8:05 am

Good Morning!

NDX futures hit an overnight high of 15908.80, just above the Fibonacci 50% retracement level at 15886.35. While I had thought that the 22-month trendline might be the stopper for this rally, and the retracement appeared complete, the powers-that-be had their own plans to raise the NDX to the Max Pain zone at 15850.00. However, today’s options gamma turns positive at 15875.00 and especially so at 15900.00. The Cycles are primed for a turn this morning. That would give the NDX 8.6 days of decline and less than two days of a bounce. The Cycles Model calls for a probable decline through the week of January 24, a possible 10.45 to 12.9 days of further decline.

The NDX Hi-Lo closed at -127.00 yesterday, still negative despite the impressive rally.

ZeroHedge observes, “Prices should continue to be unstable.

That’s the message from many in the market as while talking-heads want to proclaim yesterday as a fundamentally-driven buying spree confirming how ‘cheap’ hyper-growth has become, SpotGamma points out that is was actually a “short cover rally” fueled by delta (puts closed/rolled) and vanna (implied volatility crush).

Additionally, SpotGamma’s models continue to suggest high volatility until the 4700 strike is recovered – and it is not until 4800 that we would see significant dealer based support.”

SPX futures rose to an overnight high of 4739.00, just beyond the 61.8% retracement value at 4728.42. Today’s options expiration Max Pain zone is near 4700.00. While positive above that, gamma remains neutral to 4800.00. Another Cyclical pivot may be reached this morning that may turn equities back down. The NYSE Hi-Lo Index closed at 39.00 yesterday, above the 50-day Moving Average at 12.40.

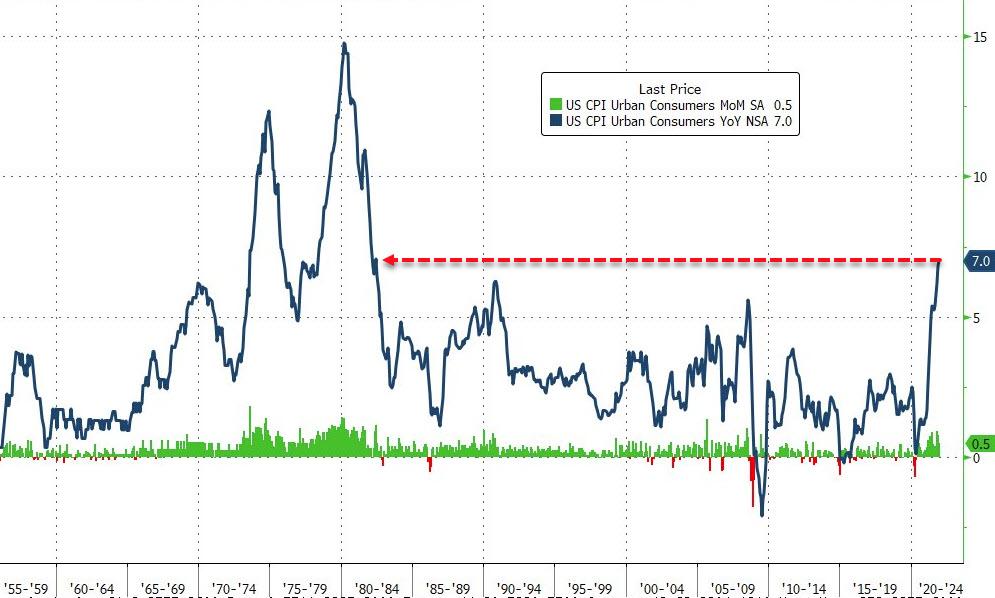

ZeroHedge reports, “U.S. index futures were little changed, if slightly in the green on Wednesday as investors settled into a wait-and-see mode ahead of today’s “brutal” CPI report which is expected to show the highest CPI print in nearly 40 years, a time when the fed funds rate was 11% compared to 0% now…

… and gauge the pace of Federal Reserve tightening. Consensus expects December CPI to show inflation climbing to 7.0%, a result which could see front- end fully price in a March rate hike (currently priced at 85%). Helping the overnight mood in Asia, was a moderation in China’s inflation pressures, with CPI dipping to 10.3% y/y in December, giving the central bank scope to cut interest rates to cushion the economy’s downturn just as most major nations look to tighten policy. At 730am ET, S&P futures were up 0.2% of 7.50, and Nasdaq futures rose 22 points or 0.14%, recovering toward Asia’s best levels; Dow futures were up about 0.1%. The dollar was slightly lower, extending on its recent sharp drop, while Treasury yields were steady.”

VIX futures rose to 18.69 in the overnight session, still beneath the 50-day Moving Average at 19.75. VIX has made a 73% retracement and may be poised for a lift-off.

TickerTape observes, “Markets crash. And when they do, it can be fast. So, it’s a good idea to study the Cboe Volatility Index—or more affectionately, the VIX—to help you guess when that next market sell-off might happen.

Often, the VIX is inversely correlated with the S&P 500 Index (SPX). When the SPX goes up, the VIX typically goes down. But there’s more to the VIX than this relationship. In addition to it being the market’s “fear gauge”—investors tend to be more fearful when market volatility (vol) is high, and less so when vol is low—the VIX measures the market’s expectation of future volatility implied by SPX options prices.”

TNX has pulled back beneath the Cycle Top and may test the Lip of the Cup with Handle at 16.93 this morning. However, it may be running out of time, as the CPI has already been announced. Be prepared for a blast-of ot Trending strength that may last up to two weeks.

ZeroHedge reports, “Consensus was convinced – with barely any outliers – that this morning’s consumer price index would print with an astonishing 7.0% YoY (and notably 7 of the last 9 releases have come in above consensus) and they nailed it with the 7% print at its highest since June 1982 (when ET was launched in the US)…

Source: Bloomberg

That is the 19th straight monthly rise in headline CPI and Core CPI also surged to its highest since Feb 1991 (printing hotter than expected at +5.5% YoY)…”

ZeroHedge observes, “What do you get when you tae half a portion of excess GDP growth this year over trend expansion, together with half a portion of excess inflation over its long-term trend and combine them with the neutral rate of the economy?

You get a Fed funds rate of 4.15%, that’s what. At least, that’s according to the recipe that John Taylor at Stanford University came up with before the turn of the century. Taylor himself agrees. The Fed is “way behind” the curve, and depending on the assumptions made, the federal funds rate should be anywhere from 3% to 6%, not the near-0% now targeted by the central bank, he remarked at this year’s annual meeting of the American Economic Association.”

USD futures made an new overnight low of 95.23 but may be poised for a bounce higher. Trending strength comes back early next week and may last through the first week of February.