12:33 pm

SPX is testing its modified Ending Diagonal trendline at 4135.00. The odds of yet another rally higher are slim, but may not be completely ruled out until SPX breaks down beneath trendline support. Additional confirmation of the breakdown occurs at the 100-day Moving Average at 4116.50. There may be a bounce soon, so patience is the byword.

ZeroHedge comments, “Investors’ fear of missing out is back, stoking a rally in equity markets that most strategists say has gone too far against a gloomy economic backdrop.

The Stoxx 600 has risen nearly 9% since hitting a 17-month low a month ago, though that doesn’t tell the full story of what has been a significant rebound for many cyclical sectors in a big turnaround from the first half. Tech is up 20%, automaker stocks have risen 16%, consumer and industrials each advanced about 15%.

According to Nomura cross-asset strategist Charlie McElligott, the rally has been “an angst-ridden pain trade” that’s leading to an “increasingly unstable FOMO-type behavior” and carries potential for further equities inflows.”

10:30 am

The structure in GKX is troublesome, but the Cycles Model may have the proper outlook. The current Master Cycle may end in mid-August with a potential new low near the Cycle Bottom at 392.82. The 61.8% retracement level is at 387.70. This may be due to the high profile reporting of the export of Ukrainian grain. Should this occur, it may be a deep value buy.

Reports of the decline are belatedly coming out after nearly three months of decline. However, the production of food worldwide is deteriorating.

- ZeroHedge reports, “The president of the largest farmers’ union in France has warned that a shortage of feedstock caused by severe drought may lead to a milk shortage.”

- ZeroHedge observes, “The effects of elevated food prices have rippled worldwide and forced governments to impose price controls and trade restrictions. Price increases are due to supply constraints driven by several variables, including high energy prices, geopolitics, and weather. Ukraine restarted maritime transport of crops to the rest of the world, forcing grain prices to slip, though the food crisis is far from over.We pointed out in April that the next challenge for the global food supply could be a plunge in rice production (read: here). Fast forward months later, and our suspicions appear to be right as India, the world’s largest rice exporter, has seen planting areas of the crop decline by 13% due to heatwaves and drought.”

- On Friday, ZeroHedge commented, “A video showing pigs eating a deceased pig on a farm in China went viral recently. Some of the pig farmers, working for a major Chinese financial group, said that the cannibalism occurred because of feed shortages. One expert believes that feed shortages are a reflection of bigger problems in China’s economy.”

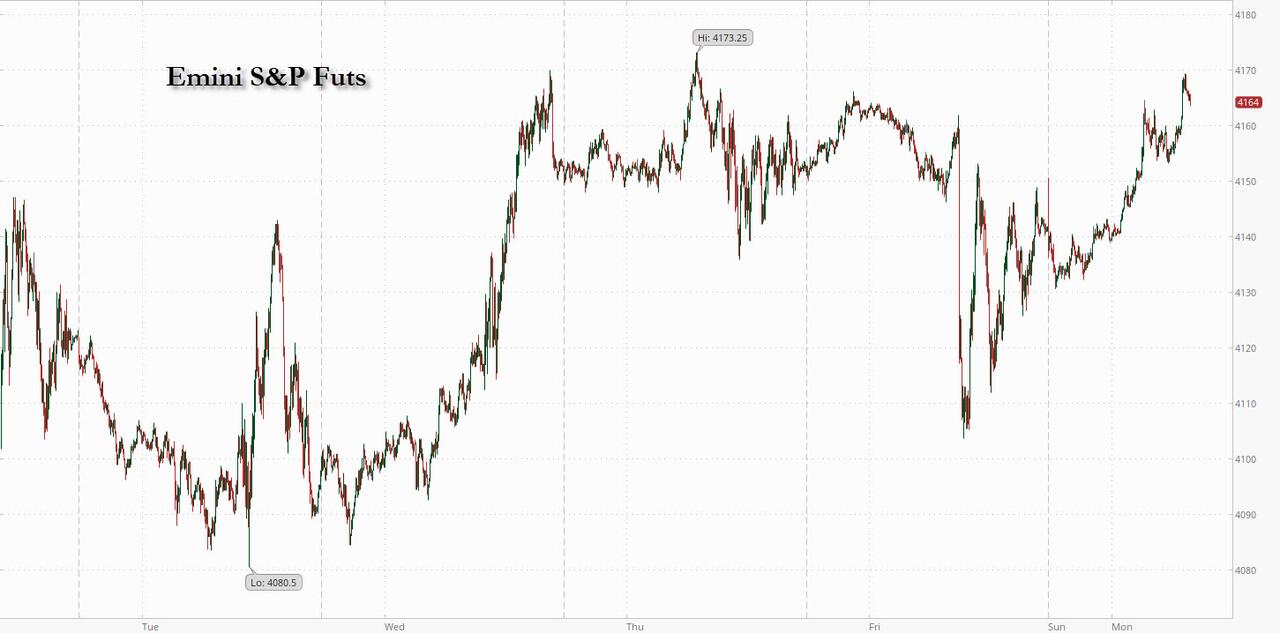

8:05 am

Good Morning!

SPX futures re flirting with a possible probe higher this morning, on day 259 of the Master Cycle. The new high this morning was at 4170.50, re-opening the possibility of SPX at 4200.00 – 4225.00. The retracement has been somewhat irregular, making it more difficult to follow. However, the Cycles Model did point out the last bit of strength for the SPX arriving over the weekend.

In today’s op-ex, Max Pain is again at 4145.00. Calls dominate above 4150, with long gamma beginning at 4180.00. Puts rule beneath 4140.00 with short gamma at 4125.00. This is a very tight market and there may be some gamma-driven fireworks.

ZeroHedge reports, “US equity futures rose to start the week as the “most hated meltup” continued just as we said it would over the weekend as stubborn bears are forced to cover and start chasing higher out of FOMO, while Treasury yields fell while investors assessed the path of monetary policy ahead of this week’s critical CPI data. Nasdaq 100 futures rose 0.7% while S&P 500 futures gained 0.5% by 7:30 a.m. in New York after the underlying benchmarks dropped on Friday following news that US job growth soared beyond expectations. Meanwhile, the yield on the 10-year Treasury dropped to 2.79% after soaring at the end of last week, while the dollar dipped and bitcoin jumped above $24K.”

VIX futures were higher this morning despite the rally in equities, reaching a morning high of 21.87 after being beaten down on Friday. The Wave structure is unreadable. As mentioned before, Wave Es are rogues.

Wednesday’s op-ex shows Max Pain at 22.00. The shorts (puts) beneath that are sparse, while long gamma resides at 25.00.

Bloomberg reports, “Rising volatility may be about to test the US stock market’s 13% jump from June lows.

That’s the picture painted by technical charts looking at the Cboe Volatility Index, a gauge of implied equity swings for the S&P 500 known as the VIX.”

TNX pulled back this morning after Friday’s surge higher. The rise in yields doesn’t appear to pose a threat, but a move above overhead resistance (50-day Moving Average) at 29.63 may paint a different picture for investors.

USD futures pulled back to test Intermediate-term support at 106.05 this morning. It is now on a buy signal after making its Master Cycle low last week. The Cycles Model suggests a 7-week rally, giving it the capability of retesting the July 2001 high at 121.21.

West Texas Intermediate Crude has consolidated this morning inside Friday’s trading range. It still has about two weeks of further decline in the current Master Cycle. The next support is the Cycle Bottom/ Broadening Wedge trendline at 66.14.

ZeroHedge remarks, “Oil prices have tumbled 25% since early June, driven by low trading liquidity and a mounting wall of worries: recession, China’s zero-COVID policy and real estate sector collapse, the US SPR release, and Russian production recovering well above expectations.

However, Goldman’s Damien Courvalin believes that the case for higher oil prices remains strong, even assuming all these negative shocks play out, with the market remaining in a larger deficit than we expected in recent months.”

Gold futures rose above 1800.00, but remained within Friday’s trading range. It appears to have made its Master Cycle high on Thursday, day 261. Once beneath the Lip of the Cup with Handle formation, it may have 5-6 weeks of decline ahead. I found it interesting that there are two Cup with Handle formations on this chart. The lower formation has extended from June 2020.