2:19 pm

SPX is making new lows. Why isn’t VIX making new highs? There may be several reasons. First, the new lows in the SPX appear to be a Wave (b) expansion. This would have a lesser effect on the VIX due to its corrective nature. Second, tomorrow is the expiration for VIX monthly options. VIX is still influenced by the shorts below 23.00. Gamma turns positive at 25.00. And third, VIX may be used by the dealers as a means of influencing the SPX, as in “Tail wags dog.” Should SPX make a new high, the decline in stocks may accelerate.

1:59 pm

SPX made a new low, going deeply into short gamma territory. It may have made an expanded correction and now must dig itself out of the hole. To escape the short gamma, the minimum bounce must be above 4600.00. The 38.2% Fib retracement would be 4638.02. The 50% retracement is 4659.16 and the 61.8% Fib retracement would be 4689.28. Chances are that it may not cross the trendline at 4665.00. This could be a fast bounce, but not fatal to the overall decline. Should the bounce fail, we may see an oversold panic decline.

12:00 noon

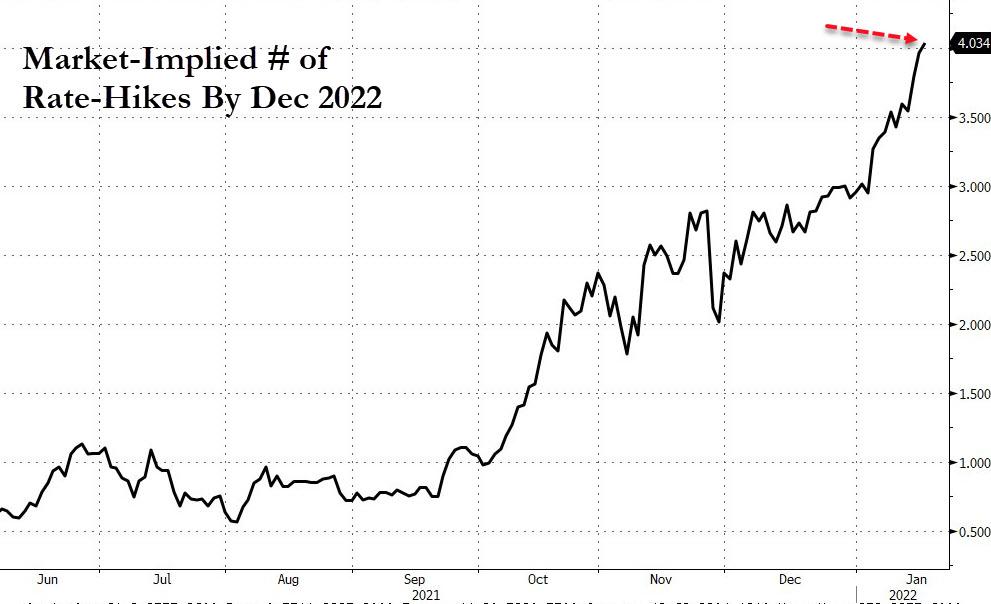

Nomura Warns “Rates Vigilantes” Are At The Gates

ZeroHedge remarks, “Nomura’s Charlie McElligott began his note this morning with an ominous tone, warning that the Rates Vigilantes are at the gates and are now pushing through / above 4 hikes in ’22…

…(and with more “trending” to a 50bps hike out of the gate) – and with a chance now that IF the Eurodollar market were to go ahead and price a hike pushing towards a 50bps “rage liftoff” to start at the March meeting (I’m still paying little-to-no mind to talk of Jan)…

…the Fed will simply “have to” take what the market is dictating to them, despite me currently believing that the FOMC has little desire to do-so.”

(Ed: This is what I have been saying all along.)

11:50 am

BKX has challenged its Cycle Top this morning at 144.25. Beneath that is a confirmed sell signal with the Cycles Model suggesting an almost continuous decline through the end of February. Banks reporting losses and misses in their quarterly earnings confirm that liquidity is being drained from the market.

ZeroHedge reports, “One trading day after JPM reported disappointing earnings and its stock suffered the biggest post-earnings drop in a decade, moments ago Goldman joined it in the penalty box with its shares tumbling as much as 3.1% in premarket trading Tuesday after reporting worse-than-expected fourth-quarter trading revenue, even if overall revenue beat (Q4 revenue $12.6BN, Exp. $12.08BN), with EPS of $10.81 also coming in below expectations of $11.76. Total profit declined 13% to $3.94BN, even as revenues grew 8%. Still, this was a solid number in context: profit at JPMorgan fell 14% in the fourth quarter from a year earlier, while profit at Citigroup fell 26%.”

11:44 am

SPX bounced from its 100-day Moving Average at 4576.00. It appears to be trapped below 4600.00 so the bounce may have ben shortened. Short gamma is prevalent at this level, so be prepared for further weakness.

ZeroHedge remarks, “As Europe closes, US equity markets took a decided leg lower with Small Caps and Nasdaq leading the way but S&P and The Dow not escaping the selling pressure this time…

And this push lower sent the S&P to its 100DMA, The Dow broke below its 100DMA, Nasdaq surged below its 200DMA and Russell 2000 is searching for any support…”

11:05

TNX surged to a new high of 18.56 as ZeroHedge reports, “The New York Fed just issued a statement that is is rescheduling today’s planned Treasury Purchase due to “technical difficulties”:

Due to technical difficulties, today’s Treasury outright purchase operation – scheduled for 10:10 AM in the 4.5 to 7 year sector for up to $6.025 billion – is being rescheduled.

It is now scheduled to take place Wednesday, January 19, 2022 at 10:10 AM. Information on Treasury securities operations can be found on the New York Fed’s webpage.

This does not impact any other operations scheduled for today.”

10:15 am

SPX has completed a 5-Wave impulsive decline. Now for the probable corrective bounce. The 50% retracement value is 4668.00 while the 61.8% Fibonacci retracement is at 4687.00, just above the Wave (iv) high. There is some indication that the bounce may fall short of those two targets. Short gamma is very strong and may become irresistible beneath 4600.00.

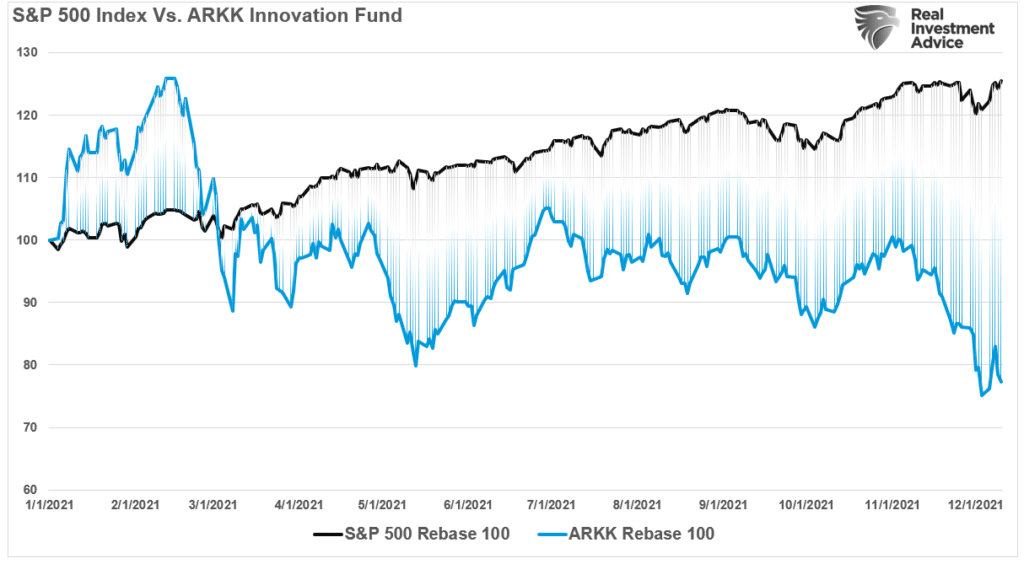

ZeroHedge observes, “The market selloff into January rattled investors as concerns of “So Goes January, So Goes The Year” began to dampen expectations. Combined with a more aggressive stance from the Federal Reserve, rising inflation, and a reduction in liquidity, investor concerns seem to be well-founded.

As discussed last week in “Passive ETFs Are Hiding A Bear Market,” the “blood bath” in the high-beta stocks is particularly humbling for the retail crowd that piled into risk with reckless abandon last year.

“Probably one of the best representations of the disparity between what you see ‘above’ and ‘below’ the surface is the ARKK Innovation Fund (ARKK). While the S&P 500 index was up roughly 27% in 2021, ARKK is down more than 20%. That is quite a performance differential but shows the disparity between the mega-cap companies and everyone else.”

7:40 am

Good Morning!

NDX futures made a morning low at 15284.40 as short gamma has its sway on stocks that could only thrive in a low interest environment. The dominoes are falling while NDX may have another 8 days of decline in a 21.5 day crash. The NDX Hi-Lo Index fell to -600.00 on Friday, setting the tone for this morning’s bloodbath.

SPX futures fell to 4599.20 this morning, testing last Monday’s low and the 100-day Moving Average at 4575.14. Today’s options are positive above 4685.00 and gamma turns long at 4700.00. Today’s cumulative options expiration remains short at 4625.00 and gamma goes short beneath 4600.00 which may stat a chain reaction among the dealers who must match up their books with investors/speculators who are increasingly bearish in options. SPX has 8 days left of a potential 17.2 day decline in the current Master Cycle. On Friday the NYSE Hi-Lo Index fell to -98.00.

ZeroHedge reports, “Yesterday when US stock markets were closed but both bond and equity futures were trading, we pointed out that 10Y Treasury futures implied a yield of over 1.80%, a number which was the highest in years and which we warned would cause headaches for stock traders when the US reopened fully on Tuesday. And sure enough, with 10Y yields surging as high as 1.8536% overnight and 2Y yields jumping to 1.05% (up a whopping 15bps from 0.90% last Friday)…

…. futures are getting hammered this morning, with emini S&P futures down 48 points or over 1% and just above 4,600, while Nasdaq futures were getting hammered again, sliding 1.62% or 254 points. The dollar rose and Brent oil touched $88/bbl, the highest price since 2014.”

VIX futures rose to a new high at 22.09 and is on a confirmed buy signal above the 50-day Moving Average at 19.95. VIX is on the same Cycle as SPX, but inverse with 8 days left of the current Master Cycle.

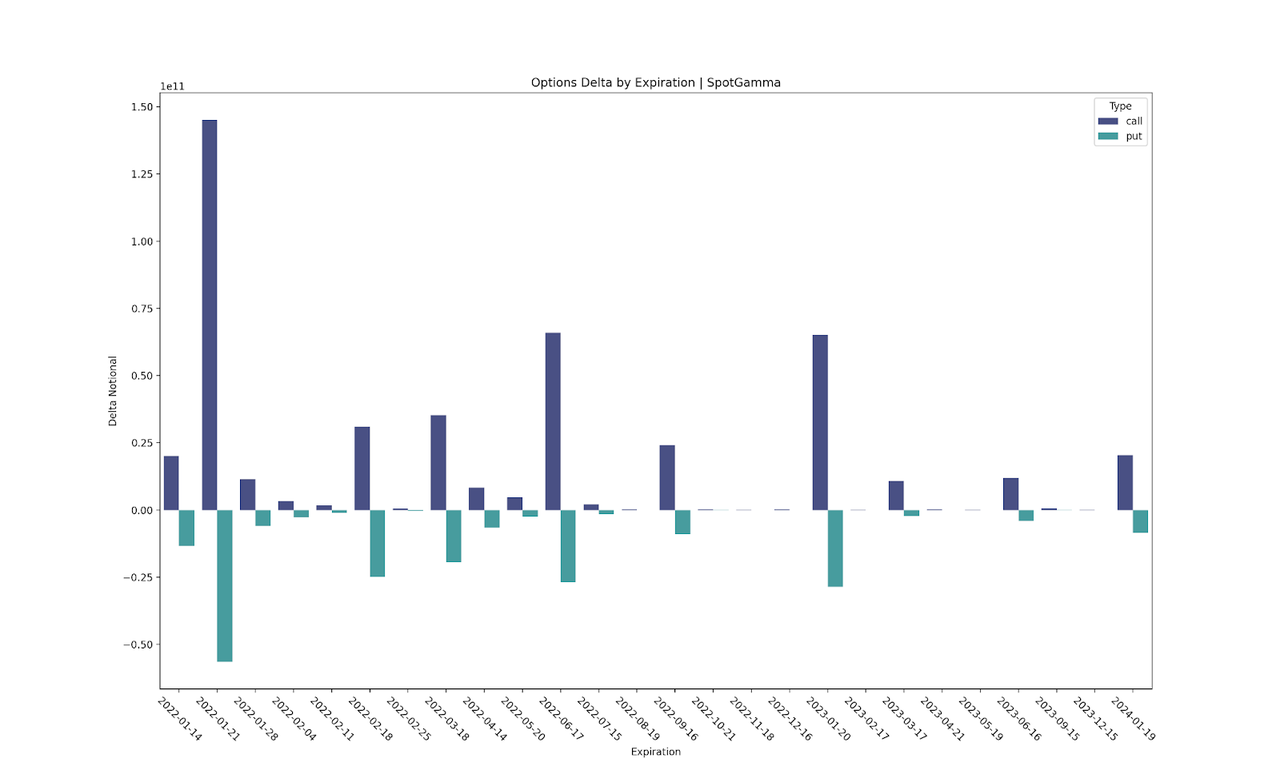

ZeroHedge reports, ”

- The Event: This Friday, January 21st, deep in the money calls worth billions of dollars are set to expire. Deep in the money calls are unique, because they are valued as being essentially equivalent to shares of stock (referred to as a Delta 1 position). Most of these calls were purchased in 2021 and have participated in the massive stock rally over the last year (S&P500 +24% since 1/1/21).

- The Participants: We think these calls are held by a wide variety of players, from large hedge funds all way to wealthy individuals. For example, its well known that Nancy Pelosi favors purchasing long-dated call options. By purchasing large, long-dated call positions, investors gain levered exposure to higher stock prices, while limiting downside risk. Meaning, they can pay a premium to buy more upside through long-dated calls then they can get by buying shares of a company’s stock using the same amount of investment capital.

- The Potential Impact: Regardless of these investor’s individual strategies, at SpotGamma, our models indicate that the net options delta set to expire on Friday, January 21st is over $125 billion. Our base case is that the expiration of these deep in the money calls are a catalyst for volatility – that is expanded stock price movement higher or lower. The ability to assign a direction to this volatility is dependent on how one assumes these investors are positioned.

If the bulk of these call positions (which could vary on a ticker by ticker basis) are held long by investors, then our assumption is that there are options dealers who are short these calls. In turn the dealers likely hedge these short call positions through owning shares of the underlying stock, and/or offsetting long call options (aka long delta positions).

Conversely, if these investors are net short calls, then dealers would own long calls and may in turn short the underlying shares as a hedge.”

USD futures are climbing after having made their Master Cycle low on Thursday. USD appears to be on the final surge of its corrective phase that may run to 98.30, the 61.8% retracement of the 2020 decline.

TNX gapped above the prior high as trending strength took hold this weekend. This period of strength may last through the week with the current Maser Cycle set to last through the end of February. Normally the interval between Cycles is 30 to 60 days. This one is anticipated to go 86 days in varying degrees of strength.

ZeroHedge asks, “(Will) rates matter?

The short term gap between NASDAQ and the 10 year is rather wide here (again). If “they” start to care about rates properly, tech could be in for another round of beating…

Source: Refinitiv

GS: front end will shift higher

GS: “We think current market pricing is too low, and expect the front end of the curve to shift higher by the end of next year”.

Source: Goldman

Fed pricing still looks modest…

…when looking longer out. Nordea, who has been spot on the inflation/yields narrative, writes: “…we do see more room for such pricing to surface later this year and next and see higher bond yields also at the longer end of the curve.”