2:32 pm

BKX, our liquidity proxy, just gave us a sell signal. It has declined beneath the 50-day Moving Average at 106.43. Yesterday it made its Master Cycle high on day 265. The Cycles Model shows that the next Master Cycle low may not come in until September 30. This may be the 15th reason for an economic crash in the second half of the year.

ZeroHedge gives the other 14 reasons, “It looks like we are going to get official confirmation that a recession has already begun when the GDP number for the second quarter comes out later this week. But that isn’t what we should be focusing on. Yes, things weren’t great during the first half of 2022, but they are going to be significantly worse during the second half. Small businesses are starting to fail all over the country, a housing crash of potentially epic proportions has started, layoffs are on the rise from coast to coast and economic activity is really slowing down all around us. So if you think that things are bad now, just wait, because they will soon be a whole lot more painful.”

10:23 am

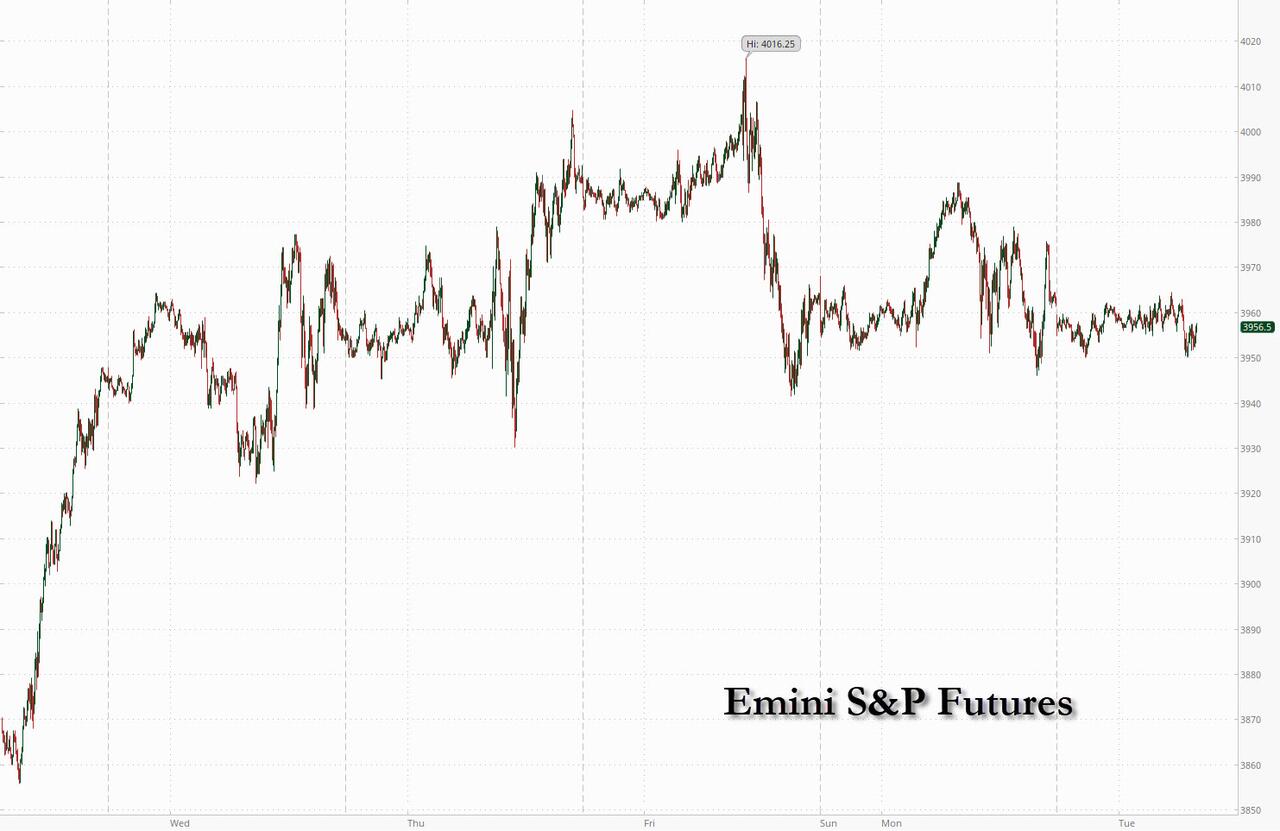

SPX is making new lows and potentially challenging the 50-day Moving Average at 3921.00. A decline beneath the 50-day confirms the sell signal.

ZeroHedge highlights Goldman’s change of tune, “Some very concerning market observations from Goldman trader John Flood discussing the real rot below the market surface:

Monday was the lightest volume session of the year with 9.32b shares trading across all US equity exchanges breaking previous low mark of 9.4b back on 7/11/22. YTD daily avg for shares traded across all US equity exchanges sits @ 12.5b. Monday was also the lightest notional trading session of the year w/ $392b trading vs ytd daily avg of $638b.

Our desk was a 3 on 1 – 10 scale in terms of overall activity levels. I am personally taken aback by how resilient mkt has been over the past few weeks.

I don’t see L/Os putting their ~$210b of cash to work. I am seeing them use pockets of strength to sell lower conviction more illiquid names in block form and raise even more cash. Last week our desk had 11 blocks which is noteworthy.

Positioning, sentiment and liquidity all incredibly depressed. Feels like we are due for a real pullback but clearly it wont be a straight line down.”

10:12 am

The Ag Index leaped higher with strength today as it emerges out of a very stretched correction. The Cycles Model calls for up to three weeks of rally prior to a pause in mid-August. Primary Wave [3] until late November or early December with the potential of more than 100% gains. And excellent long potential.

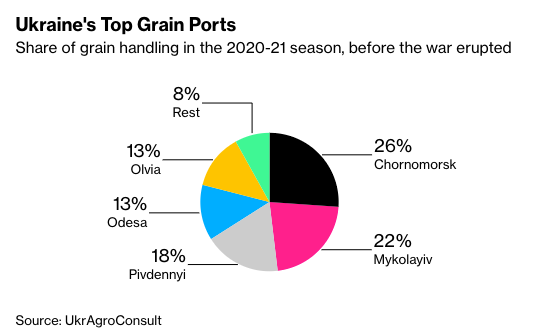

ZeroHedge observes, “Wheat prices soared Monday after Russia attacked the Black Sea trade port in Odessa, Ukraine, on Saturday. The strike comes less than one day after Ukraine and Russia brokered an export deal — mediated by Turkey — to export millions of tons of grains.

On Friday, officials from the U.N., Turkey, Russia, and Ukraine signed an agreement to reopen three ports, including Odessa, the country’s largest port. It’s a move heralded by these officials to alleviate a global food crisis.

Kremlin spokesman Dmitry Peskov insisted the weekend missile attack is “in no way related to infrastructure used for the export of grain.”

7:50 am

Good Morning!

SPX futures dipped to a low of 3947.30, within yesterday’s trading range. It appears to be marking time for the FOMC announcement. The top of the squeeze may have made its appearance last Friday. SPX is on an aggressive sell signal with confirmation beneath the 50-day Moving Average at 3921.54.

It should be no surprise that Max Pain in today’s op-ex is at 3965.00. Options turn bullish at 3975.00 and long gamma begins at 4000.00. Puts dominate at 3950.00 and short gamma may begin near 3925.00. Wednesday’s Max Pain is at 3945.00 with very little call action. Puts dominate beneath 3900.00.

ZeroHedge reports, “US stock futures dropped as investors braced for Wednesday’s Federal Reserve meeting, while Walmart’s surprise profit warning fueled concerns about the strength of US consumer spending. A barrage of earnings including notable misses by the likes of GM and a 3M guidance cut, did not help the mood. Contracts on the S&P 500 and the Nasdaq 100 were each down 0.4% by 7:45am in New York. European stocks rose driven by energy stocks amid a fresh surge in gas prices following Russia warnings of an imminent halving in NS1 shipments even as European Union countries reached a political agreement to cut their gas use. The dollar jumped and 10Y yields tumbled below 2.75% as a recession looks inevitable, no matter how Biden defines it.

VIX futures rose to 24.07, within yesterday’s trading range. A breakout beneath the June low is encouraging shorting the futures and ETFs.

Next Wednesday’s op-ex shows Max Pain at 29.00 with calls dominating above 30.00. Puts prevail at 28.00 and short gamma starts at 26.00. The crowd has really piled on to the short side of the ledger, which is typical near a Master Cycle low.

Bloomberg proclaims, “A recent bout of volatility in US equities has prompted some traders to think Wall Street’s so-called fear gauge should be higher. For Goldman Sachs Group Inc., that isn’t necessarily the case.

In fact, strategists led by Rocky Fishman recommend investors buy puts on the Cboe Volatility Index, effectively betting on relative calm in coming months. The VIX, a gauge of cost for S&P 500 options, historically tends to move in the opposite direction of the equity gauge 80% of the time. At one level, the team’s prediction for lower VIX implies a call for higher share prices.”

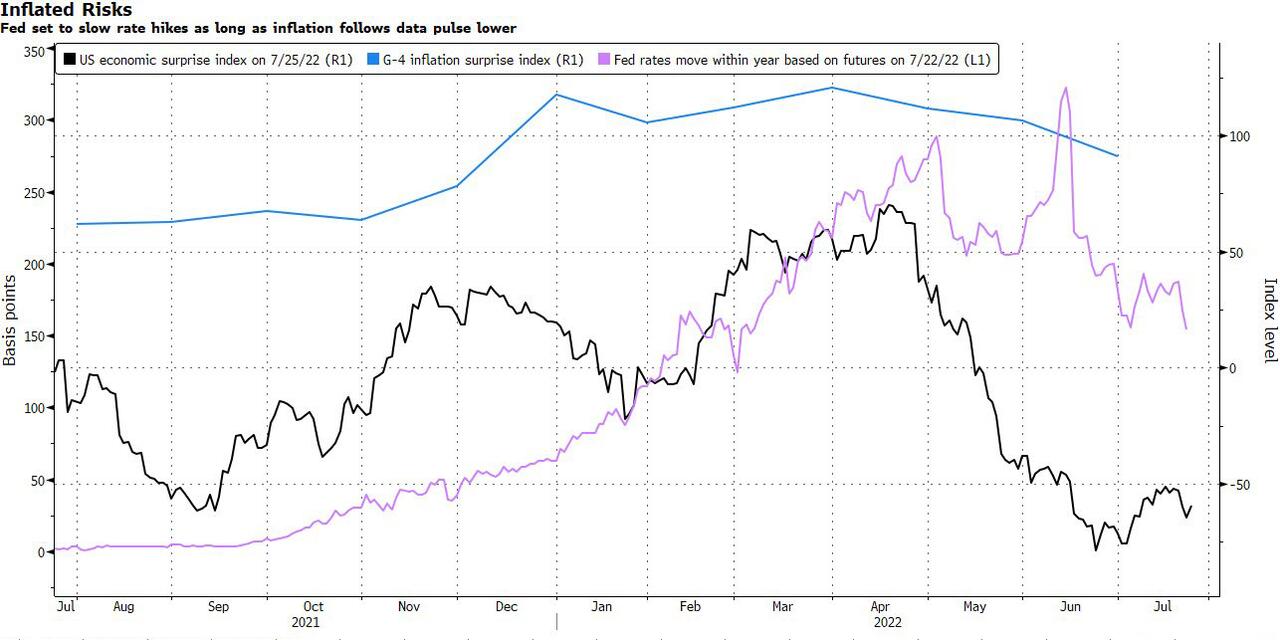

TNX is challenging last Friday’s possible Master Cycle low. Today is day 259 of the old Cycle, so there is a potential for making a marginal new low. The Cycles Model calls for 3-4 weeks of rally that may exceed the previous high. The next technical resistance appears at 53.16, made in 2007. Recession risk is high, but that won’t stop the Fed from hiking aggressively, since that is the only tool they have left.

ZeroHedge comments, “Risk Assets Are Hoping July Will Be Last Jumbo Fed Hike

The way yields and equities are dropping underscores the message from investors to the Fed: “You better slow down!”

The recession drumbeats grew louder after last week’s slump in US activity gauges and with rates traders pricing for the Fed rate to peak some time between November and February at about 3.3%. That’s going to make it very hard for the central bank to do anything but ease back, unless it wants to create real panic across markets.

The inflation-recession conundrum remains for the Fed, however, so such “tough love” can’t be ruled out. There’s been a strong undercurrent in Fedspeak and commentary from former Fed officials that the central bank has to be willing to risk recession to tame inflation if that’s what is needed.”

USD futures rose to 107.14 this morning, signaling a change in direction. The Cycles Model shows significant strength this week as it rises toward its Master Cycle high due during the second week of August.

Gold futures eased back toward the Cycle Bottom support at 1708.24 prior to a fresh rally higher. The weakness may not last, as the Cycles Model shows exceptional strength for the rest of the week. The next Master Cycle Pivot is due early next week.

Crude Oil futures rose to 98.98 this morning as the retracement continues for the next few weeks. The target for the retracement appears to be the 50-day Moving Average, currently at 108.41. A period of strength ignites later this week and continues with strength into the Master Cycle high, due in mid-August. A probable tax increase may be the fly in the ointment to sour this rally.

Bloomberg reports, “Big Oil is poised for a record-breaking $50 billion profit in the second quarter, but the industry’s stellar performance could contain the seeds of its own decline.

The soaring earnings are direct result of the high energy prices that have stoked inflation, piled pressure on consumers, raised the risk of recession and prompted calls for windfall taxes. Amid this political and economic turbulence, shareholders may have to temper their expectations for rising returns.”