3:20 pm

As a further evidence of a bearish structure, the NYSE Hi-Lo Index opened negative and remains so going into the close. The adjusted reading (sans the ETFs), which will not be available until morning, may be considerably more negative.

2:55 pm

Imagine my surprise when a Triangle formation appeared on the chart of the SPX. This is a continuation formation that may be even more bearish than most could imagine. A Triangle occurring at the bottom of market day 21.5 has interesting implications. First of all, it suggests that Wave (C) may be extremely impulsive and dangerous…until it reaches its target. Second, it does not negate the Cup with Handle formation which allows multiple crossings of the Lip. By the way, the Cup with Handle may not be the final destination. Finally, it still does not tell us which multiple of days it will take to reach bottom. A “best guess” suggests 12.9 days from today, taking us to October 25…

…which potentially agrees with the proposed VIX Master Cycle high which has been a puzzle to me until now. Stand by for a possible final probe to or above the upper trendline before the reversal.

10:02 am

SPX lost Cycle Bottom support at 4307.18 and support at the Lip of the Cupw with Handle formation at 4306.00 suggesting that institutional money and possibly hedge funds are exiting the market. Monday’s low at 4278.94 is threatened and gamma is growing more negative.

ZeroHedge observes, “The last few days have seen US equity market trading within a broad range, characterized by violent lurches from one side of the range to the other.

SpotGamma attributed this “ping pong” due to the unchanging options landscape. Despite the volatility there are little material changes to options positions, and so dealers (they’re short gamma) are simply adjusting their hedge.

They likely need to buy futures up to the 4365 zero gamma line (zero gamma implies “no more gamma hedge needed”) and selling down to the large put area <4300.

SpotGamma notes that overnight data indicates that rather slowly the options positions are beginning to fill in at prices overhead. The Volatility Trigger (aka gamma flip line) has dripped lower to 4345 (from 4370) and we note a lot of gamma now at the 4350 position. In other words: our upper bound is now 15 handles lower today than yesterday. The air pocket above 4300 is constricting.”

8:10 am

Good Morning!

SPX futures made an overnight low of 4284.10 before easing back to 4300.00. Yesterday’s observation of the 8.6-hour rally apears to have been accurate. Today’s options expiration still dominates trading. There is open interest in 19,383 net call contracts at 4350.00, which were threatened but not achieved at the close. SPX peaked just under the 50% retracement level at 4371.34 and are considerably lower, hovering near 4300.00, where the options gamma is negative. SPX’s final spike of strength is now over and the race may be downhill from here.

ZeroHedge reports, “n our market comments on Tuesday we were stunned by the resilient surge in tech names and the broader market, even as yields soared on the biggest jump in breakevens since the presidential election, noting that something is very broken with this picture. Well, one day later normalcy is back: US stock index futures tumbled as much as 1.3% on Wednesday before paring some losses, after soaring oil and gas prices (rising as much as 40% in Europe today alone) fed into fears of higher inflation and fueled concerns of sooner-than-expected tapering, which in turn pushed 10Y yields just shy of 1.57%. At 730 a.m. ET, Dow e-minis were down 309 points, or 0.9%, S&P 500 e-minis were down 49 points, or 1.12%, and Nasdaq 100 e-minis were down 181 points, or 1.23%, to the lowest level since June 25 on a closing basis, signaling more downside for tech shares after Tuesday’s short reprieve

Up to Tuesday’s close, the S&P 500 index logged its fourth straight day of 1% moves in either direction. According to Reuters, the last time the index saw that much volatility was in November 2020, when it rose or fell 1% or more for seven straight sessions.”

VIX futures surged to 24.10 in the early morning hours before settling back somewhat. The Cycles Model suggests a surge of strength today as it may break out of its consolidation range.

TNX futures appear to have broken above the previous high at 15.67, but it opened in the cash market a bit more subdued. The Cycles Model suggests today may be a day of strength (a breakout?) with more to come in the following week. A Master Cycle high is due during options week. It is possible that the Cycle Top resistance at 17.94 may be reached by then.

ZeroHedge remarks, “US 10 year breaking out?

The US 10 year is above the big 1.55% level. Let’s await to see how this closes today, but a “proper” close above the key resistance means things will get “dynamic” again.

First big level to the upside would be around recent highs at 1.75%.”

Source: Refinitiv

USD futures reached an overnight high of 94.45, challenging the prior high. A breakout here tels us that Wave 3 has a distance to go before completion. The Cycles Model suggests USD may continue higher, and with strength during options week. The Master Cycle doesn’t end until the second week in November.

Crude Oil pulled back from its Cycle Top resistance at 78.19 as it makes a brief consolidation. Trending strength may return at the end of the week, however. The current Master Cycle may continue through early November before reaching its next high.

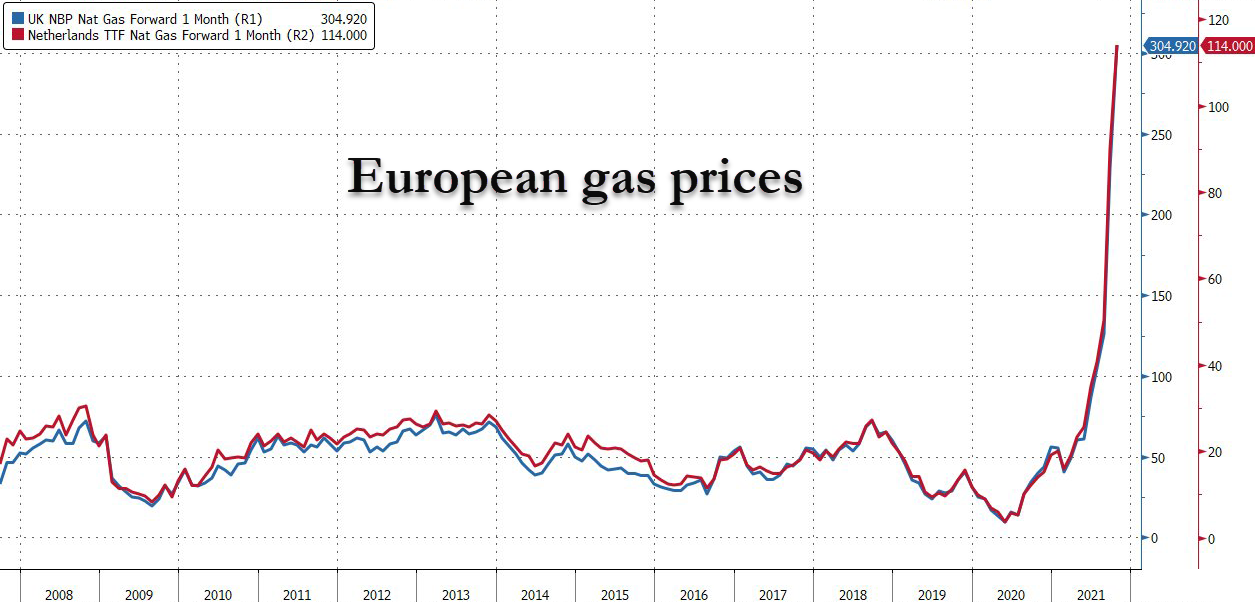

ZeroHedge notes, “Europe’s power crunch is roiling energy markets Wednesday as Dutch and U.K. natural gas futures jumped 60% in just two days, hitting record highs along with soaring power prices.

Front-month Dutch natgas futures rose an astonishing 40% today to a record 162.125 euros per megawatt-hour after a 20% move higher on Tuesday. U.K. natgas futures surged 39% today, hitting 40 dollars.

For context, the EU NatGas prices are equivalent to $250 oil…

The GSCI Ag Index remains above all supports and is on a buy signal. The Cycles Model suggests that it may remain so through mid-December. The price of energy will have a massive effect on agriculture, as we note below.

ZeroHedge observes, “A natural gas shortage across Europe has created supply-chain shocks, as seen in the food industry, where problems continue to worsen. European natgas prices are at insane levels, triggering a domino effect of output reduction or closures of fertilizer plants on the continent.

Last month, two of the U.K.’s largest fertilizer factories producing 45% of domestic demand closed, and one shortly reopened with government aid. By late month, Austrian fertilizer producer Borealis AG slashed ammonia output after the cost natgas compressed margins in an industry facing tight supplies.

As the dominos fall, SKW Piesteritz, Germany’s largest ammonia producer, announced a 20% reduction in ammonia production due to the record-high natgas prices on Tuesday.

“The level that has now been reached no longer enables economically sensible production, so that we are forced to take this step,” the company told Bloomberg in an emailed statement.

“Without government action, there is a risk of production being halted shortly,” the statement continued. “