1:25 pm

Index options managed to close near the Max Pain zone at the open. Now stocks and ETFs (retail) options expire at the close with 435.00 at the Max Pain zone. Puts dominate at 434.00 and below, with short gamma at 430.00. There’s no telling exactly were things can go downhill, so dealers are keeping a tight rein on the process for now. Traders are hoping that month-end pension fund rebalancing ma pull the market out of its sticky wicket. Unfortunately, Monday’s options expiration is even more loaded for bear than today’s.

This may be playing out similarly to the crash of 1987. Will history repeat…or rhyme?

11:15 am

SPX continues to defend 4350.00 against further encroachment from the bears, but market momentum is turning against it. The NYSE Hi-Lo Index is now at -267.00, hardly bullish. Despite the apparent “success” of this defense, the dealers and hedge funds may have simply postponed the inevitable capitulation and may have turned it into a panic.

Note: Stocks rallied into the 17.2-day pivot at 11:30 am, where I had originally proposed a Cycle low. Instead, the pivot tells us to expect up to 4.3 days of decline from here. Crash helmets required beyond this point…

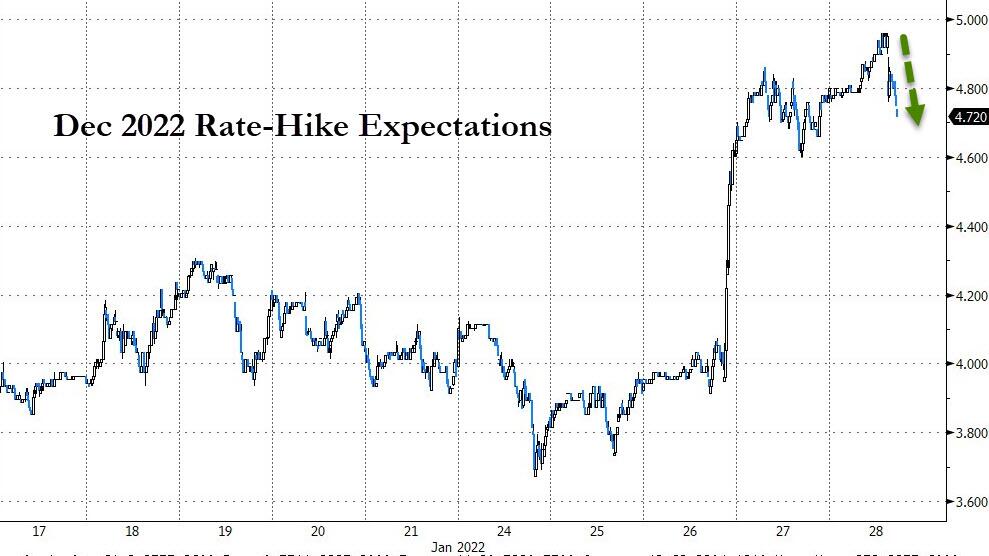

ZeroHedge advises, “Arguably due to rising recession risks, rate-hike expectations are fading modestly this morning…

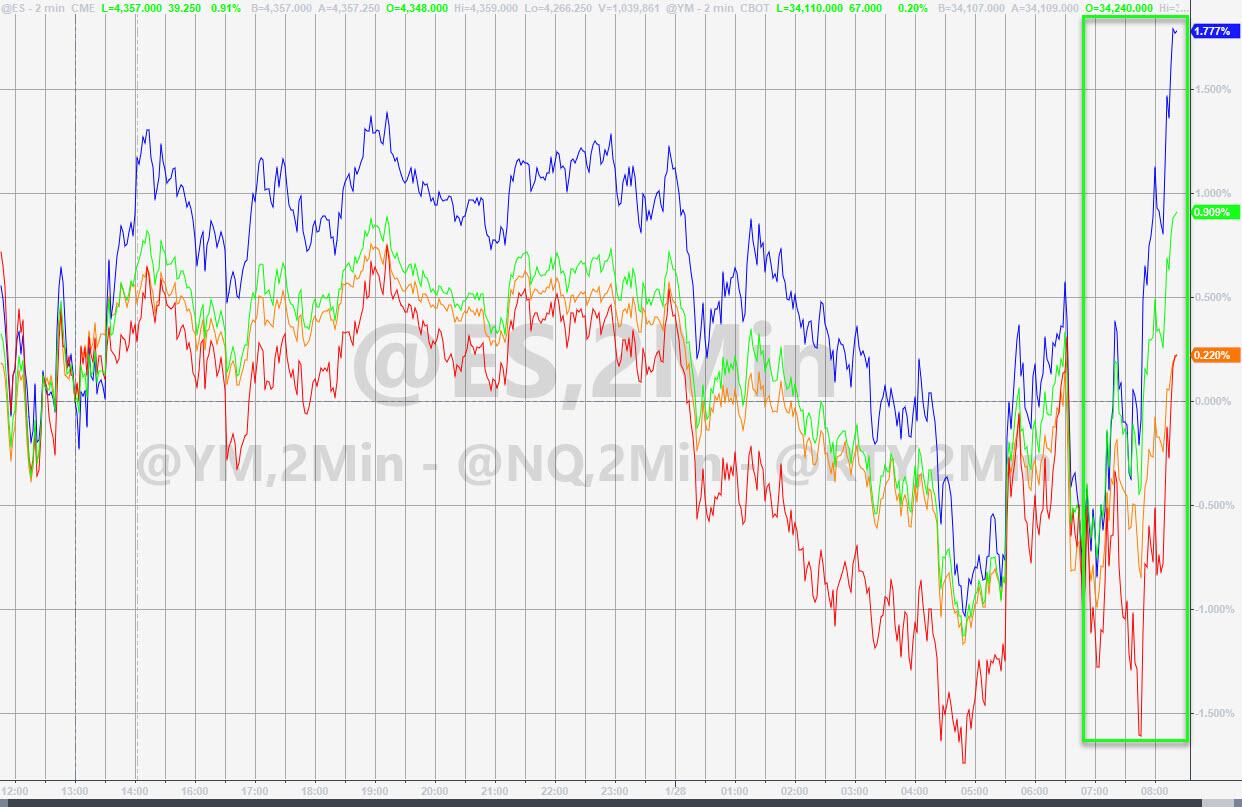

And that – it would appear – is all that anxious dip-buyers needed as they ripped stocks higher from an ugly overnight session. Nasdaq is now up 2% after being down 1%…

The ramp has lifted The Dow back to unchanged on the week…

ZeroHedge remarks, “This is not a Friday brimming with positive developments, to put it mildly. However, at time of writing Asian stocks were following US futures higher on what looks to my jaded eye to be nothing more than a good key earnings report. Here’s a Friday thought: perhaps we should dump all our chattering economic data and burbling/shilling financial reporting and just have the earnings and share price of one firm as a proxy for everything everywhere, the apotheosis of the agglomeration that globalized financial capitalism drives: but why am I even saying “perhaps” when one reads all the rest of the news that apparently doesn’t matter?”

8:15 am

Good Morning!

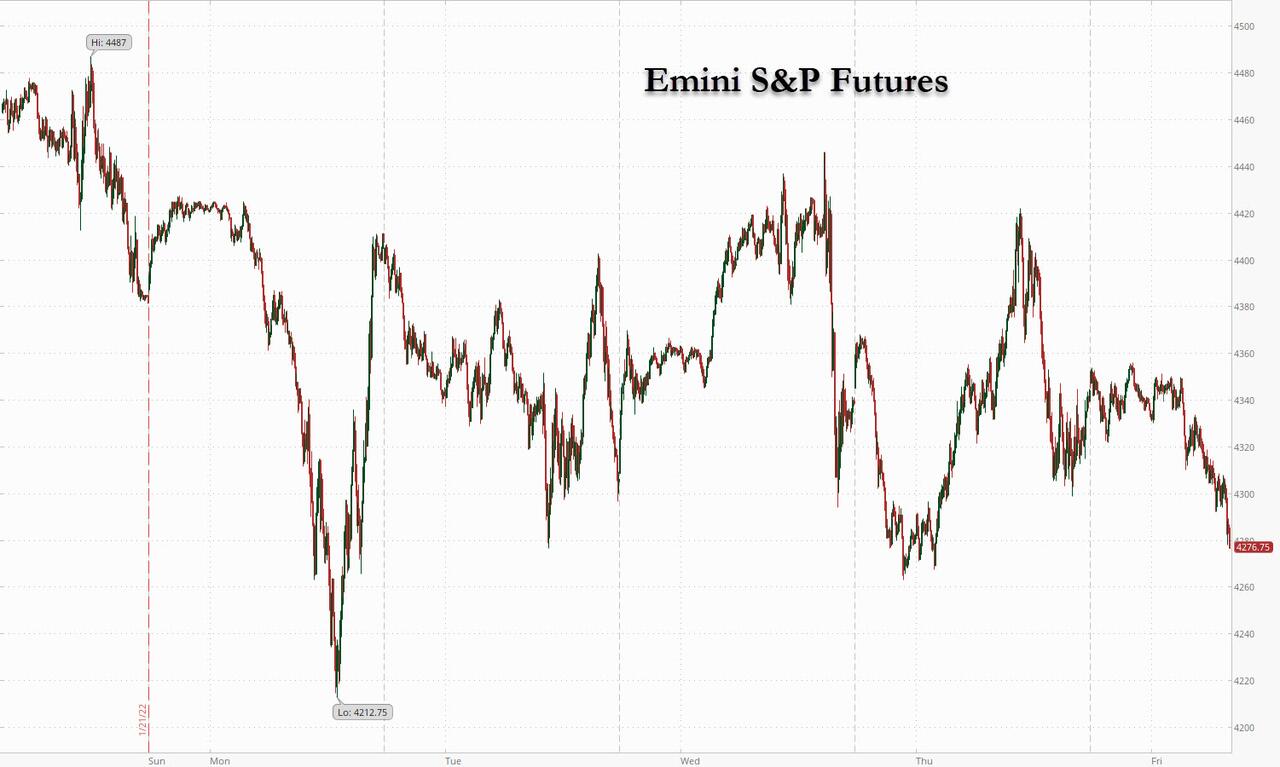

SPX futures have declined to 4274.90 thus far in the final series of declines, the first potentially to the Cycle Bottom at 4096.21, then the last potentially to 4000.00 as the final capitulation occurs. We will attempt to monitor the progress of he decline during the day as the bottom may come as early as 11:am, depending on how well the dealers can defend the Max Pain zone at 4385.00. Today’s expiring options are short beneath 4350.00 with short gamma at 4300.00 and below.

The NYSE Hi-Lo Index closed at -393.00 after trading modestly positive at 6.00.

ZeroHedge reports, ” If you thought that yesterday’s blowout, record earnings from Apple would be enough to put in at least a brief bottom to stocks and stop the ongoing collapse in risk assets, we have some bad news for you: after staging a feeble bounce overnight, S&P futures erased earlier gains as traders ignored the solid results from Apple and instead focused on the risk of higher interest rates hurting economic growth. Contracts in S&P 500 dropped as negative sentiment continued to prevail, while Nasdaq 100 futures erased earlier gains after strong Apple earnings. As of 730am, Emini futures were down 48 points or 1.12% to 4,269, Dow futures were down 335 points or 0.99% and Nasdaq futs were down 77 or 0.6%. The dollar was set for a fifth straight day of gains, the longest streak since November, 19Y TSY yields were up 3bps to 1.83%, gold and bitcoin both dropped.”

VIX futures are climbing, but still inside yesterday’s range with a high of 32.82. In Wednesday’s options expiration, calls dominate at 25.00 and above, with positive gamma at 27.00 and higher. Despite Wall Street’s effort to keep a lid on the VIX, bad news may propel it to 50.00 or 60.00 in a heartbeat. Today and Monday are days of trending strength for the VIX. The only thing I can attribute to this is some outside event that jolts the market.

Bloomberg argues, “Seven straight jumps in the so-called “fear gauge” for the S&P 500 is a signal that it may be time to wager against volatility, if history is any guide.

Only 10 times in the past two decades has the Cboe Volatility Index — better known as the VIX — risen for that many trading sessions in a row. Investors who shorted the gauge after the previous nine streaks of that length would have earned a return of nearly 19% after 20 days, according to data compiled by Bloomberg.”

TNX futures hit a high of 18.54 this morning before settling back above the Cycle Top at 18.04. Trending strength returns next week as it may stage a potential breakout to new heights.

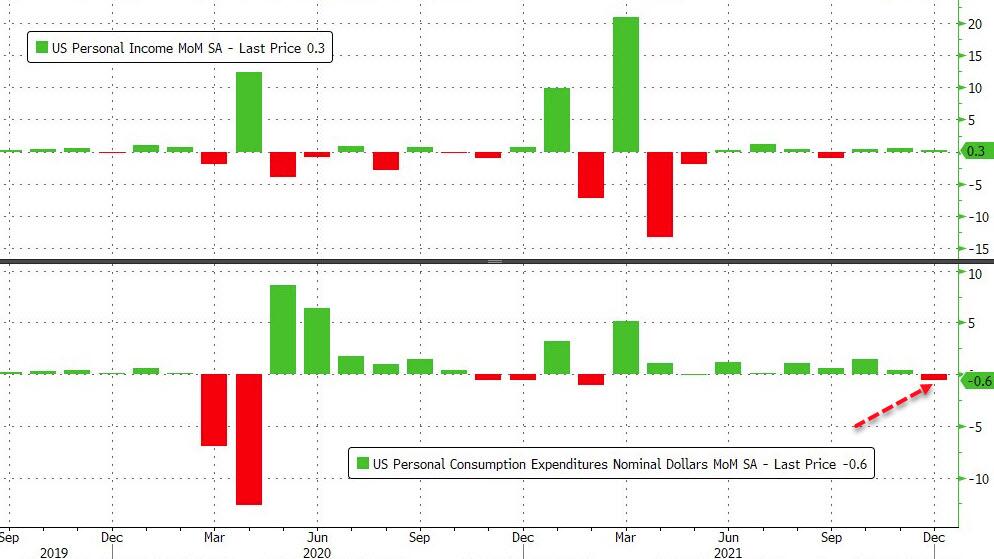

ZeroHedge observes, “Analysts expected a mixed picture from income and spending data in December (with spending expected to drop and incomes rise – an odd pairing during the Christmas month) and they were right with incomes rising 0.3% MoM (slightly less than expected) but spending tumbling 0.6% MoM (meeting expectations). That is the first drop in spending since Feb 2021…

USD futures pulled back today after breaking out above the November high. The Cycles Modle points out next week showing high trending strength, while the next Master Cycle appears to be due in the second week of February. The potential target remains at 98.30.

ZeroHedge reports, “Relatively little talk about the dollar given the latest explosion higher. The mid January shake out has turned into a brutal squeeze, catching many by surprise. DXY is approaching the first big resistance here and RSI is very overbought, but as we all know, overbought can stay overbought for a long time…Second chart shows the last shake out in positioning.”

Source: Refinitiv

West Texas Crude made a possible Master Cycle high yesterday on day 254. The chances are good that the Master Cycle may extend into next week. A new high in crude simultaneously with a new high in the VIX appears intriguing.

OilPrice observes, ”

- Europe’s energy crisis has already cost governments tens of billions of dollars and a looming confrontation with Russia would only make that worse.

- European households are already set to see a 54% increase in the cost of gas and electricity despite the best efforts by governments to keep prices down

- Russia provides about 40% of Europe’s natural gas, and if Russia does invade Ukraine and European governments respond with sanctions, there is a chance that supply could be cut off”

The GSCI Ag Index had its Master Cycle high on Tuesday on day 258. Usually there is a one-to-three week correction before moving higher. All things considered, should it not go beneath the 50-day Moving Average at 400.30, we may see a possibly short and shallow correction before moving considerably higher.

ZeroHedge observes, “This was supposed to be the year that things “got back to normal”, but here we are at the end of January and things have only gotten worse.

As we move forward into February and beyond, there are two key global shortages that we are going to want to keep a very close eye on.

One of them is the rapidly growing fertilizer shortage. A few days ago, the Wall Street Journal ominously warned that “high fertilizer prices are weighing on farmers across the developing world”…”

Gold futures are making new lows as I write. This decline may continue until mid-February, when the next Master Cycle (low) is due. It is on a sell signal as of yesterday.