9:57 am

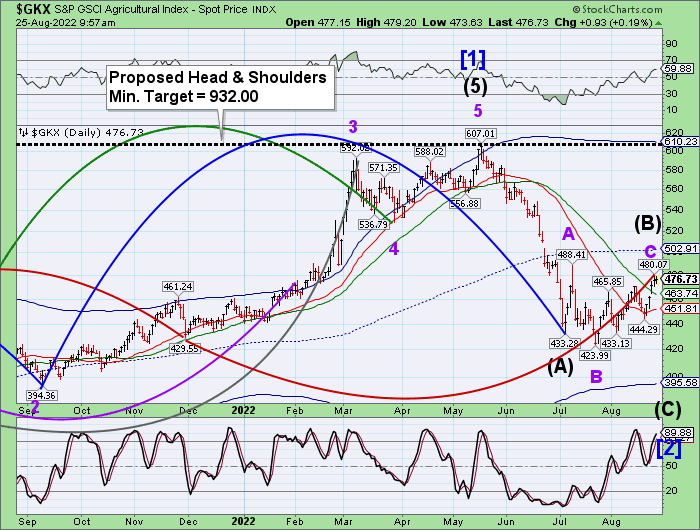

GKX has hit its Master Cycle high yesterday, on day 267. The next move appears to be counter-intuitive, as agriculture prices decline in the face of growing shortages. This may be due, in part, to declining liquidity. The Cycles Model suggests declining prices through mid-October. This may be a result of dealers selling off last year’s inventory and the lack of information on the true yield of this year’s crops. The Ag Index may decline as far as 300.00 before the next leg up.

ZeroHedge reports, “Major grain traders have drawn concerns over profiteering and speculation in global food markets, prompting calls for a windfall tax.

According to The Guardian, the world’s top four grain traders (Archer-Daniels-Midland, Bunge, Cargill and Louis Dreyfus, known collectively as ABCD) have seen record or near-record profits or sales, and are forecasting demand to outstrip supply until at least 2024 – likely leading to even higher sales and profits over that period. The four companies control between 70% and 90% of global grain trade.”

ZeroHedge further observes, “The Ukrainian Agriculture Ministry reported Tuesday that a total of 33 cargo ships carrying about 720,000 tonnes of foodstuffs have left Ukraine since a deal to facilitate the export of grain out of Ukraine’s Black Sea ports was implemented.

The numbers show that the deal between Russia and Ukraine that was brokered by the UN and Turkey and signed in July has been a success. Ukraine’s Agriculture Ministry said that in addition to the 33 ships that have left, another 18 are loading and are preparing to depart from Ukraine’s Black Sea ports.”

7:35 am

Good Morning!

SPX futures rose to an overnight high of 4185.20, but since have backed away from their retracement. There may be another probe lower with a potential target near the 100-day Moving Average at 4082.00 or possibly Intermediate-term support at 4066.13.

In today’s op-ex, Max Pain is at 4145.00, while long gamma begins at 4175.00. Short gamma starts at 4100.00. Dealers are walking a tightrope.

ZeroHedge reports, “Futures jumped overnight after China revealed its latest massive stimulus (which however is still woefully insufficient to prop up the country’s crashing housing sector) steadied nerves in the nervous wait for Fed Chair Jerome Powell’s key speech at 8am tomorrow.

Shortly after 2am ET, China stepped up its economic stimulus with a further 1 trillion yuan ($146 billion) of funding largely focused on infrastructure spending, support that analysts quickly agreed won’t go far enough to counter the damage from repeated Covid lockdowns and a property market slump. The State Council, China’s Cabinet, outlined a 19-point policy package on Wednesday, including another 300 billion yuan that state policy banks can invest in infrastructure projects, on top of 300 billion yuan already announced at the end of June. Local governments will be allocated 500 billion yuan of special bonds from previously unused quotas. However, as has been the case for the past 2 years with Beijing’s drip-drip stimulus, economists were downbeat on the measures, while financial markets were muted. The yield on 10-year government bonds rose 2 basis points to 2.65%. China’s CSI 300 Index of stocks rose as much as 0.6% before paring gains to trade up 0.3% as of 2:28 p.m. local time. A similar reaction was observed in US futures which initially spiked by nearly 30 points, reaching a high of 4187.5 before fading most of the gains; emini futures traded +0.6%, or 25 points higher, at 7:30am ET, while Nasdaq futures were up 0.85%. Emerging-market stocks also rallied the most in two weeks on the Chinese stimulus news, only to see gains fade. Treasury yields and a dollar gauge dipped, while the crypto space rose on China’s stimulus.”

VIX futures are probing lower, at 22.26 this morning. However, this may be the prelude to a show of strength this weekend with the VIX rising above its nearby resistance level at 25.12.

Yesterday’s op-ex cleared much of the negativity in the VIX. Next Wednesday’s op-ex shows Max Pain at 22.00 and long gamma beginning at 23.00. Short gamma has all but disappeared.

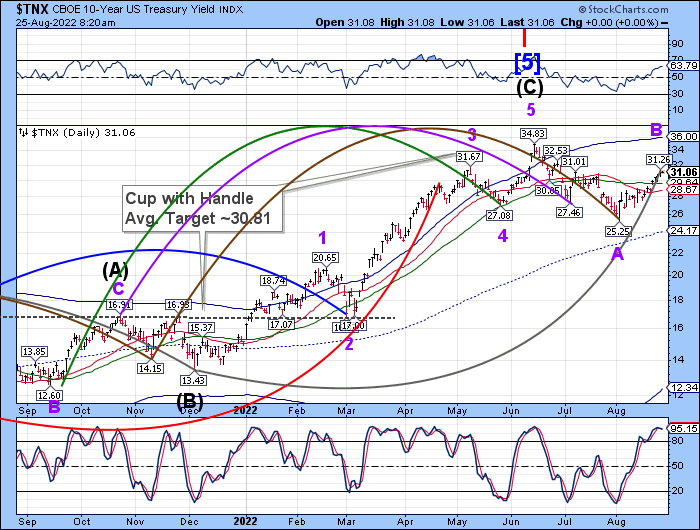

TNX has eased away from what may be the Master Cycle high yesterday, on day 264 of the former Cycle.

ZeroHedge reports, “After yesterday’s ugly 2Y auction moments ago the Treasury completed the week’s second coupon issuance when it sold $45 billion in 5Y bond due Aug 31, 2027, and which saw the yield surge to the second highest on record, up from July’s 2.860% to 3.230%, and just shy of the record 3.271% print in June; the high yield (74.56% allotted at high) also tailed the When Issued 3.220% by 1bp – this was the fourth tailing 5Y auction of the past five.

The bid to cover was ugly, slumping to 2.30 from 2.46 in July, and far below the six-auction average of 2.437. In fact, with the exception of June’s 2.28, today’s auction had the lowest bid to cover since Feb 2021.

The internals were also ugly, with Indirects sliding to 61.2% from 66.4%, although not that far below the recent average. And with directs taking down 18.2% (the second lowest since January), Dealers were left holding 20.6%, up from 16.8% last month and above the six-auction average 18.0%.”

USD futures are consolidating beneath their Cycle Top at 109.19. A pullback may be due, but the trend may be higher through the month of September.

WTI futures reached an overnight high of 95.67 as it overcomes Intermediate-term resistance at 94.39. The next resistance is the mid-Cycle at 96.50. A breakout above the mid-Cycle confirms the buy signal. The Cycles Model suggests a continued rally through the end of October.

OilPrice.com observes, “Some early investors in the Texas shale patch are now reaping the benefits of not giving up on the Permian basin over the past decade and sticking with their bet on oil through thick and thin—two oil price crashes, an increasingly louder global campaign for ditching investments in fossil fuels, and triple-digit oil prices following the Russian invasion of Ukraine.

Despite early hardships and thoughts of ditching the business of acquiring drilling rights across Texas when COVID crippled fuel demand in 2020, Cody Campbell, co-CEO at Double Eagle Energy, for example, has stuck with his guns, the Financial Times reports in a feature article. ”