2:44 pm

SPX is now beneath 4400.00 and deeper in short gamma territory. There may be a final push as high as 4471.00 made this morning to complete the corrective pattern in an expanded flat correction during Wednesday options expiration. Once completed, the next move lower may take out the March 14 low. Thursday may be aa different ballgame.

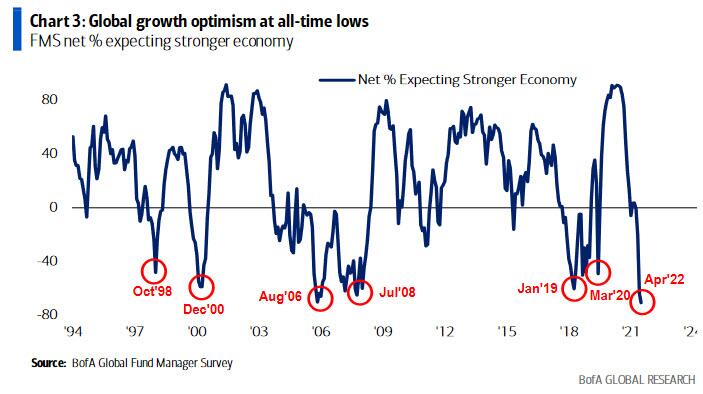

ZeroHedge comments, “One month after the March Fund Manager Survey was downright “apocalyptic” with the majority seeing a bear market and stagflation, and with optimism plunging to levels right before Lehman, today Bank of America published the latest, April FMS (available to pro subs in the usual place) in which the bank’s doom-and-gloomy Chief Investment Strategist Michael Hartnett found that his view is shared by even more Wall Street professionals, because the survey which polled 329 panelists managing $929 billion in AUM, found that global growth expectations plunged even more compared to last month, and dropped to fresh all-time lows (net -71%) …

… even as the percentage of those overweight equities remains stubbornly high (expect this number to slide in the coming weeks alongside stocks) and as BofA notes “The disconnect between global growth and equity allocation remains staggering. Investors got slightly more bullish on equities. Though still at depressed levels, equities are nowhere near “recessionary” close-your-eyes-and-buy levels.” As a reminder, we first flagged this “rare disconnect” back in September, and since then it’s only gotten worse.”

8:00 am

Good Morning!

NDX futures bottomed out at midnight at 13897.90 before making a bounce. This morning they have surpassed 14000.00 and may retest the 50-day Moving Average at 14330.93. What was support two days ago may become resistance. Should it surpass the 50-day, we may see a reprieve from the decline through the rest of the week.

Wednesday and Thursday are back-to-back options expiration days. While Wednesday’s options expiration is light, Thursday’s expiration favors puts beneath 14150.00 and short gamma may prevail beneath 14000.00.

ZeroHedge notes, “Hedge fund positioning: Back to lows. 0%-tile

Equity long/short hedge fund leverage is back to mid-March lows. Gross and net leverage both fell about 3% since the end of March which puts both at the 0th %-tile on a 12M basis with gross at the lowest since May 2020 and net at the lowest since September 2020.

Source: JPM Prime Brokerage

Puke in a Pic

In N. America we’ve seen selling for weeks now and the 4wk net flows z-score is around a -3z level after touching as low as a -4z level in the middle of last week.

Source: JPM PB

The NYSE Hi-Lo Index closed yesterday at -245.00 at day 256 of the Master Cycle. Regardless of the potential bounce today in share prices, a further decline in the Hi-Lo Index may indicate further weakness through the rest of the week.

ZeroHedge reports, “Having warned the world to expect “extraordinarily elevated” levels of inflation due to “Putin’s Price Hike”, The White House is likely in shock this morning as headline CPI rose 1.2% in March (vs +1.2% MoM) which sent the headline CPI up a shocking 8.5% YoY (vs +8.4% YoY exp and +7.9% prior) – the highest since 1981.

Source: Bloomberg

The 1.2% MoM rise is the biggest since Sept 2005 and CPI has risen for 22 straight months.

However, Core CPI (ex food and energy) rose just 0.3% MoM (below the +0.5% expected) and was up 6.5% YoY (above Feb’s 6.4% but below the +6.6% exp).

The shelter index was by far the biggest factor in the increase, with a broad set of other indexes also contributing, including those for airline fares, household furnishings and operations, medical care, and motor vehicle insurance.”

ZeroHedge comments, “On the basis that the CPI prints were “not as bad as they could have been”, US markets have reacted as if The Fed can step back from its hawkish stance and all will be well in the world.

Rate-hike expectations have eased modestly for the year… although the market is pricing in a 97% probability of 50bps hike in May(up from 92%)…

SPX futures also declined to 4387.20 by midnight, only to bounce in the morning back above 4400.00. The 50-day Moving Average is at 4424.85 and may be challenged this morning. Should it go higher, strong resistance lies at the mid-Cycle line at 4506.37.

This week’s shortened calendar brings heavy put and call positions every 50 points with calls edging out the puts above 4450.00 and puts prevailing beneath 4400.00 with very large positions on both sides up and down the scale. this may be a difficult options week to evaluate.

ZeroHedge reports, “US index futures were flat on Tuesday, rebounding off overnight session lows as investors braced for red hot inflation data which the White House yesterday called “extraordinarily elevated” and which will likely boost the argument for aggressive monetary tightening – perhaps even a 75bps or intermeeting rate hike – despite a looming economic slowdown. Nasdaq futures were 0.2% higher, while S&P futures were flat after dropping as much as 0.5%.”

VIX futures rose to 25.36 at midnight, but have retreated since then, especially after the CPI print. The Cycles Model allows the VIX to correct down to the mid-Cycle support at 21.19. However, it indicates a probable explosion of strength over the weekend, suggesting a resumption of hostilities in the Ukraine during the Holy Week of Easter.

TNX pulled back this morning from its new high as it takes a breather. The Cycles Model exhibits too much strength for a sustained or significant pullback for at least another week.

USD futures are consolidating within Monday’s trading range. Today is day 256 of the Master Cycle A reversal may be made as USD crosses beneath the Cycle Top Support at 99.40. It may happen at any time.