7:40 am

Good morning!

SPX futures are higher this morning, but not making new highs. Thursday’s high at 4429.97 remains the peak of this Cycle at day 262 but the breakdown has not occurred. In the options market, the calls prevail at 4400.00 and higher, while the puts open interest dominate bneath that with 4350.00 as a breakpoint that may induce forced selling. Today is day 266 of the old Master Cycle, should it revive. The Wave pattern apears incomplete.

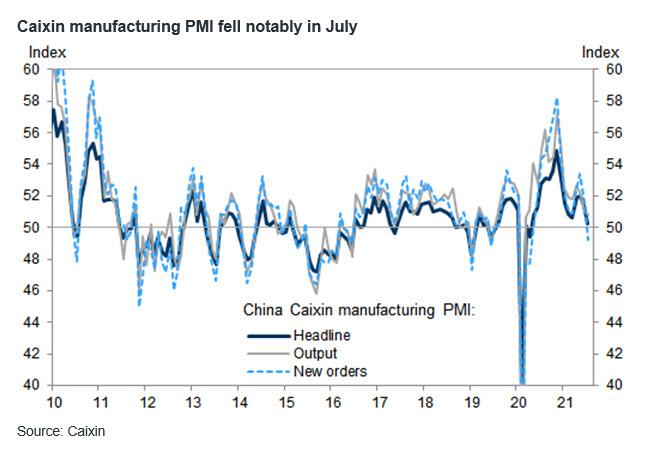

ZeroHedge reports, “Any other day, especially with traders so on edge over anything to do with China, futures would be deep in the red after Beijing reported another sharp drop in the Caixin manufacturing PMI, which slumped from 51.3 in June to 50.3, missing expectations of 51.0 and on the verge of contraction while the new orders sub-index did contract, sliding to 49.2 from 51.6, the first time below 50 since last May….

… but not today, and instead Chinese stocks surged by the most in ten weeks as traders rushed to buy everything from baijiu producers to construction firms on expectations of increased support for the economy after Beijing signaled it would intensify policy support in the second half of the year to bolster the country’s economic growth amid deceleration, China Daily says in a report on Monday and confirming what we reported two weeks ago in “China’s Credit Impulse Just Bottomed With Profound Implications For Global Economies And Markets“.

The Shanghai Composite Index rose back to its Head & Shoulders neckline after plunging to Cycle Bottom support at 3304.40 on Wednesday. This constitutes a 50% retracement of the decline thus far. There may be a further move to 3480.82 to meet the neckline and mid-Cycle resistance. However, the retracement may be over or nearly so. Wall Street makes up chatter to explain the moves in a cause-and-effect pattern. The fact is that the social mood has changed and no amount of jawboning or stimulus will change the Cycle.

ZeroHedge reports, “We noted last week that the delta variant has finally arrived in China, causing one of the country’s worst outbreaks since the original wave of COVID that spread from Wuhan across China (and world). Well, despite authorities’ best efforts, the outbreak appears to have worsened over the weekend, and now officials are reimposing COVID-related restrictions in Beijing for the first time in months as questions about the efficacy of Chinese COVID vaccines multiply.

According to Bloomberg, the outbreak is now the broadest since the original outbreak in late 2019 as cases are being found in 14 of 32 provinces. The fact that delta has spread so widely across China – even if the case numbers, which are likely under-reporting (perhaps dramatically) the true levels of delta penetration, are still relatively low – is alarming government officials.”

NDX futures are back above 15000.00, but no new high here, either. The Wave pattern also appears incomplete, but time is running out for a Master Cycle extension. The trendline is at 14800.00 for a chart sell signal. The NDX Hi-Lo Index closed at 33.00 on Friday so there is not much gas left in this tank.

VIX futures are on the rise, but haven’t broken above Friday’s high at 19.72. The trend is solidly higher, but VIX must break the trendline just above 22.50 or the prior high at 25.09 to convince traders that it’s time to panic.

TNX is entering its final week of the current Master Cycle. Today is day 255 so the probability of an imminent new low and reversal is high.

ZeroHedge observes, “Citius, Altius,Fortius – the Olympic motto – which translates to Faster, Higher, Stronger, might as well be our current motto for Treasury yields. We think that the Treasury market will price in a faster pace of rate hikes, resulting in higher US 10-year yields, consistent with a stronger economy.

We think that 10-year yields are too low versus our fair value estimate at ~1.60%, in large part due to positioning unwinds in recent weeks that have magnified the impact of negative COVID-19 headlines. In our view, yields do not appropriately reflect the strong US economy, or the Fed’s stance. With cleaner market positioning, our economists’ expectations for strong labor market and inflation data, and our base case for a deficit-funded infrastructure package, we see yields rising in the coming weeks.”