8:30 am

The Shanghai Composite Index rallied to 3260.17 before easing back, closing the gap. With six weeks to go to the next Master Cycle Pivot, there is little or no chance of recovery. While the bounce looks impressive, it is primarily short covering based on Xi Jinping’s jawboning.

ZeroHedge comments, “Calming words from Chinese President Xi Jinping’s right-hand man Liu He helped spur one of the most-dramatic turnarounds of Chinese and Hong Kong stock markets in history. The verbal intervention, coupled with possible follow-up policy support, may mark a market bottom, if history is any guide. Beijing’s policy put is still alive. “

SPX closed yesterday exactly at its options expiration Max Pain zone. (I wonder how they do that?) Futures have since declined to 4329.70 before a small bounce. Friday’s expiring options turn negative at 4330.00 and gamma goes short beneath 4250.00. There are $3 trillion in nominal options expiring tomorrow which are pretty evenly divided between puts and calls. Today may mark the top of a 4.3-day decline aiming for the Cup with Handle formation target.

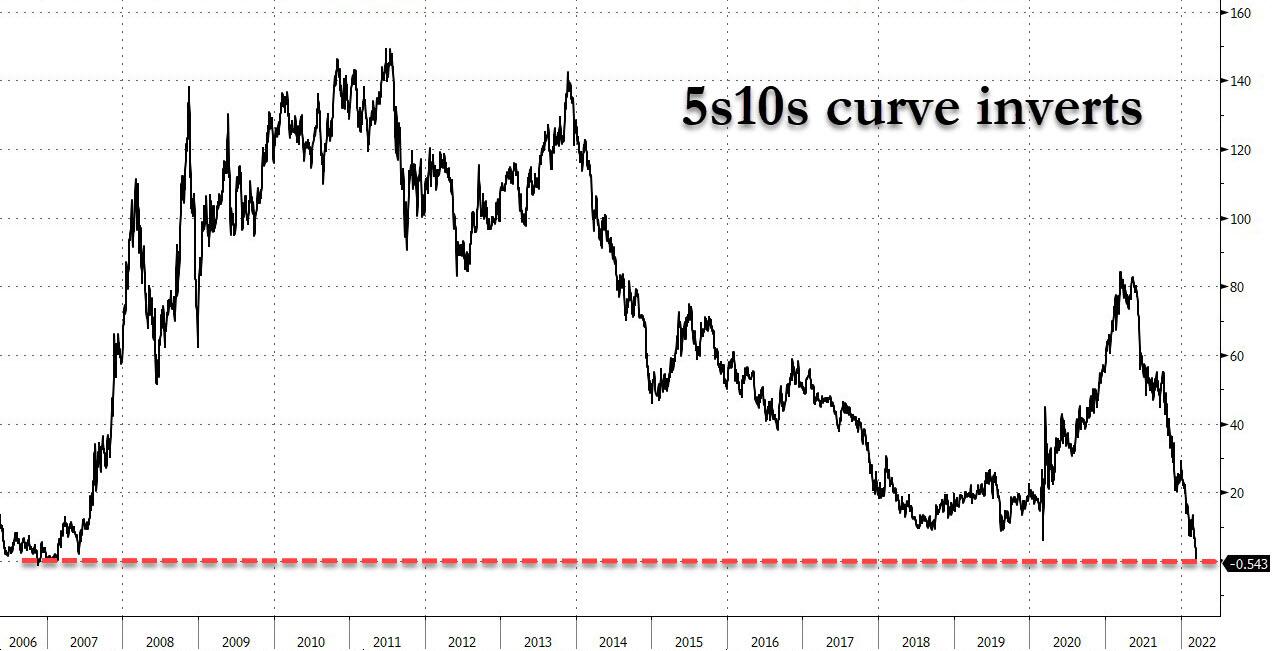

ZeroHedge reports, “After yesterday’s explosive session, which saw stocks trade in violent kneejerk response to conflicting headlines out of Ukraine at first, only to post the biggest ever post FOMC reversal, as markets realized that the Fed’s overly hawkish ambitions are too great and doom the rapidly slowing economy to an accelerated recession, overnight trading has been positively subdued with emini S&P futs trading in a tight 20 point range between 4,340 and 4,360 until 6 am ET, when European stocks turned negative and US equity futures suddenly dropped as much as 0.5%, after the Kremlin said reports of major progress in Ukraine talks are “wrong” and Kremlin spokesman Dmitry Peskov dismissed reports that the warring parties are moving toward a settlement, blaming Kyiv for slowing the negotiations, crippling any hope for a quick ceasefire deal and adding to worries about the outlook for economic growth as the Federal Reserve’s campaign against inflation gets underway. Futures were already wavering as the bond market flagged a growing risk that the Fed’s efforts to rein in prices could trigger an economic downturn with the 5s10s curve inverting. Ominously, Brent jumped more than $5/bbl after tumbling below $100 yesterday.

Contracts on the Nasdaq 100 dipped 0.4% by 7:30 a.m. in New York, while S&P 500 futures were 0.34% lower. The benchmark S&P 500 on Wednesday posted its best two-day rally since April 2020 as the Fed hiked interest rates by a quarter point and Chair Jerome Powell signaled the economy could weather tighter monetary policy. Gold and 10Y yields dropped to session lows, and bitcoin was modestly lower on the session. Europe was slightly green while Asia stocks closed higher, led by the Hang Seng which rose 7%”

VIX futures rose to an overnight high of 27.47 after reaching support at the 50-day Moving Average at 26.32. The Master Cycle appears complete on day 260.00. This is the setup for a slingshot move that may fulfil the required distance for the Head & Shoulders formation.

TNX pulled back from yesterday’s high, but only for a day, as trending strength comes roaring back over the weekend. It may find support at the Cycle Top at 20.33 before resuming its uptrend.

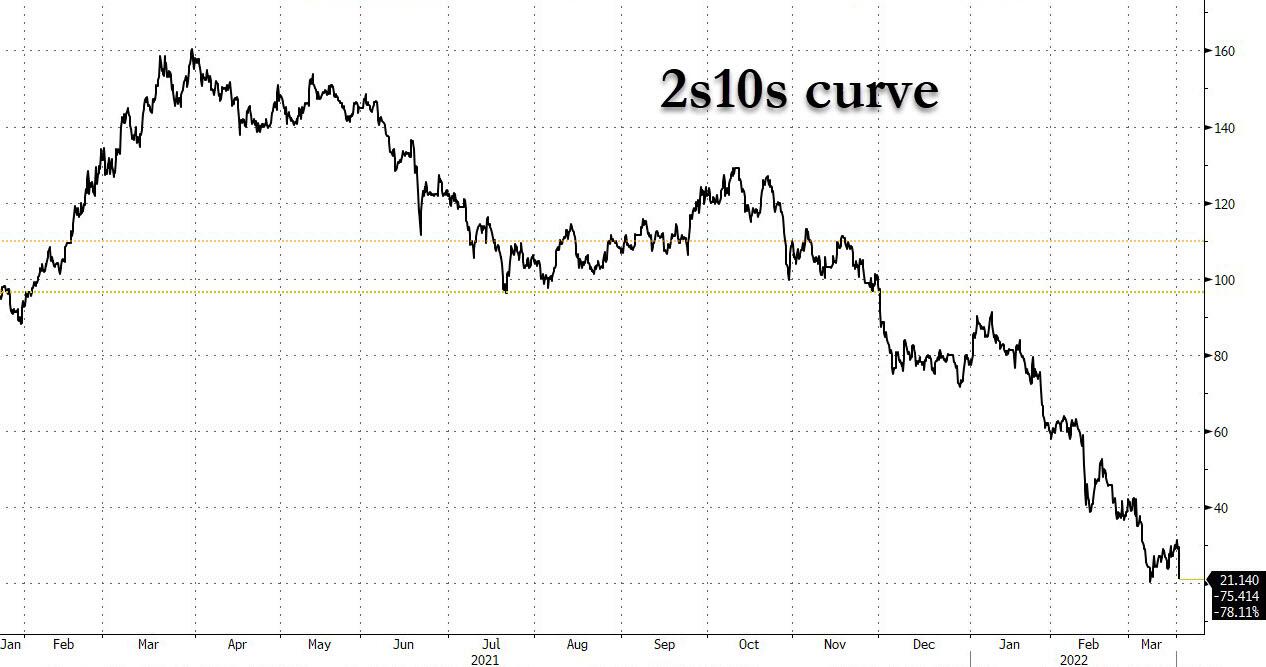

ZeroHedge remarks just how far behind the Fed really is with rates. “Echoing our earlier thoughts that the Fed officially started the countdown to the next recession (and rate cuts) when it inverted the 5s10s moments after Powell starting speaking, DB’s Jim Reid writes that while not every Fed hiking cycle leads to a recession, all hiking cycles that invert the curve have led to recessions within 1 to 3 years. And the problem with the Fed hiking cycle that starts today, he adds with a ZH-esque does of skepticism, is that “there is a decent likelihood that the curve inverts relatively early on. 2s10s peaked at +157.6bps last March and traded as low as +21.9bps last week before settling at around +30bps as we go to print.”

As a reminder, while not as popular as the 2s10s, the 5s10s is also a harbinger of recessions, and usually precedes the 2s10s inversion by weeks. It is this curve that inverted today.

Crude oil is challenging its Cycle Top and trendline at 10.68, but may have a few more days of decline before the Master Cycle is complete. Today is day 254, so the bottom appears to be anticipated on Monday or Tuesday.