3:30 pm

I had been warning since yesterday that trending strength was on the increase. It appears that the increase in strength will continue through the weekend. A breakout above the 50-day Moving Average at 15.37 may be in order…

ZeroHedge reports, “After two mediocre coupon auctions were staggered on Monday ahead of today’s sale of 30Y paper in the form of a 29-Y 10-Month reopening, the bond market seemed content that there would be no fireworks. Alas, the bond market was wrong again, because moments ago the Treasury sold $24BN in what can only be called an ugly auction, if nowhere near as ugly as the infamous February 7Y auction.

With the When Issued trading at 1.976%, the market was expecting the first sub-2% high yield since February. It wouldn’t get it because the auction priced at exactly 2.000%, tailing the When Issued by 2.4bps, the biggest tail since last August.

The Bid to Cover of 2.193 was also quite ugly, down from 2.29% last month and the lowest since February. It was also below the six-auction average of 2.32.

The internals likewise were disappointing, with Indirects taking down 61.1%, down from 64.0% in June and below the 62.4% average. And with Directs taking down just 16.6%, the lowest since November, Dealers were left with 22.3% of the allotment, the most since October.”

3:15 pm

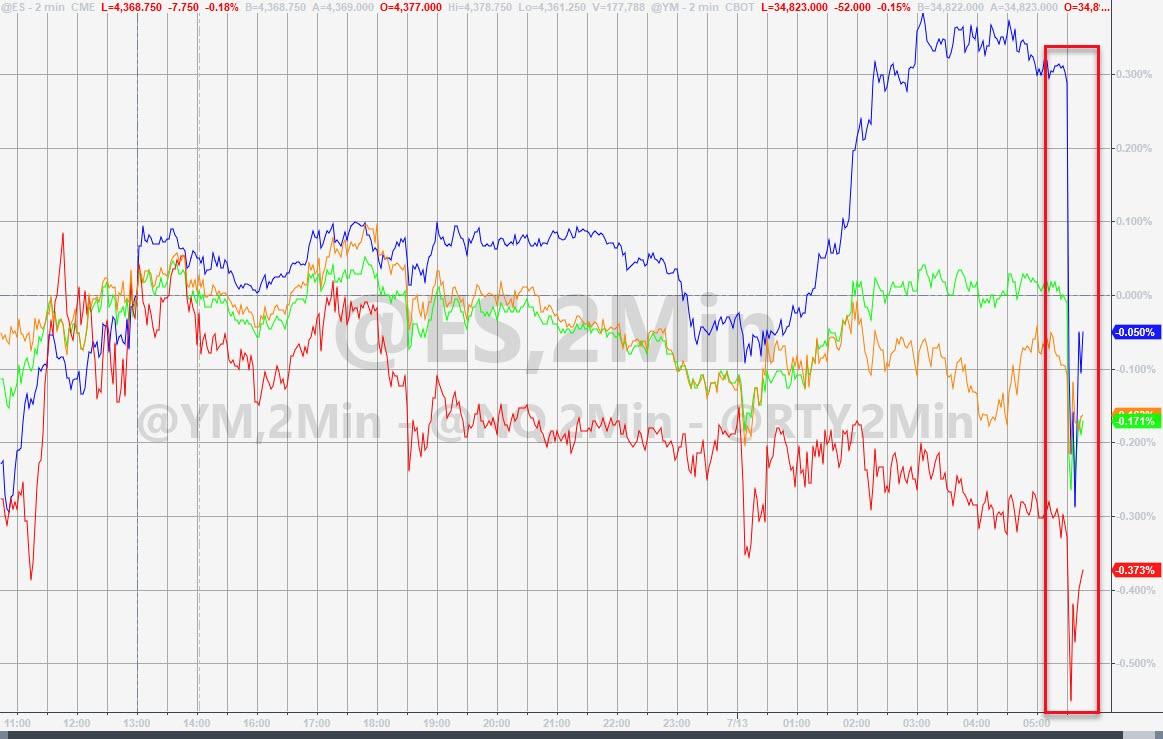

SPX had declined beneath its Cycle top resistance at 4377.00. This puts us on alert that the probability of a reversal is at hand. For tomorrow’s SPX option expiration, there are 1000 more puts than call contracts at 4370.00! Should the SPX continue down, we may see an acceleration to the downside. I had been commenting that there was evidence of substantial distribution by institutional investors. See the comment below. Is Goldman Sachs pulling out the rug from under us?

ZeroHedge remarks, “While most analysts and traders were digging through Goldman’s investment banking and trading results – of which the former came in stellar while trading, especially in FICC, was mediocore…

… when the bank reported its second best quarter on record, there was some more notable slide in the bank’s Q2 earnings presentation, and it had to do with what Goldman is doing for its own prop, or “asset management” book.

As shown in the table below, Goldman’s Asset Management (F/K/A “prop”) also had a stellar quarter, generating a record $5.1BN in net revenue, more than double the year ago quarter.”

8:15 am

Good Morning!

Earnings Season is kicked off with two Major banks, Goldman and JPM. SPX futures made yet another all-time high at 4378.62. Futures currently trade about 12 points beneath the cash market, suggesting a morning high near 4390.00. The Cycles Model suggests another Master Cycle high may be due. Notice that the last two Master Cycles ended during options week. This one may be due either this week or early next.

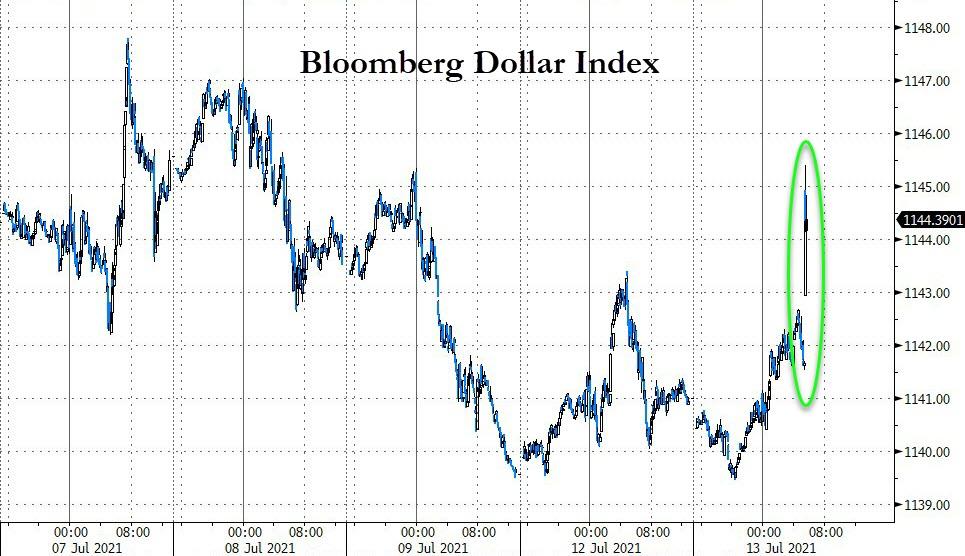

ZeroHedge reports, “The dollar spiked after the much hotter than expected CPI print…

Source: Bloomberg

Stocks were slammed…

…and bond yields rose…

VIX futures made a low of 15.96 last night, but spiked higher this morning. Note the coiling action of this year-long pennant formation. This pennant infers a move as great or greater than last year’s rally (approximately 75 points).

Yesterday, NorthmanTrader observed, “Last week in “Crushed” we talked about a coming volatility spike and sure enough $VIX spiked to over 20 from the 15 handle in a matter of days only to be crushed again. Thursday’s one hour 1.7% dip on $SPX was once again ferociously bought and new highs have once again ensued, no matter what the internal picture of the market may be, which continues to rally irrespective of the lack of participation underneath the surface.

Just this morning we got a taste of this:”

NDX futures also made a new all-time high, but switched direction at 7:00 am and are clearly in the red as I write. What has triggered this is unknown, but it appears to be serious. Is this the Master Cycle High?

US 30 futures turned down at 7:45 am after a flat overnight session. Note that a new all-time high has not been accomplished. This has serious implications going forward , not only due to a Master Cycle change, but because a lower high infers that the most violent of declines may be straight ahead in Wave 3.

BKX, our proxy for market liquidity is sitting on the neckline of a Head & Shoulders formation that implies an approximate 25% decline, or greater. A breakthrough at 118.70 appears to “pull the plug” on market liquidity.

ZeroHedge reports, “”Transitory” or not? That’s the question today as all eyes dives into the details behind the surge in Consumer Prices for signs that Powell’s plan is failing. BofA forecast headline and core CPI prints to come in hotter than expected (and they’ve nailed every print this year) and they were right again with a massive beat – Headline CPI rose 0.9% MoM (against expectations of +0.5%), the biggest MoM jump since June 2008. This sent YoY headline CPI soaring to +5.4%,”

TNX is trading on strength this morning and may be due for stronger moves in the next week or so. This is especially ironic, since a 10-year auction was held yesterday.

ZeroHedge reports, “inety minutes after today’s first auction, when the Treasury sold $58 billion in a somewhat subpar sale, moments ago the Treasury followed up the 2nd coupon auction of the day when it sold $38 billion in benchmark 10Y paper in today’s 9-year 10-month reopening which also could have gone better.

The high yield of 1.371% – which stopped through the 1.374% when issued courtesy of a substantial concession throughout the day – was well below last month’s 1.497% and was in fact the lowest high yield for the tenor going back to February when it priced at 1.155%. However, the Fed’s hawkish pivot which spooked the bond market with traders fearing about the plunge in r* has pushed yields sharply lower in recent days and sure enough today’s 10Y auction yield was the lowest in 5 months.

Besides the dip in the high yield, the auction also saw the bid to cover slide to 2.39 from last month’s 2.58 and the lowest since April’s 2.36.”

USD futures leaped to a high of 92.71 this morning. The Cycles Model suggests a strong follow-through for the next week or two. A new Master Cycle high maybe due by the end of the month.