11:21 am

NDX has made its reversal after the bounce fell short of the 61.8% retracement at 16056.00 and the 50-day Moving Average at 16087.68. The opportunity to short the NDX is now. SPX will follow.

10:05 am

BKX may be the answer to the conundrum of the sinking US Dollar. It appears that money is still flowing into the financial system, evidenced by the rise in bank stocks, the first entities to benefit from money flows. Today is day 267 of the the current Master Cycle. It is not remarkably late yet, but is having a negative influence on Treasuries and the USD.

7:30 am

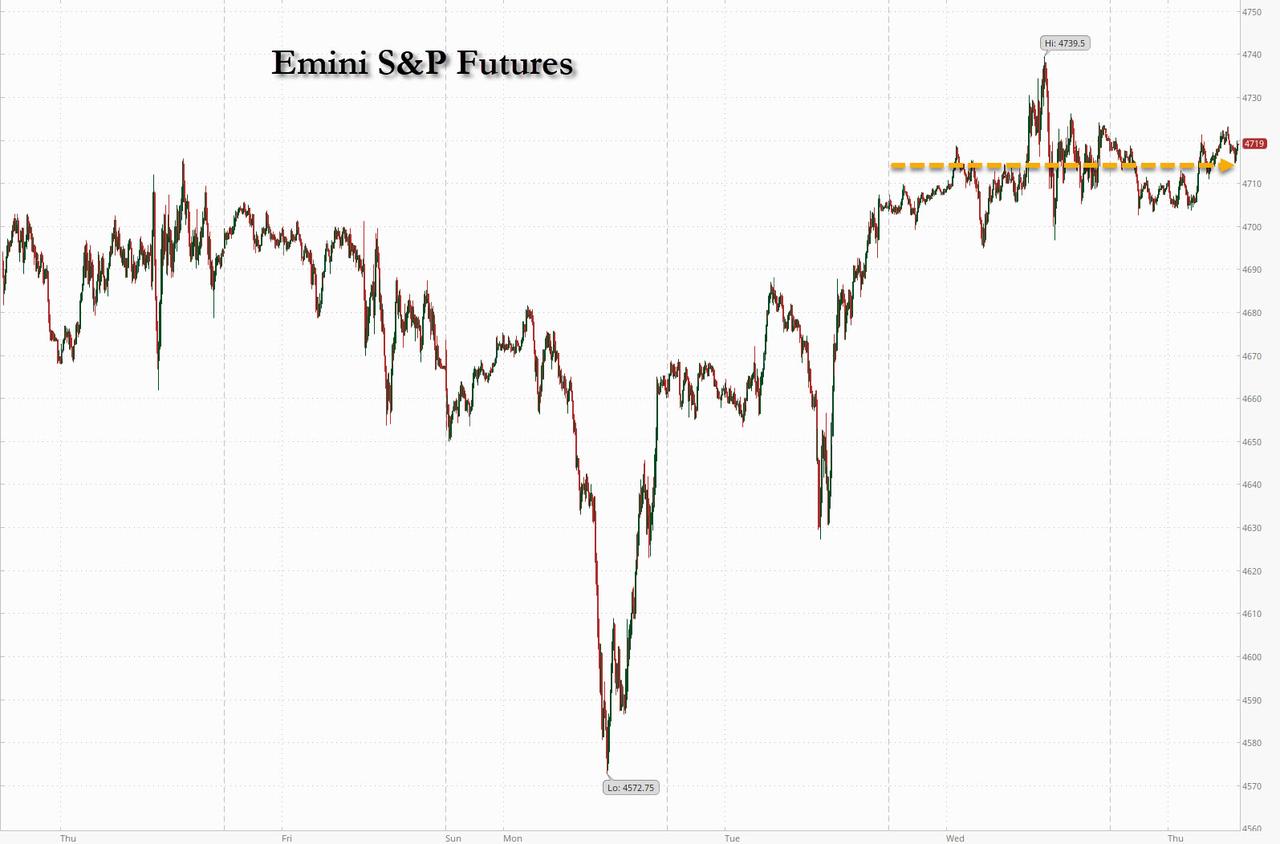

Good Morning!

SPX futures are holding steady near the options Max Pain zone at 4720.00. Options turn negative at 4700.00, while gamma goes negative at 4675.00. It is quite alarming to see how much the options market dominates the SPX. Monday morning’s low was due to Friday’s bearish puts being settled, but SPX quickly recovered to minimize the options pain (to the dealers) by the close of the day. Max Pain is the point where options speculators in both puts and calls get paid the least. Dealers may still be licking their wounds to the wallet that the last decline produced. The NYSE Hi-Lo closed at 64.00 yesterday.

The Cycles Model suggests a turn lower into the last week of January. The probable decline may target the Cycle Bottom at 4063.47, or possibly lower. Point 6 may be reserved for the end of February.

ZeroHedge reports, “US futures were little changed on Thursday one day after the highest CPI print since 1982 and just minutes before another red hot PPI print is expected (9.8%, up from 9.6%), as investors tried to gauge the timing and pace of monetary tightening. S&P 500, Dow and Nasdaq 100 futures were up 0.1% as investors waited for the next trading signal. 10Y yields were flat around 1.74%, and the dollar edged lower as a growing tide of investors bet the world’s reserve currency has reached a peak with rate hikes largely priced-in to the market with Fed tightening likely to lead to an economic slowdown.”

VIX futures rose this morning after an overnight low of 17.85. Yesterday it made an 81.7% retracement, far more than the normal 67% retracement to the mid-Cycle support at 18.62. It may be that the bounce has excited speculators betting on a further decline in the VIX since at the 18.00 strike there are 214,715 put contracts against 9,497 open interest call contracts for next Wednesday’s options expiration. Max Pain for these speculators is 23.00.

NDX futures are rising modestly after the NDX closed positive gamma yesterday. Tomorrow’s option expirations are positive above 15770.00. A decline beneath the trendline at 15600.00 (Max Pain) would reinvigorate the bears. It is interesting how trendlines and Moving Averages influence the investing crowd. I think it is unintentional.

TNX paused near its likely Trading Cycle low made yesterday, due to pre-auction short covering. The Cycles Model indicates that trending strength may come back with a vengeance over the next week.

ZeroHedge remarks, “Ahead of today’s 10Y auction, some rates pundits speculated that the auction would be another blockbuster affair like yesterday’s 3Y if for no other reason than the special, -0.1% rate 10Y notes earned in the repo market suggesting the short overhang is once again extensive and there would be a short covering during the actual auction.

And while that may have been the case before today’s session, the sharp drop in yields across the curve as inflation fears faded after today’s CPI print, meant that it would be virtually impossible to get a non-tailing auction and sure enough, moments ago the Treasury completed the sale of $36BN in the 9-year 10-month reopening of cusip CDJ7, which priced at 1.723%, tailing the When Issued 1.720% by 0.3bps, making this the third consecutive tailing 10Y auction following the end of 6 consecutive stop throughs. The yield was just over 20bps higher than the 1.518% from December 2021 and also the highest since Jan 2020.”

USD futures are lingering near their overnight low at 94.65. Granted, the USD may pull back as far at the mid-Cycle support at 93.19. However, it has stretched the Master Cycle to 288 days, a month beyond the mean. It could mean that investors have been frightened by the high CPI and PPI. Or it could be a major institution is acting to keep confidence up. We’ll know more soon.

ZeroHedge remarks, “Sometimes, financial-market discourse may sound as if Formula One commentators had suddenly switched over to a marathon, where getting overexcited about the first lap may say nothing about what the eventual result might be.

In the first few days of the year, as Treasuries slumped, analysts were wondering whether to tear up their calls for their year-end 10-year yield forecasts. Now, it’s the turn of the dollar — hard as it may to believe, we are just into the second working week of the new year.

In truth, fundamental judgments on none of the assets are passed every single day. Sometimes, there is a lot of noise, but no real signal, and it happens especially around the start of the year as flows move across seamless financial borders with greater velocity. Indeed, it does feel that way: real-rate differentials have hardly moved one way or the other since the start of the year, meaning capital flows may be the reason why we are seeing what we are.”