9:32 am

The Ag Index is now in its final week of the current Master Cycle. It may rise as high as the mid-Cycle resistance at 492.99 as it is in a period of trending strength, but it may not last more than a few days beyond the holidays. Support lies at the 50-day Moving average at 462.87.

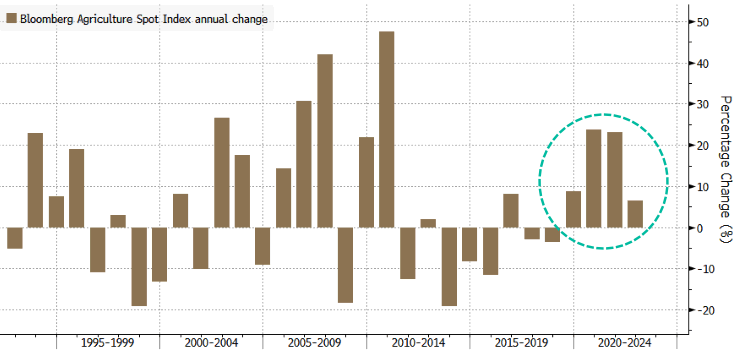

ZeroHedge observes, “Believe it or not, now is a great time to be a farmer. Agricultural commodities are set to lock in another year of annual gains, the longest stretch in decades, prompting higher farm incomes.

The Bloomberg Agriculture Spot Subindex, which tracks everything from corn, soybeans, and wheat to sugar and coffee, will lock in the fourth year of annual gains today.

Bloomberg said this would be the “longest stretch of annual gains since at least the early 1990s as drought and war cut production and erode inventories, keeping global food inflation simmering.”

High prices for crops and livestock indicate boom times for the US farm belt, making farmers, ranchers, and agricultural firms all winners after a decade of sliding net farm income.”

8:00 am

Good Morning!

SPX futures declined to the JPM collar at 3825.00 in the overnight session. The Cycles Model seems to agree by suggesting a quiet market for the next week or so. Upside potential may be limited by the 50-day Moving Average at 3887.82 or the 100-day at 3905.40. The 38.2% Fibonacci retracement value is 3891.40. The current hourly Cycle may last until (peak) Tuesday morning. However, the danger of a sell-off intensifies beneath 3800.00.

Today’s op-ex shows Maximum Pain for options investors at 3830.00. Long gamma starts at 3835.00, while short gamma begins at 3800.00, with the collar extending to 3850.00.

What is a collar? A collar is an options strategy that involves buying a downside put and selling an upside call that is implemented to protect against large losses, but that also limits large upside gains. The protective collar strategy involves two strategies known as a protective put and covered call.

ZeroHedge reports, “US equity-index futures slumped on Friday, tracking European stocks lower, after Wall Street’s best session of the month and denting hopes that Santa Claus would make a late appearance on the last trading day of the year and ease the pain for investors as global stock markets are about to close the books on their worst annual performance since the global financial crisis in 2008.

Similarly to European bourses, US tech led the decline – after leading yesterday’s gain – with contracts on the Nasdaq 100 down 0.7% at 5:26 a.m. in New York. The tech-heavy index enjoyed a 2.6% jump during the previous session, thanks in large part to a sharp bounce-back in Tesla shares. The Nasdaq has lost a third of value this year as tech stocks emerged as some of the most vulnerable to rising rates. Optimism spurred by weaker than expected continuing job claims data signaling some easing in tight US labor markets faded overnight, taking contracts on the S&P 500 about 0.5% lower, and appears to be headed for that infamous JPM Collar strike of 3835.”

VIX futures are higher this morning, but still within yesterday’s trading range. Trending strength may give VIX a boost above the Triangle formation as early as next week. Strength may intensify through mid-January.

TNX is rising above the 50-day Moving Average at 38.19 this morning as it completes Minor Wave 1 from the trendline. The current Master Cycle is due to end next week. However, the rally may intensify after a brief pullback following the Pivot.

ZeroHedge reports, “And so, after a strong 2Y auction on Tuesday and a medicore, tailing 5Y sale yesterday, we finally came to the last bond auction of 2022 when just after 1pm ET, the Treasury sold $35 billion in 7 Year paper in what can at best be described as a sloppy affair.

The high yield of 3.921% was just above last month’s 3.890%, and tailed then when issued 3.913 by 0.8bps. This was the third consecutive tail if far smaller than last month’s 2.7bps gaping tail.

The bid-to-cover of 2.454 was higher than both October and November, but below the six-auction average of 2.512.

The internals were stronger, with Indirects taking down 68.1%, the highest since August and well above the 66.0% recent average; and with Directs awarded 16.2%, or slightly below the recent average of 19.8%, Dealers were left holding 15.8%, above the average of 14.2%.”

USD futures may have risen above the trendline at 103.50 this morning. This indicates a potential move to test overhead resistance at 105.32 and above. Trending strength is due for a comeback during the second week of January, giving it an extra push above the 200-day and mid-Cycle resistance at 106.44..