10:25 am

Now that SPX has risen to a new high, it appears to be aimed directly at the Cycle Top resistance at 4468.30. The triangle formation tells us that this is the final move to the peak.

The VIX made a new (Master Cycle) low this morning at 16.08 in an all-out effort to keep equity momentum high. Unfortunately, at day 275 in the SPX, the Cycle may be totally exhausted.

7:30 am

Good Morning!

SPX futures challenged yesterday’s low at 4430.00 by declining to 4427.60 this morning. The (cash) low may act as a trigger point for a short position. Yesteray’s high at 4445.21 did not even achieve the minimum move out of a triangle at 4446.82. Time has run out on the 274 day-old Cycle. The Cycles Model suggests the new Master Cycle (low) may occur on August 26 after 12.9 days of decline.

ZeroHedge reports, “Another day, another extremely tight range of overnight futures trading – with spoos stuck in a 1% range for the past two weeks, it feels as if nothing can push the index away from its massive gamma gravity around 4,400, although today’s CPI – if it shocks either higher or lower relative to expectations – may be just the trigger that breaks this boring rangebound market. 10Y Yield rose as high as 1.375% as the dollar tracked the move higher.

Amid muted trading volumes, S&P futures dipped slightly lower from a fresh record ahead of data out today showing U.S. consumer prices probably jumped again in July; Nasdaq futures fell on Wednesday, while Dow indicators rose slightly as investors swapped heavyweight technology stocks with economically sensitive sectors following the approval of a U.S. infrastructure bill. At 745am ET, Dow e-minis were up 2 points, or 0.1%, S&P 500 e-minis were down -5 points, or 0.11%, and Nasdaq 100 e-minis were down 31points, or 0.2%.”

NDX futures are still attracted to round number support at 15000.00. However, it has broken the Ending Diagonal trendline leaving Short-term support at 14976.24 as the final confirmation of the uptrend.

VIX futures rose to the 2000 gap trendline at 17.08 in the overnight session. The 50-day Moving Average at 17.39 gives us the buy signal for the VIX after last Friday’s Master Cycle low.

USD futures made a new high at 93.19 before pulling back, still in positive territory. The Cycles Model offers a triple dose of strength next week, so we may see a further pullback in anticipation of that robust momentum.

Gold Futures probed above the Broadening Wedge trendline at 1730.00 today. Monday’s low at the Head & Shoulders neckline may not be the final low. We will know further in the next week. Unfortunately, “buy the dip” will be heard all the way to the bottom, where there will be silence.

Gold Futures probed above the Broadening Wedge trendline at 1730.00 today. Monday’s low at the Head & Shoulders neckline may not be the final low. We will know further in the next week. Unfortunately, “buy the dip” will be heard all the way to the bottom, where there will be silence.

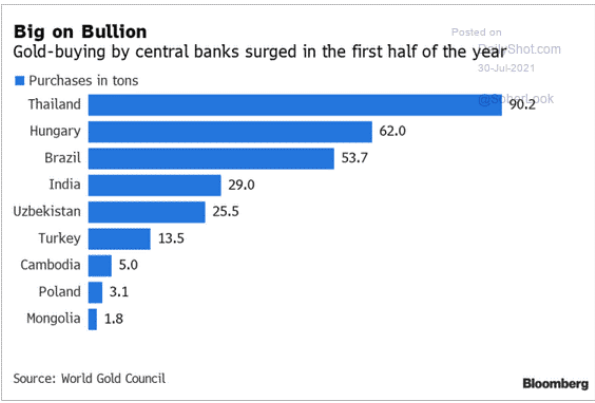

ZeroHedge observes, “Below we unpack the implications behind central bank gold purchases (rising), negative real yields (falling) and Stanley Fischer’s Fed-speak (cringing).

What Bankers Do, Rather Than Say

By now, the open farce as to “central bank transparency” has been made abundantly clear; looking for plain-speak honesty in such circles is akin to looking for an honest man in parliament.

Thus, rather than just follow what central bankers say, it’s often far wiser to watch what they do.

Central Bank Gold Purchases

Toward this end, it’s worth noting that central banks have been buying gold lately, and at significant levels.”

TNX futures rose to a new high at 13.78, suggesting the cash market has further to run. The next resistance is the 50-day Moving Average at 13.93. The next Master Cycle (high) may terminate during the week after the September options expiration.

ZeroHedge observes, “While nerves may be rising ahead of tomorrow’s CPI print which – if it comes in hotter than expected – could ensure a taper announcement is coming as soon as this month, that was not on exhibit during today’s first of the week refunding coupon auction, in which the Treasury sold $58 billion in 3Y notes to surprisingly strong demand.

The high yield of 0.465% stopped through the 0.468% When Issued by 0.3bps, the biggest stop through since March and followed last month’s 0.2bps tail. The yield was modestly higher than last month’s 0.426%.

The bid to cover of 2.541 also came in strong, rising from last month’s 2.411 and also above the six-auction average of 2.450. In fact it was the highest since March 2021.

The internals were quite solid too with Inidrects awarded 55.4%, well above both July’s 53.2% and the six-auction average of 2.450. And with Directs taking down 18.4%, a number in line with recent auction and the highest since Dec 2019, meant that Dealers were left with just 26.2% which was the lowest since August 2017.

Altogether a very strong start to the week’s coupon issuance however it appears to have been priced in as 10Y barely shrugged in response. Tomorrow’s $41 billion 10Y auction will be another story, however the solid demand for the front-end today suggests that worries over tomorrow’s CPI print may be exaggerated.”

The GSCI Ag Index has another week or more to break out above the Wave (B) high and re-esablish the uptrend. It is above the 50-day Moving Average at 410.41 and on a buy signal. but the trend is still uncertain. With the drought, heat and wildfires in the US, processing plants in Canada on strike, drought and cold in South America and floods in China and Europe, the fundamentals indicate food demand may outstrip supply very soon.

ZeroHedge advises, “Brazil’s top producing regions for coffee, oranges, and sugar have been devastated by the worst weather in decades and could leave a lasting impact on prices, according to Bloomberg.

The South American country is one of the world’s leading coffee, sugar, and orange producers experienced a cold snap and drought this growing season in the Center-South area that has significantly damaged crops.

We have focused on coffee and orange markets and how prices are sloping higher after harvest output will likely come in well below average.

Now we’re setting our eyes on the sugar market, where losses in production, exacerbated by an already tight global supply, is fueling higher prices that may be sticking around for the next 18 months. ”