1:15 pm

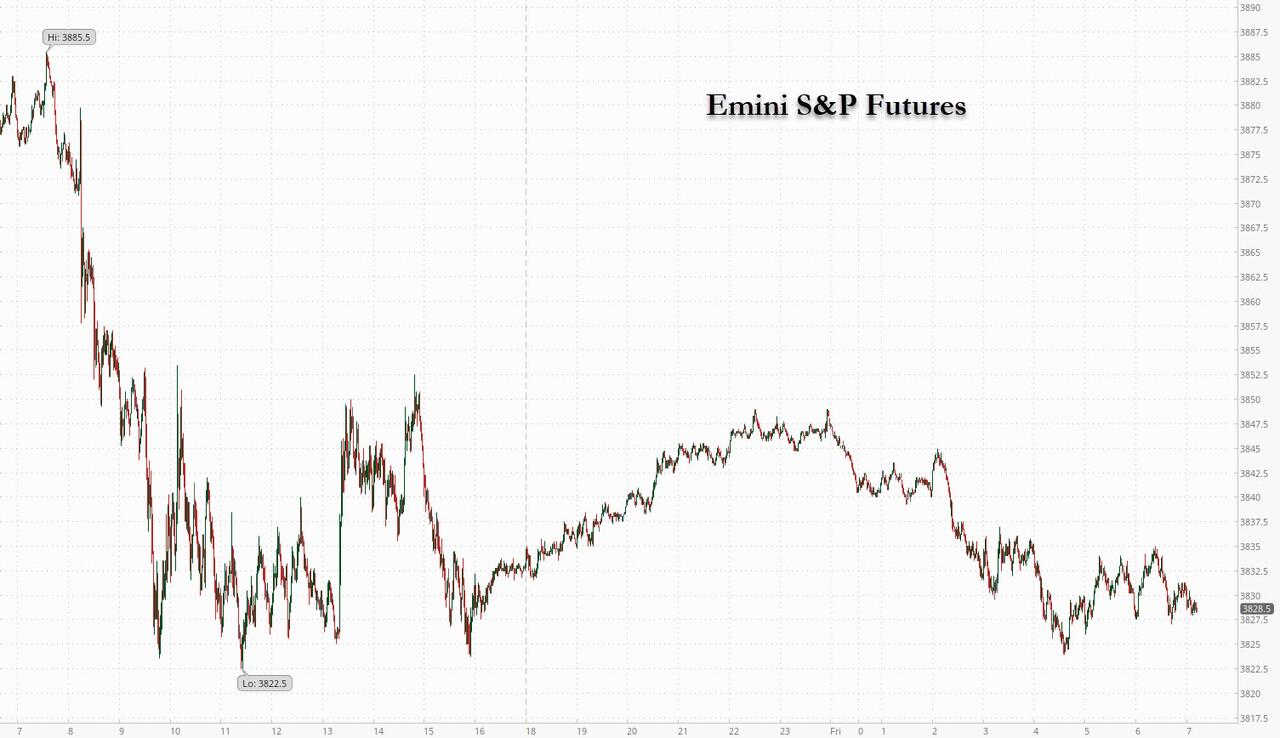

SPX made a new retracement high, but fell short of the 50-day Moving Average at this time. It has the potential of a reversal here. A Key Reversal may take SPX to or beneath 3800.00, so be prepared. I have not given a buy signal since the retracement has been too choppy, although long. The Triangle formation fits this description quite well and I have labeled it as such.

10:05 am

SPX gapped up to Short-term resistance at 3852.90, but failed to overcome it. It has since declined to 3809.66 and is hovering between support and resistance. Should Short-term resistance be overcome, the 50-day Moving Average and the Fibonacci 38.2% retracement lie at 3898.00. The market is now focusing on weaker wage growth.

8:55 am

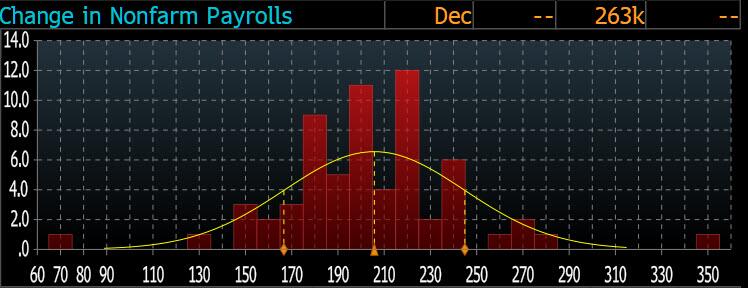

ZeroHedge analyzes, “There was a general sense of foreboding ahead of today’s jobs report, because as we wrote in our payrolls preview, several strategists noted that there was virtually no number that would be good for risk assets. As Goldman trader John Flood said, “whispers into December’s jobs print are creeping higher as we have already gotten 4 strong labor data points this week… We are still in a good data is bad for stocks set up but the new spin is that really bad data is also bad for stocks. AKA risk is skewed to the downside.” Meanwhile Bloomberg’s Heather Burke writes that the “median estimate for the change in non-farm payrolls is 202k versus a prior 263k and for the unemployment rate to stay steady at 3.7%. But the Fed’s own estimate is for the unemployment rate to shoot up to 4.6% this year. Until we get there, there is not going to be an alignment of demand with supply, which will compel the Fed to stay hawkish with no chance of a pivot.”

So with that in mind, here is what the BLS reported moments ago:

In December, payrolls rose 223K, which was down from last month’s downward revised 256K and also the lowest since the negative December 2020 print, but was above the consensus estimate of 202K.”

8:40 am

BLS reports, “Total nonfarm payroll employment increased by 223,000 in December, and the unemployment rate edged down to 3.5 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, health care, construction, and social assistance.”

7:45 am

Good Morning!

SPX futures bounced in the overnight session, only to fall back to the flat line by morning. The markets await the BLS Employment Situation Survey. due at 8:30 am. A better-than-expected report may cause a breakdown beneath 3800.00 confirming the decline that may continue through the end of January. A report that comes in at or beneath expectations may cause a challenge of the 50-day Moving Average at 3898.70.

Today’s op-ex shows Maximum Pain for options investors at 3810.00. Long gamma begins at 3850.00 while short gamma starts at 3800.00. A report exceeding expectations may break through the 3800.00 barrier and possibly break the hold that the options players have on the market.

ZeroHedge reports, “US equity futures struggled to maintain gains on Friday as traders awaited the December jobs report that will help chart the path forward for Fed monetary tightening. Contracts on the Nasdaq 100 and the S&P 500 were unchanged at 7:15am ET, erasing earlier gains sparked by a report that China was planning to relax restrictions on developer borrowing, and dial its stringent “three red lines” policy that exacerbated one of the biggest real estate meltdowns in the country’s history. US equities dropped on Thursday as separate data showed the labor market remained strong. European markets were steady as data showed euro-area inflation returned to single digits for the first time since August. Treasury 10-year yields steadied after climbing for the first time this week on Thursday following comments from Fed officials, while a measure of dollar strength climbed for a second day, as the yen fell to levels not seen in a week, after the Bank of Japan unveiled further unscheduled bond buying to control its yield curve.”

ZeroHedge further states, “As discussed earlier, the rate of payrolls growth is expected to cool (modestly in December, much more in Q1), with the street looking for the addition of 202k nonfarm jobs in December, which would be beneath the prior 263k rise as well as recent averages.

A couple quick points here: as Jim Bianco pointed out economists have consistently underestimated payrolls in 2022 and as shown below, the (first release) of the payrolls report has consistently beaten the median estimate for the past 8 months and 11 of the past 12.”

VIX futures are nudging against the 50-day Moving Average at 23.04 this morning. There is pressure for a breakout above the 50-day as trending strength starts to build today for the first time since mid-December. The Cycles Model calls for a peak during the week of the monthly options expiration on January 18.

Next Wednesday’s options expiration shows Max Pain at 22.00 Short gamma begins at 21.00, while long gamma starts at 25.00. At the moment, there is more conviction on the short side, but that may chaange with the Monthly Employment Report.

TNX rose after the BLS report, but remained beneath the 50-day Moving Average at 37.83. The trendline is near the Intermediate-term support at 36.67. Waiting for the breakout or breakdown.