12;00 PM

For those of your who may not be aware, the La Palma Volcano has intensified its eruptions and opened up yet another vent. The threat of a tsunami intensifies, although the NOAA?National Weather Service has not recognized it as a threat. I have informed family members on the East Coast to seek higher ground. Should a collapse occur, we would only have 6-9 hours warning.

I am leaving town for the weekend. Be back on Monday morning.

8:15 am

Good Morning!

SPX futures are down over .5% already. Welcome to the second half of the decline (in time). The retracement is showing Wave (2) behavior, so I will leave the current labels. This Master Cycle is scheduled to land on October 15, but that day being options expiration, may extend several more days due to the bearish gamma. The list of catalysts has not gone away, although China is rising to the forefront.

9:44 am Note that SPX may yet rise to its Wave B high at 4486.87 as liquidity is still being poured into the markets. Should new lows be made beneath the 50-day Moving Average at 4437.30 in the next hour, that event goes away.

ZeroHedge observes, “US futures and European stocks fell amid ongoing nerves over the Evergrande default, while cryptocurrency-linked stocks tumbled after the Chinese central bank said such transactions are illegal. Sovereign bond yields fluctuated after an earlier selloff fueled by the prospect of tighter monetary policy. At 745am ET, S&P 500 e-minis were down 19.5 points, or 0.43%, Nasdaq 100 e-minis were down 88.75 points, or 0.58% and Dow e-minis were down 112 points, or 0.33%.”

VIX futures rose to a mornig high of 20.37, challenging the trendline and promises more to come.

Nomura notes that the rally carried big volumes, “Yet despite the return of such scattered bullish flows, McElligott notes that there remains much angst in the Vol space (Skew still roofed as downside demand remaining extreme), versus still “pervasive skepticism” towards broad Equities upside index / ETF / sectors / industries (Call Skew still nuked).”

The NYSE Hi-Lo closed beneath its 50-day Moving Average at 77.68, leaving some doubt about the “RECOVERY.” Today’s (and future) action may show the real weakness in the NYSE. Monday’s low was day 256 of the old Master Cycle. The new Master Cycle is due to bottom on October 15.

TNX gapped above bot the 100-day and mid-Cycle resistance at 14.07, putting it on a buy signal and launching a new rally that may reach the Cycle Top in Wave (A) and 20.00 or higher in Wave (C) of [5]. The spike in volatility today may be a delayed reaction to the rising yields as noted yeterday.

The Cycles Model clearly marked the bottom of Wave [4] on September 15 even though I missed it due to a truncation in which Wave 5 was higher than Wave 3. The chart is now corrected.

ZeroHedge notes, “While the US 10 year put in a huge candle yesterday, breaking above big resistance levels, bond vol (MOVE) was steady.

The early year squeeze in yields was accompanied with surging bond vol (which Fed dislikes).

The move in yields is so far just one day, but let’s see how bond vol reacts should we get a continuation of the squeeze move.

Source: Refinitiv

A rapid spike in yields was previously considered a market risk

SPX had its first >+1% day since July 23. A confluence of factors contributed to the risk-on behavior. VIX falling below 20 also helped. Inflation L/S best factor, 6M Momo worst. Cyclicals over Defensives. SVX beat SGX by 47bps but Barra Growth outperformed Value. The 10Y closed at 1.423% vs. 1.301% yesterday; the large move in bonds was not met with increased Equity Vol. A rapid spike in yields was previously considered a market risk.”

USD futures appear to be consolidating beneath yesterday’s Master Cycle high. Although Wave (C) is roughly equivalent to Wave (A), the correction can go considerably higher, from 98.30, the 61.8% retracemment value, to as high as the Weekly Cycle Top near 100.00. But first, there should be a retracementat least down to mid-Cycle support at 91.51.

GKX crossed above its mid-Cycle support/resistance at 407.56 and is testing its 50-day Moving Average at 412.09. A rally above that level puts i into a buy signal that may last through mid-December. You can see that Wave [2] appears to be in a modified running correction, where Wave (C) ends higher than Wave (A). This is very bullish, since the technicals imply a possible doubling in food prices. It may also cause a lot of suffering among low income families, who are already having trouble putting food on the table.

ZeroHedge reports, “UK politicians are in utter panic as similarities to the 1970s-style “winter of discontent” of shortages and socio-economic distress could rear its ugly head in the coming months, according to Reuters.

A significant driver in what could very well be a hellacious winter for Brits is soaring natural gas and electricity prices that have already disrupted segments of the UK economy and sent shockwaves through energy markets, chemical producers, and the food industry, among others. Compound this all with labor shortages thanks to Brexit, and the dire situation may worsen.

Some Brits who remember the past worry a winter of discontent could be imminent. Many are facing extraordinary high power bills and sharp food inflation that are eating away at wages, along with shortages of goods at supermarkets.”

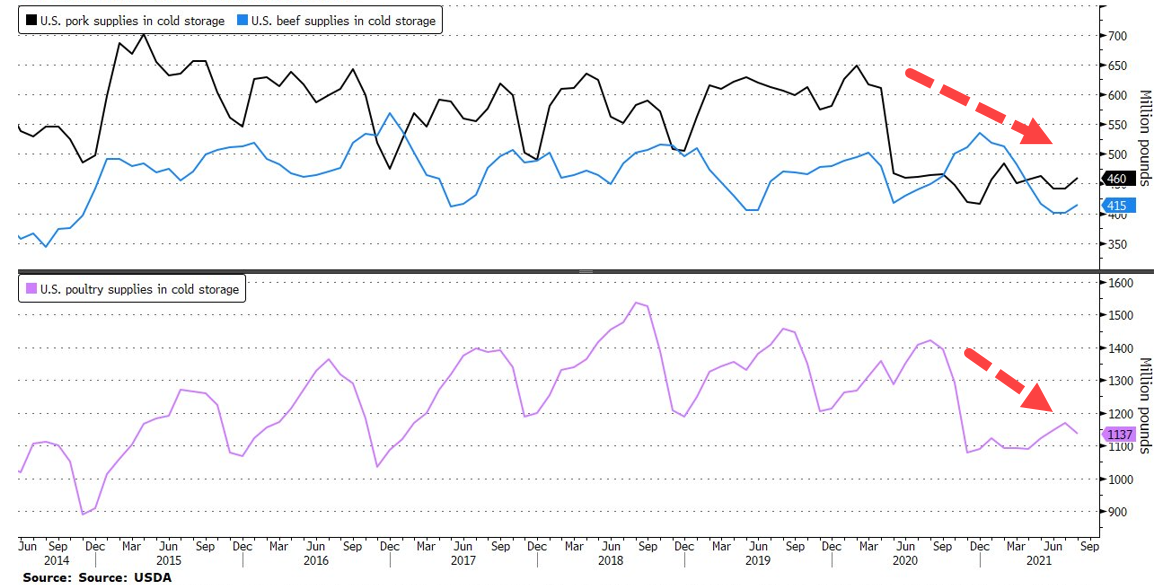

Closer to home, ZeroHedge observes, “Beef, pork, and chicken in US cold storage warehouses have yet to recover from pandemic lows and could continue to support higher prices.

New United States Department of Agriculture (USDA) data shows beef reserves dropped 7.7% from a year ago in August, poultry supplies fell 20%, and pork plunged 44% to their lowest levels since 2017, according to Bloomberg.

Jim Sullivan, commercial director for Stable USA, said low meat inventories would suggest meat prices will stay elevated.

“Prices remain very elevated compared to seasonal expectations,” Sullivan said. “