1:24 pm

SPX has retraced most of the way to its trendline near 4485.00. The 50% retracement value is 4490.78. Currently it has gone to 4479.91, just above the 38.2% Fib retracement at 4477.72 in a Wave [a] of 2. Wave [b] of 2 may be quite deep, with a floor near 4400.00. The final surge may be on Friday, where it may revisit the trendline as it rises to +/- 4490.00. We may see volatility go through the roof should the decline go beneath the 50-day Moving Average.

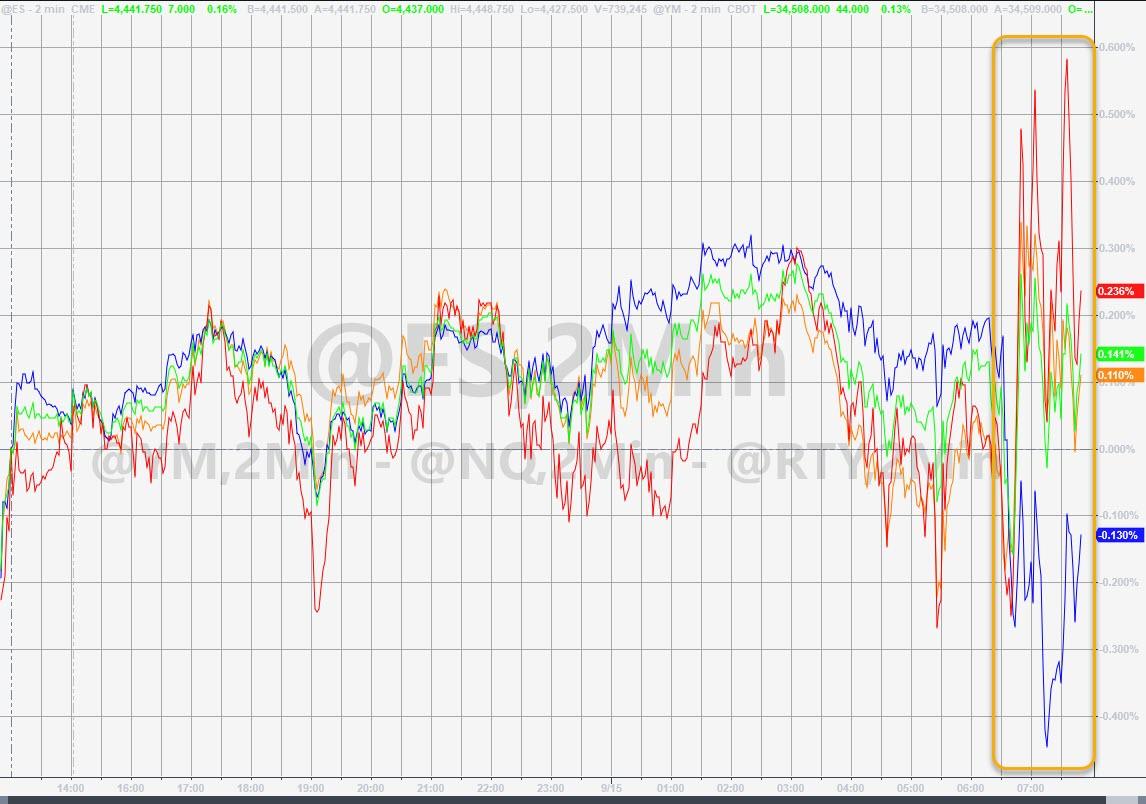

ZeroHedge comments, “This morning’s chaotic trading in stocks could be indicative of the pull and push that Nomura’s Charlie McElligott sees playing out over the next week or so.

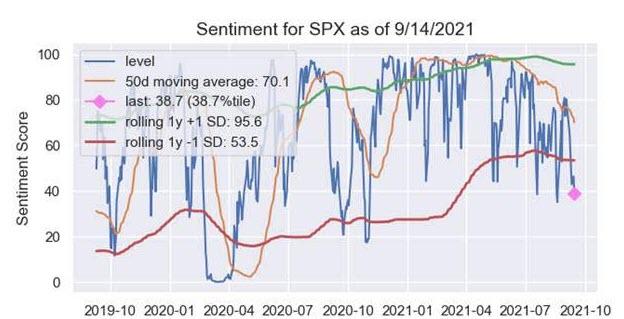

Specifically, Nomura’s SPX sentiment index is cratering and at 38.7%ile, back near lows of the year.

Forward returns backtest to show sideways for the next 1m with negative excess return.

But it is the ultra-short-term which is most interesting…”

7:30 am

Good Morning!

SPX futures remained within a 16-point range of yesterday’s cloose. This afternoon we may see an 8.6-day decline completed near the 50-day Moving Average at 4425.04, followed by a bounce into options expiration. A 50% retracement of this decline will put SPX back up to 4485.00, near the trendline.

Today’s expiring options are heavily weighted with puts at 4450.00 and beneath. The maximum pain level is 4465.00, suggesting a possible close in that area. Friday’s optiosn expiration shows a wide neutral stance with puts dominating at 4400.00 and below, calls domination at 4500.00 and higher. A gamma-induced sell-off to 4400.00 is possible today, but may still bounce back toward the trendline by Friday.

ZeroHedge reports, “While Microsoft did everything it could to halt the recent market drop which has dragged stocks lower on 6 of the past 7 days with its surprising announcement of a record, $60 billion stock buyback, the latest dismal data from China which missed across the board with retail sales, industrial production, fixed investment, property sales and investment all came in worse than expected, with retail sales growing at the slowest pace since August 2020 while industrial output also rose at a weaker pace from July…

… left a sour taste in the market, and left futures trading just barely in the green, higher by 0.1%, while Asia stocks dropped as weak Chinese economic data reinforced worries about slowing growth globally as well as in the world’s second-biggest economy amid fraught nerves over a still-dominant pandemic and tapering of central banks’ stimulus; European markets lacked direction. S&P 500 E-minis were up 5 points, or 0.11% at 07:20 am ET, Dow E-minis were down 16 points, or 0.04%, while Nasdaq 100 E-minis were up 28 points, or 0.18%. The dollar was steady and oil gained.”

VIX futures have remained neutral in the overnight session. VIX may decline to the 50-day Moving Average in the next couple of days. Today is monthly options expiration for the VIX and I would expect most of the decline to happen before the close. In today’s options expiration, puts dominate at 21.00 and lower, while calls dominate from 24.00 and higher. A negative usrprise to the market may spike VIX to 25.00.

NDX futures rose to 15438.00 in th eovernight session, but have come down since. NDX options are very light, but the QQQ (Price: 375.26) options chain shows puts d0minating at 376.00 and lower. The decline in the NDX is incomplete and negative gamma may induce a further sell-off to the mid-Cycle support at 15259.50 or possibly lower. The 50-day Moving Average stands at 15086.06. This may induce a sell off in the SPX as well…an accident waiting to happen.

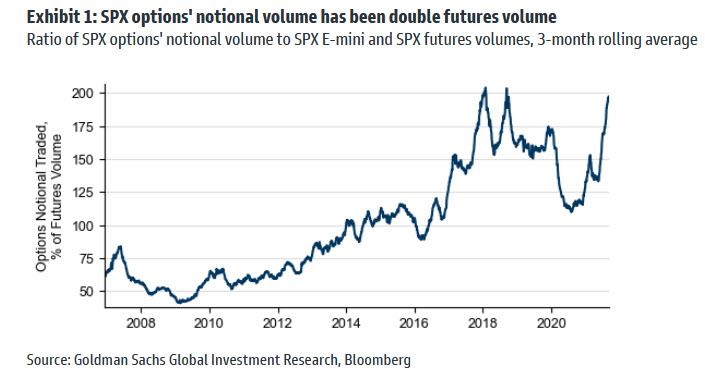

ZeroHedge observes, “Now that stocks have emerged from their 5-day losing streak, narrowly averting 6 consecutive days of declines which would have been the longest such streak since the February 2020 depths of the covid crisis, attention shifts to the market’s technicals and especially Friday’s upcoming quad-witch which sees some $1.5 trillion in SPX option expirations, as well as $1.4tln in options across underlyings expiring on Friday afternoon, including the 2nd largest expiration for single stocks outside of a January.

Courtesy of Goldman, here Four observations on option positioning ahead of Friday’s quarterly maturity:

1. Option volumes have been continuing to grow relative to delta-one volumes. Both index and single stock option markets have shown volume growth in Q3, while delta-one volumes (futures and shares) have fallen. Having traditionally traded well below 100%, SPX options notional volumes are now double the volume of futures traded.”

TNX declined this morning and may be on its way to 11.00 by Monday. That move may sent UST to 135.00 at the same time. Friday’s options chains for TLT (Price: 151.11) shows it is heavily dominated by calls and positive gamma may take over with today’s move sending treasuries higher.

The GSCI Agricultural Index may have made its Master Cycle low on Friday, September 10 (day 249). This Master Cycle shows relative strength as it is ready to move to new heights instead of new lows (in stocks), as it bounces off the 43-week Moving Average (not shown). The new Cycle may last until mid-December. In the meantime, we may expect food prices to possibly double by the end of the year.

ZeroHedge warns, “An executive of Kroger, one of the largest supermarket chains in the United States, warned grocery prices are about to become even higher this year as inflation sets in.

Inflation is running hotter than previously anticipated, and prices are slated to rise an additional 2 to 3 percent over the second half of 2021, Kroger CFO Gary Millerchip said during a call with reporters.

Kroger will be “passing along higher cost to the customer where it makes sense to do so,” he said on Sept. 10.”

ZeroHedge further notes, “Spot prices for nitrogen fertilizer on the US Gulf Coast skyrocketed to a near-decade high on a report the world’s largest nitrogen manufacturing plant declared force majeure.

CF Industries Holdings Inc. in Donaldsonville, Louisiana, closed its massive complex ahead of Hurricane Ida. The complex has 19 plants, including six ammonia and five urea facilities, producing nitrogen-based products for agricultural and industrial markets.

According to the letter seen by Bloomberg, CF Industries said, “due to these circumstances, CF Industries Sales, LLC has declared an event of force majeure affecting the production and shipment of product from the CF Donaldsonville, LA nitrogen complex.”

The letter was dated Sept. 3, and at that time, the facility remained closed. This stoked fears of production declines at a time when supplies are already tight.

As a result of the force majeure, US Gulf urea nitrogen fertilizer spot prices spiked 16.5%, according to Green Markets data.”

The Shanghai Composite Index plunged beneath the Cycle Top resistance, giving it a sell signal. The Bank of China has been giving the market ample liquidity to the point of nearly overtaking the previous high at 3731.69, missing by only 9 points on Friday. Now we know why there appears to be a sudden liquidity drain 12.9 years after Lehman.

ZeroHedge observes, ” Yesterday, when covering the non-stop drama surrounding China’s most insolvent property developer, Evergrande, we said that it would be remarkably ironic if Evergrande were to announce a default – which everyone knows is coming – today, on the 13th anniversary of Lehman’s bankruptcy filing on Sept 15, 2008.

Well, in this delightfully absurd world we live in, that’s just what happened only instead of Evergrande making the announcement, it was the entity that will soon control the massively overlevered property developer that made it for them: the Chinese government.

According to Bloomberg, Chinese authorities told major lenders to China Evergrande Group not to expect interest payments due next week on bank loans, which takes the cash-strapped developer a step closer the nation’s largest modern-day restructurings, and guarantees that China’s “Lehman Moment” is now just a matter of days, if not hours.”