11:05 am

BKX has been in an overlapping, contentious decline from January 13, 2022. Although there may be different interpretations, the decline may be an extended one, with the worst at our doorstep. The new Master Cycle is not due to end until the end of June. Be prepared for the worst.

10:14 am

NDX is testing the Lip of the Cup with Handle formation near 13050.00. The warning of a quick and sharp reversal was appropriate, as one can see. SPX may not be far behind. Most analysts are not aware of the Cup with Handle formation. Thus, it is in little use in the mainstream. One of the features is that it is similar to the Head & Shoulders, which is in common usage, but with some differences. The main one is that the Lip is permeable and may be criss-crossed multiple times, giving the impression of no trendline at all, versus the Head & Shoulders, which has a fairly solid neckline. Once it is crossed, there is no going back. Since there is so little recognition of the differences, analysts often ignore the formation, to their detriment. Another difference is that the target is a Fibonacci calculation, which is often ignored, since it can be higher or lower than the Head & Shoulders target.

NDX is also nearing its Maintenance Margin requirement for many investors. Those on margin may soon be getting calls as losses exceed their maintenance margin. This, plus short gamma, may sound the death knell for may overconfident investors.

10:25 am

Note that the NDX has now crossed beneath the Lip and the decline is intensifying.

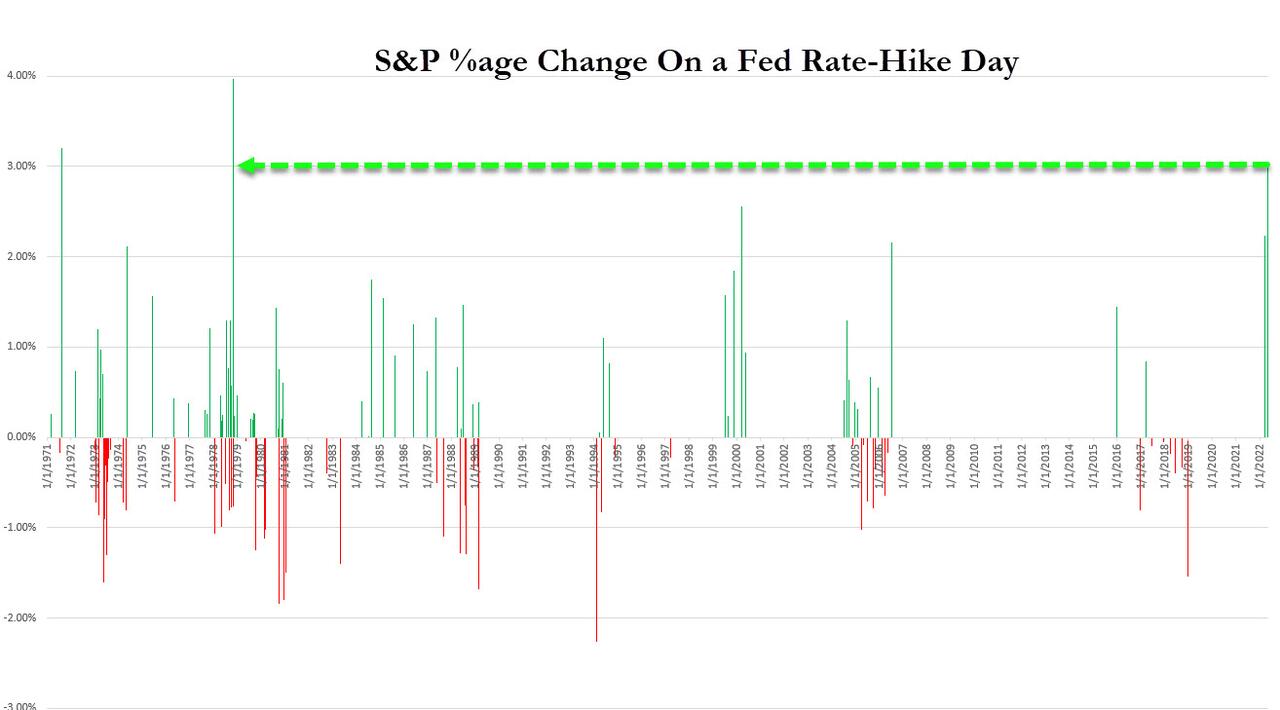

ZeroHedge remarks, “After yesterday’s biggest gain on a Fed rate-hike day since 1978…

It appears short-squeeze ammo and gamma has run out as Nasdaq pukes back all of its gains…

8:00 am

Good Morning!

Where are we? I have chosen to highlight the weekly chart to show the dimensions of where we may be.

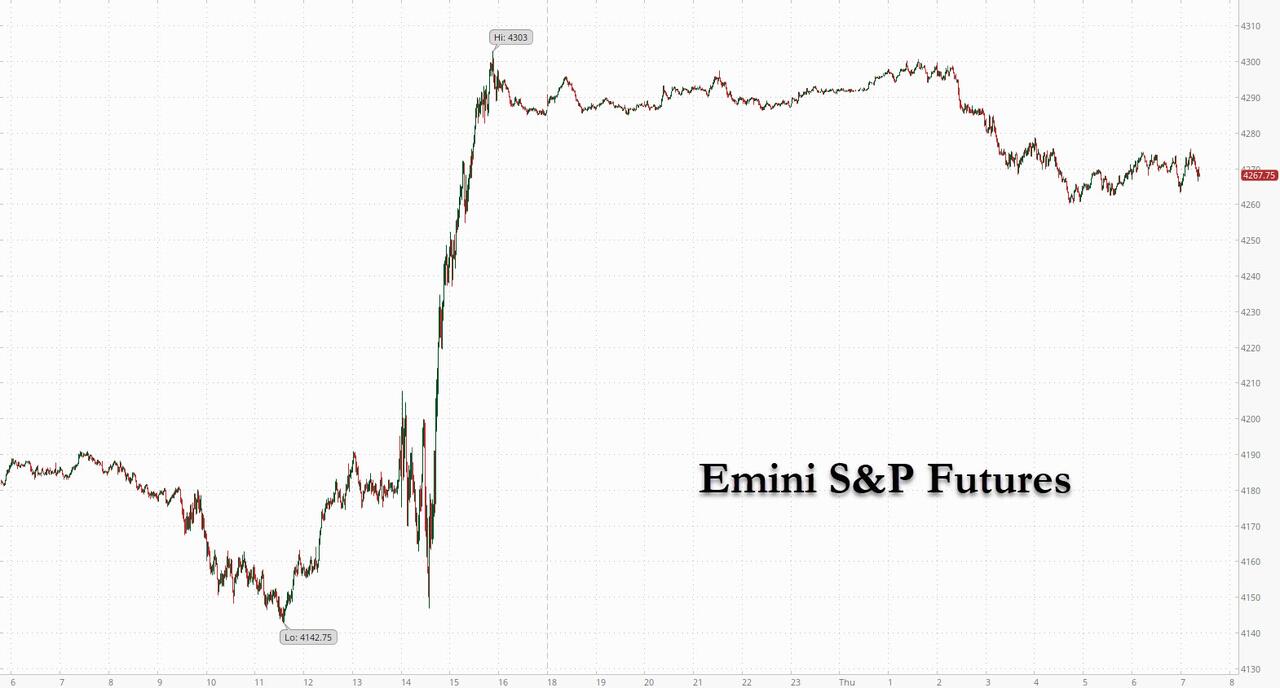

NDX futures promptly reversed after the closing bell and made a low of 13378.30 this morning. Yesterday’s bounce may have been a purely mechanical event, where a momentum ignition shook out the late comers to the shorting game. The bounce did not make the 38.2% retracement at 13684.26. Speculators have been buying short -term puts near the lows with a day-trading mindset, only to have lost it all while dealers have to buy back their shorted shares that would have covered those puts. The Cycles Model suggests a probable 12,9 more trading days to go in the decline as the next move may break through the Lip of the Cup with Handle formation. Note that the intended target may be the 10.5-year trendline, which was not broken in 2020. This target may be met later this month.

ZeroHedge observes, “David Wright is known for his ability to lead his funds through periods of intense volatility, like 2008, where his fund nearly broke even on the year while the major equity index shed half of their value. His losses during the COVID rout of 2020 were also relatively mild.

But those market ructions will likely be remembered as relatively staid in comparison to the selloff that’s just around the corner. According to Wright, who shared his thoughts on the market during an interview with Bloomberg, both of these periods – along with the dotcom crash – both had nothing on the crash that lies ahead.

SPX futures made a morning low of 4265.20 as it begins the decline through its Cup with Handle formation. In doing so, it may also re-enter the massive Orthodox Broadening Top that ultimately lands at or beneath Point 6 in late Summer. In this Master Cycle, the Cup with Handle formation makes its play, declining beneath the weekly Cycle Bottom at 2702.32. Investors think of buying puts as “insurance.” It’s not. It is simply a transfer of risk to the dealers and hedge funds. That is why we have short squeezes, to relieve the burden of carrying the brunt of the short speculation.

ZeroHedge reports, “After yesterday’s torrid, Powell-inspired meltup which saw the S&P soar the most since May 2020 (just days after its biggest drop since June 2020)…

… U.S. futures paused their surge after Jerome Powell eased fears that the Federal Reserve will unleash an even more aggressive tightening path and took a 75bps rate hike off the table. As of 745am EDT, S&P 500 futures dropped 0.6%, while Nasdaq 100 contracts fell 0.8%, as investors digested Powell’s vow to curb inflation, while acknowledging it could inflict some “pain” to the economy. In fact, an example of just what the Fed is fearing came earlier today when the BOE hiked 25bps as expected, but warned a stagflationary recession is be imminent as the central bank now expects GDP to contract while inflation rises double digits in the coming months, which is precisely what happens when central banks are far behind the curve. ”

VIX futures are moving higher, hitting 26.54 earlier this morning. The next step is crossing the neckline of the Head & Shoulders formation. The minimum Target for the H&S formation is in the mid-60’s. However, note that Wave [3] cannot be the smallest Wave and is often a multiple of Wave [1]. With that in mind, it may be possible to see Wave [3] well over 100.00 by August. Should that take place, another risk we may face is market closure or stiff restrictions on what we can do in the market, such as no shorting. Should that happen, it may make matters much worse, since that will leave no buyers at the lows to cover their shorts.

The NYSE Hi-Lo Index closed at -278.00 despite the rally. That is ample evidence of short covering rather than new money buying stocks.

ZeroHedge observes,

“Even the most circumspect friend of the market would concede that the volume of brokers’ loans – of loans collateraled by the securities purchased on margin – is a good index of the volume of speculation.”

– John Kenneth Galbraith, The Great Crash 1929

About a year ago, I noted that the “Index of the Volume of Speculation,” also known as margin debt, was in the process of putting in a blowoff top. The absolute level had reached record highs, suggesting that we were witnessing a degree of speculative activity that surpassed anything since the late-1920’s stock market mania Galbraith was specifically referring to in the quote above.

What’s more, it’s important to note that margin debt may be merely representative of a much larger use of leverage in things like asset-backed loans, call options, futures, leveraged ETFs, total return swaps, etc. All told, the total amount of leverage employed in the markets for risk assets may, in fact, be even larger than that earlier, ominous precedent.”

TNX made yet another marginal new high on day 274 of the Master Cycle. A reversal may be imminent. Once it takes place, the Cycles Model suggests a decline for the remainder of the month.