3:25 pm

After the institutions sold this morning, there was an expectation that foreign and retail investors would pick up the buying. That did not happen and now institutions and mutual funds have stepped in to sell again. Unfortunately the dealers and hedge funds supporting the options market are under-hedged and must sell/short. This may not end well for them.

1:58 pm

SPX reached the 38.2% (futures) retracement at 3939.00 given this morning. There may be another attempt at the 38.2% (cash) retracement at 3958.00 before the close. Should stocks go down from here, there may be a firestorm of selling. 35% pf SPX short gamma comes off tomorrow, but only if SPX can rally back above 4000.00 in the next 24 hours. Otherwise all of those puts must be hedged by the dealers. I am not sure I agree with Charlie McElligot, but his comments are always interesting. It appears that the May 12 low was the Master Cycle low after all, as today would be day 266, 12 days into a whole new Cycle. That gives us a very short, 4.3-day retracement and the beginning of new decline lasting several weeks, should the market fail here.

ZeroHedge observes, “Yesterday was different.

Bond yields tumbled with stocks (they have tended to rise recently as stocks tanked)…

…and VIX spiked as stocks were spanked (it has been decoupling, exuding calmness for a few days until then)…

The change was catalysed by two factors:

1) “Hard-Landing” / “Recession” narrative keeps gaining-steam, so bonds are beginning to “work” as a risk-asset hedge, and

2) Yesterday’s VIX-piry (and tomorrow’s Op-Ex) removed much of the overhang suppressing vol, crushing hopes for some form of ‘stabilization’

So given the ‘change’, what happens next?”

11:15 am

I have had three failed attempts to log in to my brokerage account. On the third attempt, they messaged me back, asking that I call them (for my protection). My attempted call was refused by my cellular company, saying they were taking emergency calls only. I wonder if this is a nationwide phenomenon??? So far, the internet and email are still working.

10:29 am

SPX made a 22% retracement to 3923.90, then gave up the ghost in an epic failure of a retracement. I have often mentioned that the institutions make their largest play in the first hour of the day, then return in the final hour for the “mop up.” Having been unable to regain the morning losses, the big players must determine whether to go short or not for the rest of the day. Will this be a 10% down day?

8:30 am

Good Morning!

NDX futures dove to 11700.90, just above the previous low, which should put us on high alert for a retracement back to 12573.00. Remember, Friday is a huge options expiration day and all the indices are in serious short gamma. While yesterday’s decline was clearly impulsive, the powers-that-be may make every effort to redeem their predicament. The 50% retracement value is 12200.00. Should the bounce exceed that, the chances of an even higher retracement may prevail. I would prefer the bounce to stay beneath the 38.2% retracement at 12100.00.

SPX futures did similarly, pausing at 3858.90, just .03 above the previous low. Should the SPX break down further, the decline remains intact. However, should the low hold, the probability of a strong retracement arises. The 50% retracement is as 3974.00, while the preferred 38.2% retracement lies at 3939.00. Thus far the futures are lingering near the low, so we wait for a move to clarify the situation. Should the cash market gap down beneath yesterday’s close, it may be favorable to an extended decline from here.

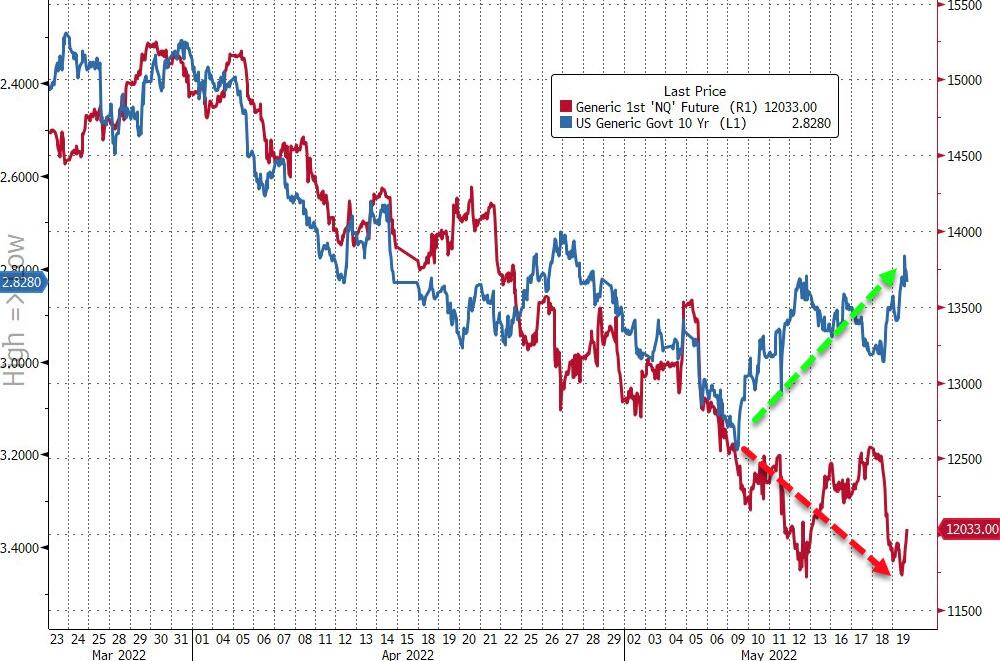

ZeroHedge reports, “US stock futures slumped again, extending yesterday’s brutal selloff that erased $1.5 trillion in market value on concerns about everything from slowing growth, to Chinese lockdowns, to soaring inflation and tightening monetary policy. Contracts on the S&P 500 were down 1.2% 7:30 a.m. in New York, having earlier dropped to 3,856, one point away sliding 20% from January’s all time highs, and triggering a bear market. The underlying index tumbled 4% on Wednesday, the most since June 2020, as consumer shares cratered after Target slashed its profit forecast due to a surge in costs. Nasdaq 100 futures were down 1.2%. 10Y TSY Yields slumped about 7bps, dropping to 2.833, while the dollar also dropped after yesterday’s surge; bitcoin was flat around $29K.

VIX futures rose to a new high at 33.11, possibly testing Cycle Top resistance, but not yet threatening the neckline near 40.00.

TNX opened beneath Intermediate-term support at 29.28, indicating a continued decline. The Cycles Model suggests a continued decline through the end of the month.

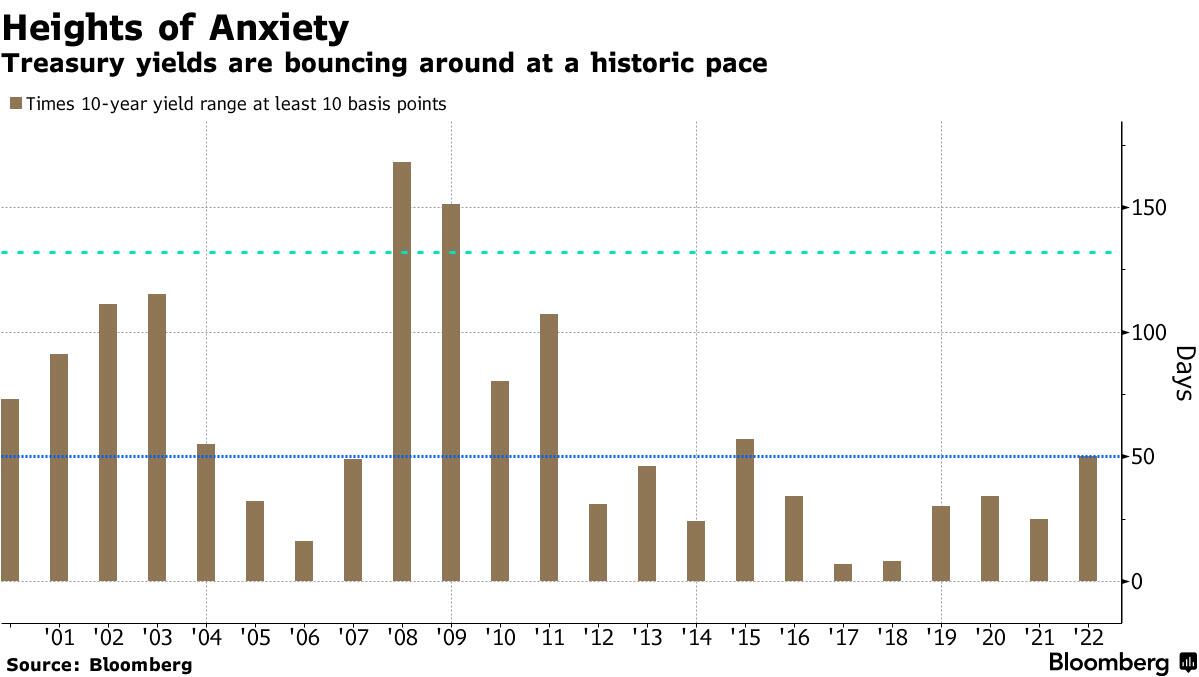

ZeroHedge observes, “There’s an alarming lack of conviction in the way markets are flip-flopping all over the place, and that’s a tribute to the epoch-making transformations occurring across the global economy.

In case you think that’s an exaggeration, consider what’s been going on in Treasuries, often cited as the world’s deepest market and a potential haven for investors panicked into prizing return of capital over returns on capital.

The past two days saw the benchmark 10-year yield jump 10 basis points and then drop by the same amount, as traders gyrated between inflation and recession fears.

USD futures sank to a new low at 102.95 this morning. The combination of lower confidence and lower yields are taking their toll on USD.

ZeroHedge remarks, “In a recent ‘Chart of the Day’ from DB’s Jim Reid, the credit strategist makes it very clear not only what comes next to the US economy (that would be stagflation for anyone who happens to be an idiot, or is a central banker, but we repeat ourselves), but also how much the consensus has moved for the US economy over the last year.

And while Reid would still not call real GDP growth at just below 3% this year “stagflation, he admits that the direction of travel is clearly moving in that direction, especially for 2023, which is when DB’s base case for a recession kicks in (to this day, DB remains the only bank which has recession penciled in as its 2023 base case; we expect every other bank to follow suit in the next 2-3 months).”