4:00 pm

NDX just took out the March 15 low at 13020.40 and is now officially in a bear market with a loss of 22.4%. The chances of a recovery are nil.

ZeroHedge observes, “As Elon Musk made yet more headlines today – by doing nothing today apart from tweeting this…

It appears someone decided he needed to be punished for daring to preserve free speech (oh the horror!) as TSLA shares tumbled over 11% today, raising questions from many on who was behind this move…

As Trey Henninger (@TreyHenninger) detailed, “If $TSLA stock hits $570, Elon Musk will be margin called on his Twitter purchase loan. If that occurs, he’ll have two business days to either pay the entire $12.5 billion margin loan, post $3.57 billion USD in CASH, or sell his $TSLAQ collateral shares. So, Soros has to short TSLA to 570 to kill the deal.”

TSLA’s tumble weighed heavily (given its weighting) on the major indices, with Nasdaq clubbed like a baby seal today, back below March’s lows (down 3.5% today)…Nasdaq’s worst day since Sept 2020

3:09 pm

SPX is pressing down on 4200.00 to see if it holds. Unfortunately, the declining impulse, consisting of 5 Waves, may finish near 4033.00, where Wave [v] achieves equality with Wave [i]. A probable alternative is that Wave [v] may be a multiple of Wave [i], due to short gamma beginning at 4200.00.

ZeroHedge (TME) is afraid to say the “B” word, “SPX approaching must hold levels

SPX is closing in on the huge 4200 level. The index has remained stuck inside the 4200/4550 range for months, with a few occasional over/under shootings. Note the 100 about to cross the 200 day moving average…not a great longer term development.

Source: Refinitiv

NASDAQ – to hold or not to hold

NASDAQ has been stuck inside the 13k/15k range since late January. We are currently at the big 13200 support, and we have seen tech under shoot down to the 13k level before reversing violently. Let’s see how this develops from here, but since the 100 day crossed the 200 day, things have been rather “fluid”.”

12:27 pm

SPX bounced at the 2-hour Cycle Bottom at 4203.00 just after the European Market close. It has since rallied and may attempt to reach Max Pain at 4310.00 at the close. However, the NYSE HI-Lo is at -230.00 and sinking fast, suggesting that the short covering may not last. This is a market to stay short for the duration, possibly 51.6 days from the March 29 high.

ZeroHedge remarks, “US equity markets are extending losses this morning, taking out yesterday’s lows and testing back down toward March lows…

As stocks catch down to the extremely hawkish reality priced into STIRs…

Bond yields are also tumbling and crypto is reversing alongside big-tech with Bitcoin back below $40k…

7:15 am

Good Morning!

All eyes are on China as the Shanghai Composite Index continues plumbing new lows. The Cycles Model suggests that, while there may be a temporary bounce in the next week, the decline may not be over until the end of May.

ZeroHedge observes, “The slothlike trade moving out of Shanghai has created a short supply of raw materials traveling on the all-important intra-Asia trade route. Countries that make up this trade pipe — Vietnam, Malaysia, Taiwan, Japan, Korea, Indonesia and Cambodia — have factories waiting on crucial raw materials needed to finish goods ranging from apparel and footwear to furniture.

This pipeline saw an expansion in the trade as more American importers diversified their manufacturing out of China as a way to work around the China tariffs.

But what this pandemic has revealed is even with this “manufacturing diversification,” the dependency on China has never been fully severed. Major raw materials such as jute, cotton, silk, wool and manmade fibers used by the textile and apparel industry are sourced in China. ”

NDX futures plunged to an overnight low of 13433.50 before rising back above the Cycle Bottom support at 13463.88. NDX is flirting with the bear market at 13400.00, a 20% decline from the top. Open interest in tomorrow’s options expiration is light with calls favored above 13500 and puts favored beneath 13250.00. The Cycles Model calls for at least three more weeks of decline, with growing trending strength.

The NDX Hi-Lo closed yesterday at -595.00, the lowest since mid-March.

ZeroHedge remarks, “The last time we heard from Morgan Stanley’s chief US equity strategist Mike Wilson one week ago, he was plumbing the depths of bearishness (as much as Morgan Stanley would permit him of course: as we have long noted, Bank of America’s own in house “Michael” strategist – that would be Hartnett – has been far more bearish), and he concluded that soaring inflation is no longer a positive catalyst for either earnings growth or stocks, to wit: the “positive effects of inflation on earnings growth have reached their peak and are now more likely to be a headwind to growth, (particularly as inflation forces the Fed to remain uber hawkish) and in that context, the growing rise in back end rates is having a meaningful impact on interest rate sensitive areas of the economy and market, like housing and impacting stocks.”

SPX futures declined to 4272.80 in the overnight markets, keeping above Cycle Bottom support at 4227.41. Yesterday, SPX attained the 17.2-day mark which I calculate to be one-third the 51.6-day decline that the Cycles Model proposes. A decline beneath the Cycle Bottom and the trendline at 4115.00 to 4120.00 activates the Cup with Handle formation with devastating results while liquidity tightens.

The NYSE Hi-Lo Index closed at -427.00 yesterday, a new low since the March 15 low. Tomorrow’s expiring options turn positive above 4320.00 and negative beneath 4305.00 with Max Pain at 4310.00. While yesterday’s cash market closed near 4300.00 as suggested, should SPX remain above the Cycle Bottom support at 4227.41, there may be another attempt to reach Max Pain at the end of the day.

ZeroHedge reports, “One day after stocks staged a remarkable rebound and closing well in the green after sliding as much as 1.5% (ostensibly after getting a boost from the latest bout of bearishness from Dennis Gartman), index futures are trading lower again despite another attempt by China’s central bank to reassure investors overnight that China’s sliding risk assets will rebound, with investors once again preoccupied by risks from aggressive monetary tightening. S&P500 futures contracts were 0.4% not too far off the worst levels ahead of a busy session of earnings releases including Google, Microsoft and Google; Nasdaq 100 futures declined 0.3%. Treasuries were steady and the dollar gained.”

VIX futures rose modestly to 27.74 in the overnight session. The 50-day Moving Average lies near the 50% retracement value. We should expect that level to be tested before moving higher.

ZeroHedge (TME) remarks, “They did it again?

Let’s see if the crowd managed doing “it” again: loading up on puts just when the market decides to bounce. People continue to buy protection when they must, not when they can. Think of “strategic hedging” like house insurance, you buy it before the house has started burning…otherwise the premium is very expensive. Chart shows the put call ratio vs SPX.

Source: Tradingview

VVIX remains “unimpressed” by the latest VIX surge

The gap between these two is at rather wide levels.

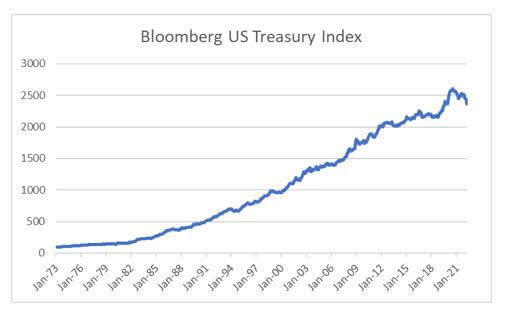

TNX continues its decline toward the Cycle Top support at 25.85. The final low may be the 50-day Moving Average, currently at 22.89. The reason for this is that the next Master Cycle (low) is anticipated for the end of May. UST is beginning a rally due to investors’ knee-jerk reaction of buying bonds while stocks decline. While there may be some merit in that move, it may not last.

ZeroHedge observes, “If I look at markets through the lens of financial history from 1970 onwards, I should be telling you to buy bonds. As Raoul Pal would say, “Buy bonds, wear diamonds” . Why? Well basically, buying treasuries has rarely lost you money. 2022 definitely stands out at a weak year for US treasury investing, but only after very strong returns during the Covid crisis.

Bonds have been a fantastic asset over the years. Good returns, with limited drawdowns. The financial market view, and one seemingly endorsed by central banks, is that central bank independence and vigilance was the cause of falling inflation and bond yields. The corollary of this view, was less central bank independence and less vigilance would eventually cause inflation, and rising bond yields. So if you were going to be bearish on bonds, then Japanese bonds were the bonds most fund managers chose to short. This was of course very wrong, and most of these funds and fund managers have left the industry, which is why short JGBs trade earned the moniker “widowmaker”.

USD futures have reached 102.00 in a classic throw-over on day 270 of the Master Cycle. The Cycles Model shows trending strength possibly ending early next week, if not sooner.