11:05 am

Theepochtimes comments on food prices, “Food prices across the world have risen to their highest levels in a decade on the back of tightening supply conditions coupled with robust demand, according to the Food and Agriculture Organization of the United Nations (FAO).

The FAO’s food price index, which measures world food commodity prices, has surged by 32.8 percent in the 12 months through September, coming in at a reading of 130 points, a level not seen since 2011. On a month-over-month basis, the index rose 1.2 percent.

Accounting for the bulk of the rise in the index were higher prices of most cereals and vegetable oils.”

10:50 am

SPX made a 61.4% retracement of Friday’s decline and appears to be stalled. Normally a Fib rally may be attributed to short covering and not much else. There seems to be little incentive to go higher. VIX also tested its low at 18.20 , but did not go beneath it.

ZeroHedge remarks, “Something’s different this time.

For the first time since the collapse in March 2020, the S&P 500 has failed to rebound back to new highs after testing its key uptrend technical levels…

Source: Bloomberg

So what happened?

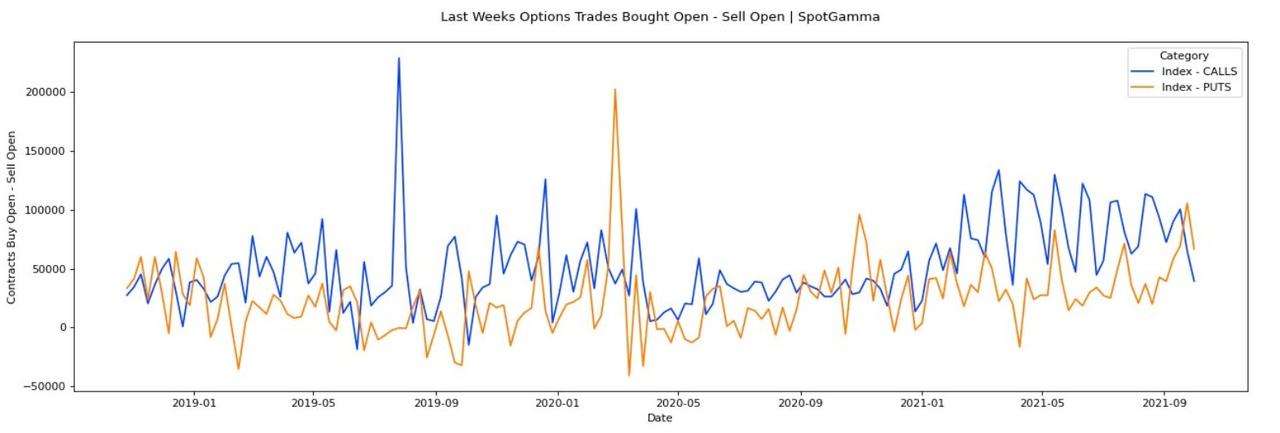

SpotGamma notes that the OCC data we collect offers some insights into what happened last week. According to this data, Index call options were sold to open in pretty strong size (top chart, blue line). Along with that there was some light put options shorted (orange line), but much less aggressively that in months past.

Source: SpotGamma

For months the default reaction to any selloff in markets was to short volatility (with the recovery time of any dip in the market measured in hours).

Off of the debt ceiling punt last week there was a snap-back rally in which very short dated options (1-3 days to expiration) were sold but nothing “real” (ie larger, longer dated) moved.

It seems like traders used Thursdays rally to reposition long volatility/short markets.

The bigger takeaway is this: that reflexive short volatility trade has apparently left the building. We’ve viewed this reflexive vol shorting as a primary driver of markets in the short term. With this mechanism absent, the market seems unable to recover.”

8:20 am

Good Morning!

SPX futures slid beneath Sort-term support at 4381.18 this morning as the weekly options settled in the Max Pain zone. A quick scan of the options expirations show that Max Pain lies at 4350.00 today, while it moves to 4375.00 on Wednesday and Friday’s monthly expiration. That information may lead us to believe that the roller coaster in porices may continue this week. However, the Cup with Handle formation may prove to be a “trap door” should prices fally beneath the Lip at 4306.00.

ZeroHedge reports, “While cash bonds may be closed today for Columbus Day, which may or may not be a holiday – it’s difficult to know anymore with SJW snowflakes opinions changing by the day – US equity futures are open and they are sliding as soaring oil prices add to worries over growing stagflation (Goldman and Morgan Stanley both slashed their GDP estimates over the weekend even as they both see rising inflation), fueling concern that a spreading energy crisis could hamper economic recovery (as a reminder, yesterday we had one, two, three posts on stagflation, showing just how freaked out Wall Street suddenly is).

Rising raw material costs, labor shortages and other supply chain bottlenecks have raised concerns of elevated prices hammering corporate profits while rising rates are suggesting that a tidal wave of inflation is coming. And while cash bonds may be closed, one can easily extrapolate where they would be trading based on TSY futures which are currently trading at a 1.65% equivalent.”

TNX futures are open this morning, but may close at the open of the cash market. Today is day 257 in the Master Cycle, giving us another day or so of trading before the final high may be in.

VIX futures rose to a weekend high of 20.45, above the Ending Diagonal trendline again after Friday’s brief test of the 50-day Moving Average. Wave [c] of 3 is projected to be at least double the size of Wave [c] of Wave 1. The last “buy the dip” opportunity for the VIX may have assed on Friday.

On Friday ZeroHedge commented, “Time to revisit Friday VIX hedges?

The theme of VIX being the relativity more exuberant one continues. Note the gap between the VIX inverted vs Spoos widening further. VIX didn’t “buy” the late day fade yesterday, and is continuing down as the weekend effect kicks in.

VIX isn’t dirt cheap (yet), but given the various cross asset vols all showing huge moves over the past few weeks, we doubt VIX will drift much lower. Our take from yesterday is playing out according to plan:

“So far trusting VIX has been the accurate “bounce” take, but let’s see if they manage puking VIX even more into Friday.”

USD futures continue to consolidate near the Cycle Top resistance at 94.13. The Current Master Cycle projects a potential low by mid-November.

West Texas Light Crude futures hit a weekend high of 82.17 before easing back. I had originally put the Master Cycle high on Wednesday (day 266), but we may be seeing an extended high this morning (day 271). If so, a corrective phase may begin, lasting through mid-November. The Broadening wedge formation may be triggered in this decline.

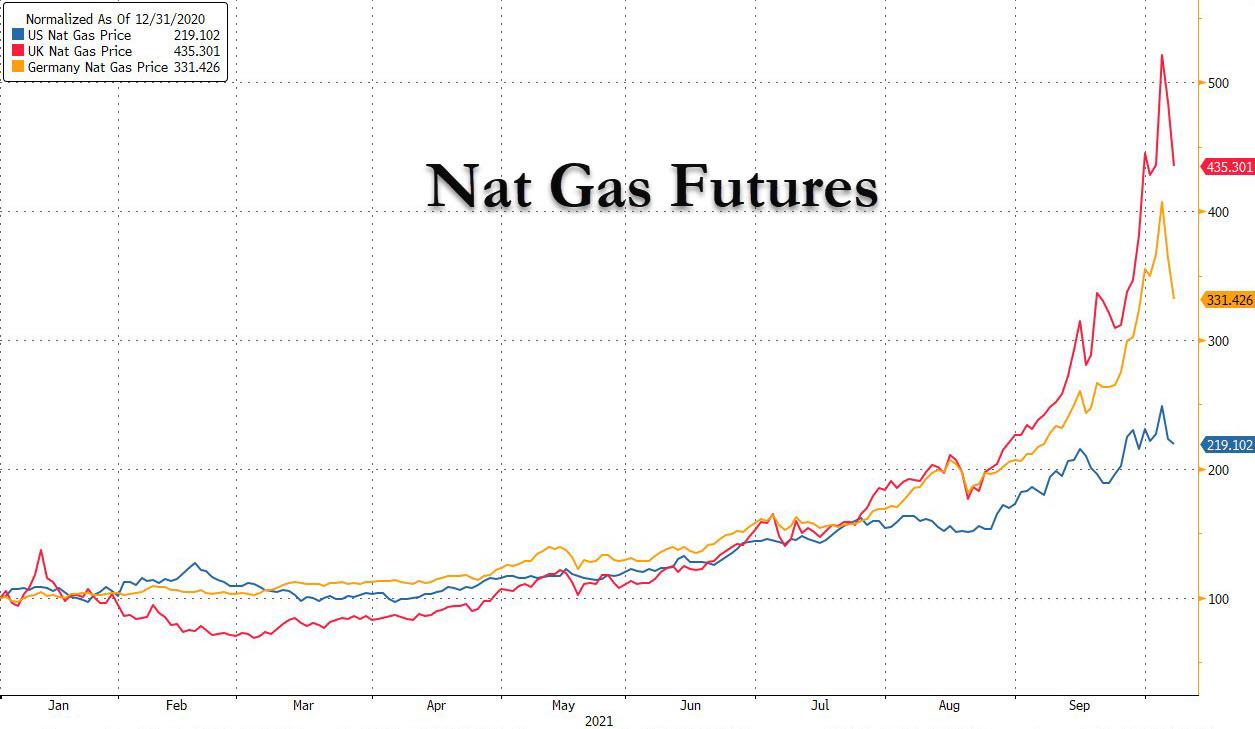

ZeroHedge observes, “The surge in natural gas prices in 2021 has put even crytpocurrencies to shame: US Henry Hub spot prices have been averaging around $6/mmbtu, up about 40% from early in August and a surge of around 200% relative to prices at the start of the year; prices in German and the UK are orders of magnitude higher.

The dramatic price increase has prompted questions how it will impact inflation prints in the near-term, both headline and core, and indeed as JPM economist Daniel Silver writes today, “this recent jump is notable and should boost consumer prices.”

ZeroHedge also worries, “Commodity prices are surging around the globe, so it should come as no surprise: Marine fuel is getting a lot more expensive. That’s bad news for ship operators on the cost side, and, in the container business, yet another headache for cargo shippers.

Marine bunker prices are “soaring,” said Alphatanker on Thursday. “This has not just impacted 3.5% [high-sulfur fuel oil or HSFO] but also 0.5% VLSFO [very low sulfur fuel oil].”

“There are expectations that crude, and therefore marine fuel, could move higher in the coming weeks as oil markets tighten further,” warned Alphatanker, adding, “This will undoubtedly clip gains in tanker earnings.”

All ship categories, not just tankers, are taking a cost hit. On Thursday, the S&P Global Platts T4 index estimated that a Capesize (a dry bulk ship with capacity of around 180,000 deadweight tons) burning VLSFO was spending $24,596 per day on fuel.”

The GSCI Ag Index continues to consolidate above all supports as it relieves its overbought condition. Thee is a possible Trading (minor) Cycle lw due at the end of the week, but the longer view is for the rally to continue through mid-December. The following articles give us pause to consider just how far food prices may rise.

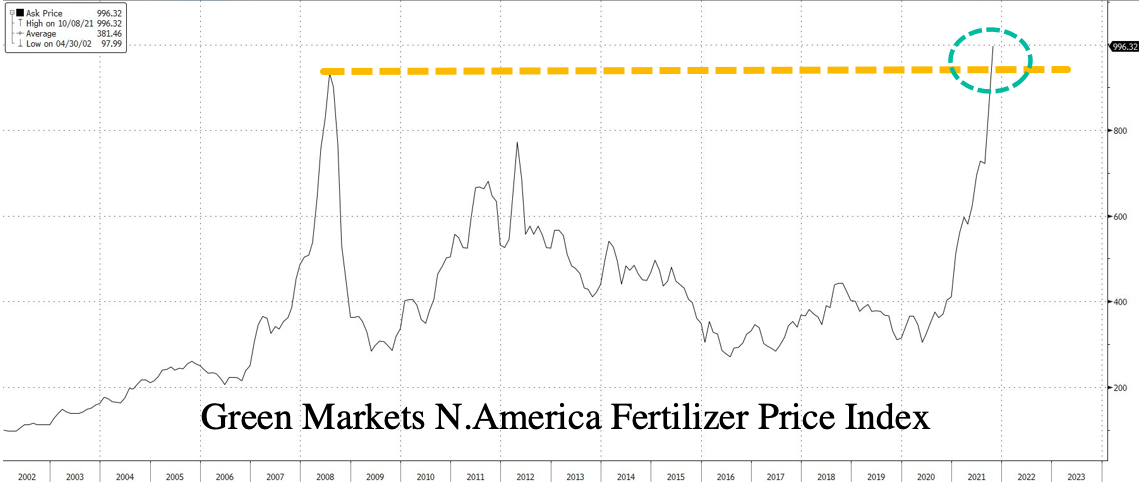

ZeroHedge notes, “Fertilizer prices have risen to a record high in North America, threatening to boost food inflation even higher. Nitrogen products are increasing due to the cost of natural gas, which is used in the manufacturing process.

The Green Markets North America Fertilizer Price Index soared to a record high last week of $996.32 per short ton.

The fertilizer market has been roiled by hurricanes, plant shutdowns, sanctions, and shortages of natural gas in Europe and China, pushing nutrient prices sky-high, which will raise the cost of production for global farmers. Here are global fertilizer prices zooming higher: ”

ZeroHedge also notes, “Americans are accustomed to a bowl of cereal as their go-to breakfast meal is about to experience a price increase because of rapid food inflation.

This year, a devastating drought in North American oat fields has resulted in the lowest harvest for the cereal grain in years, pushing prices to record highs, a warning sign that breakfast inflation is imminent.

Scorching heat waves in Candian oat fields slashed production to an 11-year low. Canada, the world’s biggest exporter, ships most of its oats to the US, its largest consumer.

The result so far has been a new record high in oats futures trading on the CME. The sudden spike in prices has yet to ripple through supply chains to affect consumers, though that will be coming.

According to Bloomberg, “the situation for North American farmers was so dire in the summer that many cut their losses and harvested damaged plants to be sold as feed for animals.”

What this means for consumers is that dwindling supplies and record-high prices will soon affect foods like cereals, oatmeal, and granola bars, all popular breakfast items.”