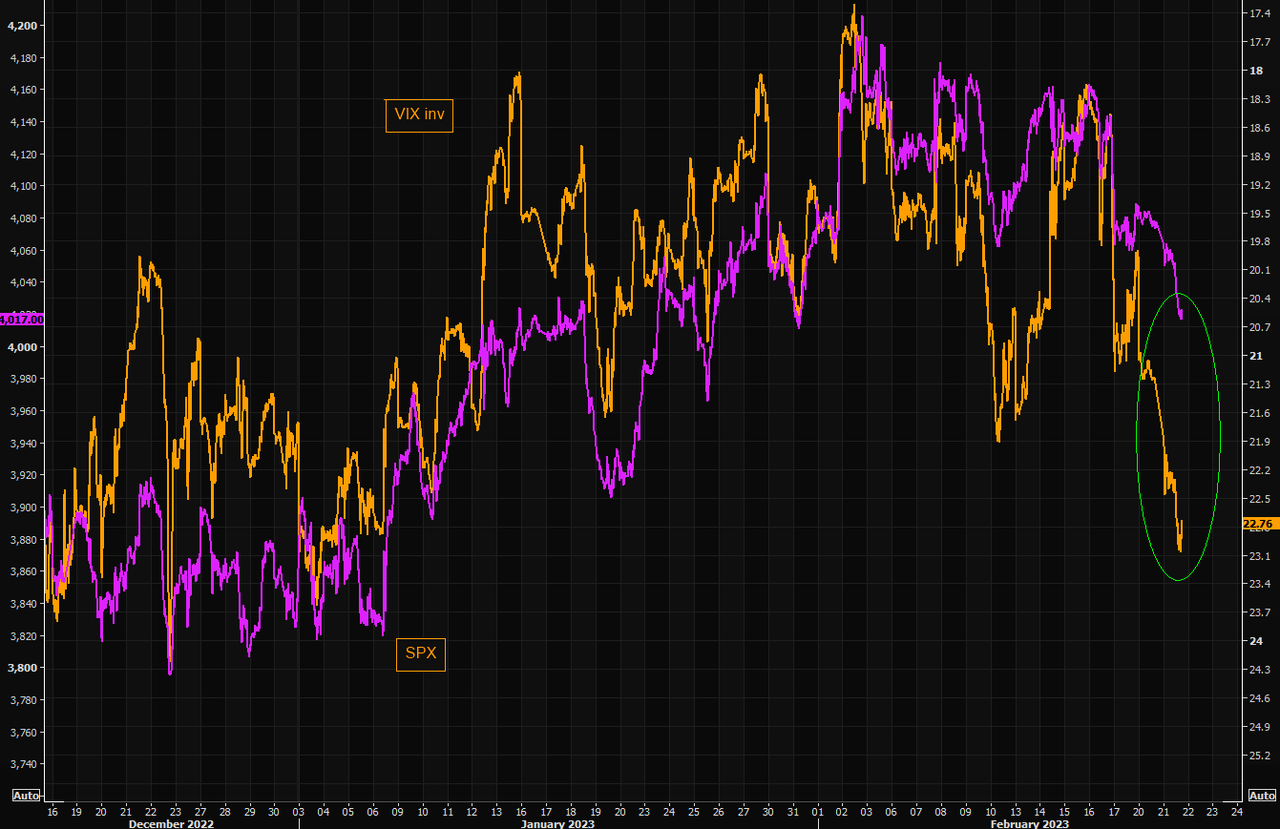

VIX futures are consolidating above the lower Triangle trendline near 23.00. There is a debate whether last Thursday’s low on day 252 was an actual Master Cycle low. The outcome of the debate may become clearer in the next week. In the meantime, trending strength is accelerating over the same period.

Today’s op-ex shows Max Pain at 22.00. Short gamma begins at 20.00, while long gamma erupts at 23.00, with strength extending to 40.00. There is no guarantee, but a hawkish Fed may push the VIX above its Cycle Top at 32.28.

ZeroHedge observes, “What price are you paying to panic

On February 2, VIX low this year, we outlined our logic on hedges/downside speculation in our thematic email “” (premium subs only, sign up ).

Vols have exploded since then and we are seeing early signs of panic in terms of pricing volatility. Most people tend to overpay for protection when things get “dynamic” to the downside as they only think about direction, but you need to consider what you are paying (implicitly) to “panic”? Make sure you don’t confuse direction with pace…Time for a thread on volatility:

1% move = 16% volatility

A 1% move in the underlying can be “translated” into a 16% implied volatility for that maturity. We are currently pricing the 1 month SPX atm around 21-22% implied volatility. That means the options market is pricing that SPX will be moving around 1.4% daily until expiration.

VIX – the new “dog”

The VIX (inverted) vs SPX gap has continued to widen as people decided that loading up on protection is a must.”

TNX appears to be consolidating after yesterday’s strong advance. A hawkish Fed may propel TNX to its Cycle Top at 42.79, despite being overbought. In any case, trending strength picks up next week, making a new high more probable. The Cycles Model calls for 4 more weeks of potential rally before the trend takes a rest.

ZeroHedge comments, “The yield curve is indicating a US recession could begin as early as June. The likely rapidity of its onset means the Fed will have to loosen policy sooner and by more than the market is currently pricing.

Recessions have gone out of fashion, with fears one will hit in the next year down sharply, according to BofA’s Global Fund Manager Survey. But the sugar high of some recent, rosy economic prints is not yet enough to derail the weight of evidence pointing the other way.”

ZeroHedge reports, “After two months of declines, in February the high yield on the 2Y auction exploded higher, and in the Treasury’s sale of $42 billion in 2Y paper completed moments ago, the US had to pay interest of 4.673%, up from 4.152%, and tailing the When Issued 4.670% by 0.3bps. The yield was also the highest going back to July 2007.

Amusingly, at the exact same time, today’s 52-Week Bill auction also closed. Its yield: 4.795%, so yes – the curve is now inverted at that 1Y-2Y kink. ”

USD futures are resting above the 50-day Moving Average at 103.28 with a possible retest of that support today. The Cycles Model anticipates a potentially explosive move higher into the end of the month. The declining Wedge offers the potential of a complete retracement.

Gold futures are consolidating above the 50-day Moving Average at 1829.30. While gold is on a confirmed sell signal, tha signal may be strengthened beneath the 50-day. The Cycles Model anticipates another 7 weeks of decline before this new trend gets a rest. The narrow trading bands imply a move strong enough to crash through the Lip of the Cup with Handle formation.

ZeroHedge opines, “By owning gold, investors are not necessarily hedging against a government default but ironically betting the Fed will increasingly misuse monetary policy to help the government avoid defaulting. That may not be the exact thesis gold investors signed up for, but there is ample evidence linking gold prices to Fed behaviors, as we will share.

Financial Mismanagement

Since 2008 government debt has risen twice as much as GDP, as shown in the first graph below. Individual and corporate debt have followed suit. The second graph below shows over $70 trillion of all debt in the U.S. economy, above and beyond annual GDP. That does not include the present value of future obligations, such as social security, which some budget experts argue can easily double the Treasury’s debt load. ”

Crude oil futures made a new low at 73.97 this morning, confirming the decline /sell signal. The Cycles Model suggests the current Master Cycle may wind up early next week. A new low, especially beneath the trendline at 72.00, may inform us whether the decline may continue or not.