3:30 pm

ZeroHedge observes, “Picking up on something we pointed out earlier, namely that after pricing in as much as 20bps of rate hikes in Q1, the market is now once again expecting a rate cut in the first quarter of 2023…

… Bloomberg’s Tatiana Darie writes that “stocks are soaring and bond yields are plummeting… as traders dial back expectations for Fed tightening, again betting on a rate cut arriving as soon as May 2023. They risk being disappointed.”

11:50 am

On Thursday I noticed what appeared to be an Expanding Triangle which is evidence of intervention (higher high, lower low, higher high). Point 5 is the high at 3736.74. Point 6 is at 3584.13. Point 7 is in process now. It may go to 3700.00 or higher before the bearish pivot. However, this may reinforce the target for the Cup with Handle formation.

6:30 am

Good Morning!

I have an engagement at 7:00 am that may last to 9:00 am, so here is an abbreviated pre-market comment.

SPX futures rose to 3608.20, testing the Lip of the Cup with Handle before resuming its decline. It may be trapped under the trendline, so it is important to keep that in mind. The decline may intensify over the week ahead. The current illustration implies a decline to 3400.00. However, an alternate view is even more bearish, especially because the bearish formations point to a much lower target.

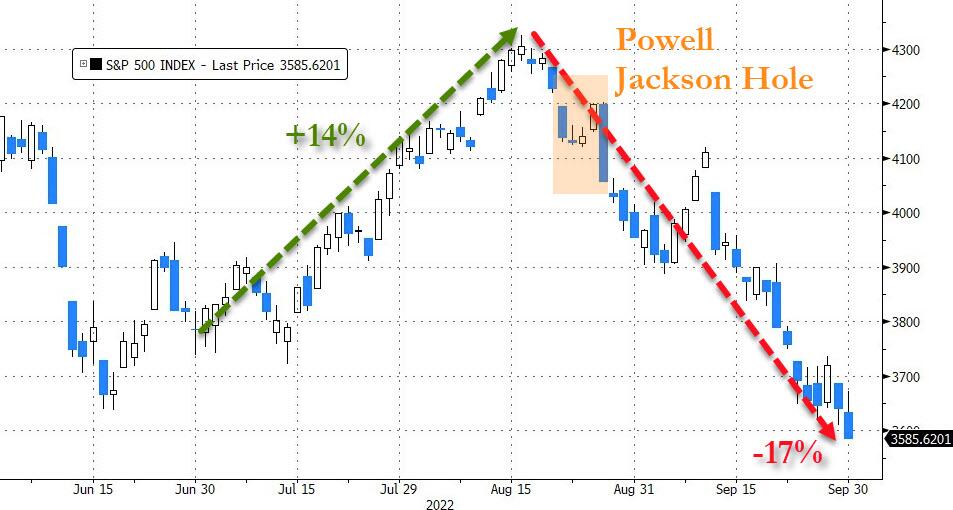

ZeroHedge comments, “Since Fed Chair Powell unleashed his short-and-sweet uber-hawkish comments in late August at Jackson Hole, market expectations for The Fed’s terminal rate (cycle high before pause or cuts resume) has surged hawkishly (adding 100bps of hikes).

However, as the chart below shows, the last week – as UK chaos erupted and spread to US equity and bond markets – there has been s dovish shift in market expectations for just how hawkish The Fed will be able to get before everything goes pear-shaped…

Powell’s speech also triggered a total puke in equity markets as all that ‘hope’ for a ‘Fed Pivot’ was dashed (prompting the greatest quarterly loss after a 10% rise since 1938)…

All of which brings us to the latest Bear Traps note by Larry McDonald, who has argued for months that Powell cannot get Fed Funds to 350bps and that belief that The Fed can achieve $1T of QT balance sheet reduction in 12 months is a childish fantasy.”

9:00 am

In today’s op-ex Mas Pain appears at 3665.00, while long gamma begins at 3700.00 and short gamma starts at 3650.00. There appears to be an effort in the morning futures to reach Max Pain.

ZeroHedge reports, “After a disastrous September, stocks have started off the new month of October – which at least historically tends to do much better than its predecessor – in extremely jittery fashion, with global stocks falling to a two-year low and US equity futures first sliding as much as 0.6%, before rising as much as 0.7% in what can only be described as an extremely illiquid market where Emini top of book liquidity is now at or below 1 million. Nasdaq futures were flat, as was the dollar while 10Y yields slumped perhaps in response to Mark Cabana’s latest note predicting a Fed “Twist” operation is on the horizon as the TSY market faces “breakdown.”

VIX futures declined to 31.25 over the weekend as it gathers strength for the next probe to the neckline at 40.00. VIX is still underperforming relative to the decline in the SPX. This may be a setup for a panic scenario, since investors are still talking about the “Fed pivot,” better known as the “Fed put.” There may be an attempt to push down the VIX as far as the 50-day Moving Average at 24.47, but it may not last.

In Wednesday’s op-ex, Max Pain is at 29.00, while short gamma lies just beneath it. Long gamma begins at 32.50.

TNX continues its correction from its recent brush with 4.00%. The Cycles Model suggests a strong uptick in Treasuries, but it may not last. Rates may resume their climb by the end of the week.

ZeroHedge comments, “Well, it finally happened: what we’ve been warning for the past year, namely that the Fed’s aggressive rate hikes will break something…

…did in fact break something, actually quite a few somethings: first the BOJ, then the BOE (just maybe Credit Suisse), and as Bloomberg’s Garfield Reynold writes, Treasury 10-year yields are surging relentlessly higher in a way rarely seen, as they have “finally” realized the Fed’s resolve to tame inflation.”