10:00 am

SPX is now testing short gamma zone beneath 3850.00. A plunge beneath that level confirms the continuation of the downtrend. The trendline at 3875.00 remains as resistance. Yesterday’s “bullish hammer” as reported by TME appears to be a fake out luring the inexperienced back into the market, only to be slammed today. The Cycles Model suggests strength in the SPX may be deferred until the end of the month, while VIX shows trending strength through the end of the week.

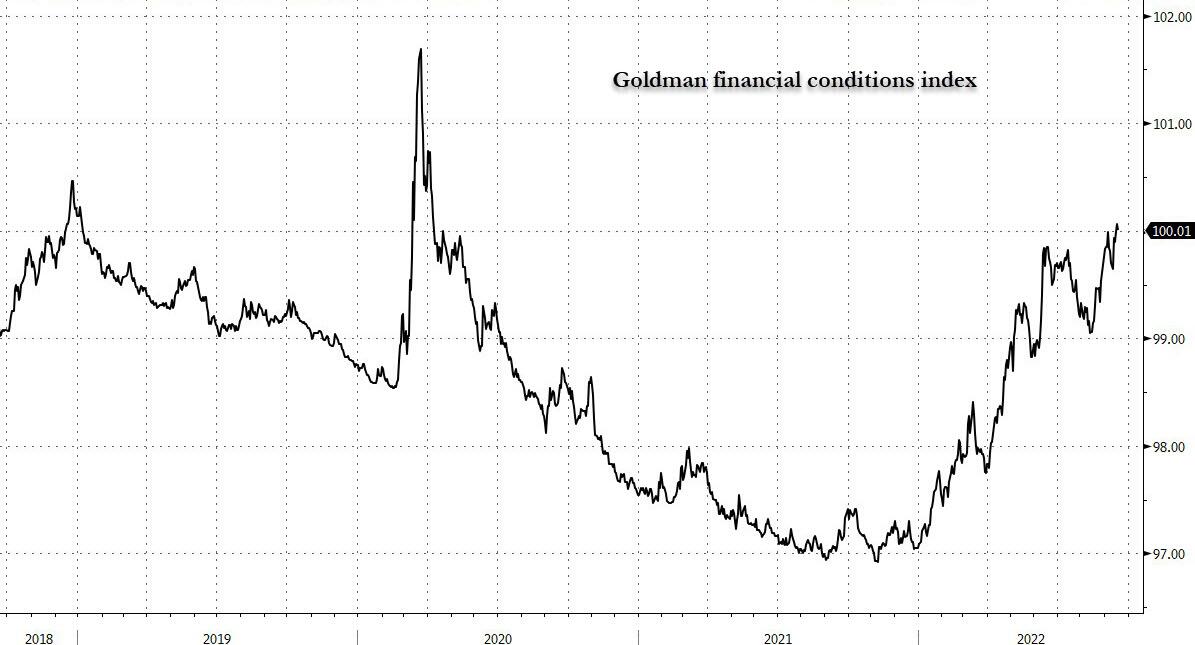

ZeroHedge remarks, “With the Fed successfully slamming stocks, corporate bonds and pretty much anything that isn’t the dollar, and tightening financial conditions the most in the past 2.5 years ahead of tomorrow’ 75bps rate hike…

… things went from bad to worse for the bulls today on surging Terminal-rate pricing – last seen at 4.49% down modestly from 4.52% earlier…

… on the back of today’s European disaster inflation prints, specifically German PPI exploding to the highest since the Weimar Republic on insane Energy costs…”

8:30 am

Good Morning!

I have been busy with chart analysis as the patterns become clearer. I had fallen to the temptation of putting Head & Shoulders and Cup with Handle formations at the purple trendline. However, the significance of that trendline is that it began in 1987. SPX fell beneath it in 2008 and the SPX remained beneath the trendline until 2021, its final blow-off. It fell beneath the trendline in May, ending a 35-year Cycle. The retest in August gives it finality. The uptrend is over. The decline is only beginning.

SPX futures have fallen back beneath the lesser trendline near 3875.00. Yesterday’s ramp in the final hour was not a new uptrend, but the positioning for a destructive third Wave.

In today’s op-ex Max Pain is at 3895.00. Dealers are still in control, but not for long. Long gamma begins at 3925.00. Short gamma is at 3850.00.

ZeroHedge reports, “Market sentiment was quite cheerful heading into the overnight session, with futures hitting a third-day high of 3,936 thanks to yesterday’ late day delta squeeze (plunge in VIX as both calls and especially puts were sold) but then it quickly soured after first German PPI came in at a mindblowing 45.8% (vs expectations of 37.1%) the highest on record since World War II…

…but what really spooked futures was the record hike by the Swedish central bank, the Riksbank, which pushed the repo rate higher by a more than expected 100bps to 1.75%, and even though the central bank eased back on terminal rate expectations, the market still saw the Riksbank surprise as potentially indicative of what the BOE and Fed may do in the coming hours.

As such, European stocks fell with US equity futures, giving up early gains, as traders braced for another supersized US rate hike amid rising anxiety the Federal Reserve could overtighten and raise the odds of a hard landing. Europe’ Stoxx 600 Index dropped 0.8%, paced by losses on real estate and miners as US equity futures also stumbled those the tech-heavy and rate-sensitive Nasdaq 100 underperforming S&P 500 peers. As of 730am, S&P futures were down 0.4% and Nasdaq contracts were down 0.5%. 10Y yields hit a fresh 11 year high as the dollar surged and gold resumed its slide.”

VIX futures rose to 26.69 in the morning session, but no new high has been made yet. Today is day 259 in the current Master Cycle. Thus far, VIX seems sleepy. However, today begins a period of strength that may extend over the weekend. This may confirm earlier comments that this Master Cycle may rise above the massive Head & Shoulders neckline at 40.00 this week.

TNX futures rose to 35.77 this morning with the cash market not far behind. The rise is inexorable. The odd part is that the Cycles won’t hit their period of strength until the end of the month! The Curren Master Cycle is due to continue until mid-November.

ZeroHedge observes, “A little over a month ago we warned that even prominent traders on Goldman’ flow desk were concerned by the market’s extremely dovish take of Powell’s July FOMC “pivot”, which had sent stocks soaring and financial conditions easing back to extreme(ly easy) levels, in effect undoing much of the central bank’ tightening cycle.

Understandably, it was around then that Goldman trader Matt Fleury asked “did Powell really mean to be so dovish?” noting that with inflation still just shy of double digits, “”has the Fed chair truly pivoted and is he now putting risk assets back at the top of the Fed wall of worry?”

Of course, following the Jackson Hole symposium, in which Powell’s brief 8-minute speech crushed the latest bear market rally, we knew the answer.”