7:45 am

Good Morning!

NDX futures continue to make all-time highs, although only by a few ticks. Retail investors continue to buy the dips while institutional investors are absent. The Fed is furiously pumping while the markets begin to sag. Someone should tell Jay Powell that the markets rise (and fall) on confidence, no matter how much money is thrown at it. As more big (smart) players leave the game, the realization that it isn’t the same trickles down to the retail end who are constantly searching for momentum plays until there are no more.

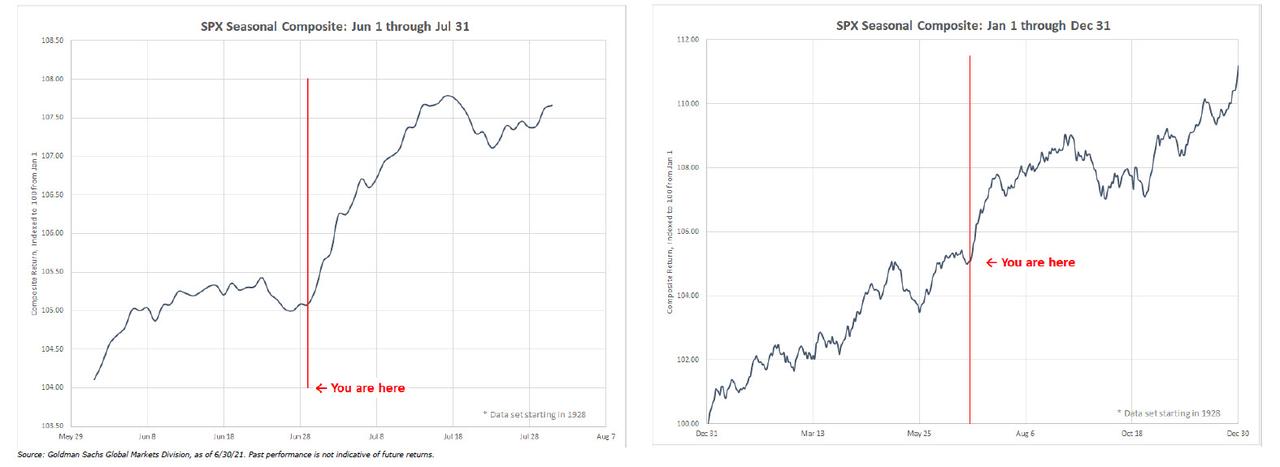

ZeroHedge comments, “Just a few days after Goldman trader Scott Rubner observed last week that the market is entering the best 2-week seasonal period of the year …

… he is out with a follow up note, in which he first points out a striking market statistic:

S&P 500 logged 7 straight trading days with a new ATH, this has only happened 5 other times since 1928. If today logs another all-time high, that has only happened 3 other times in history. No streak marked an immediate or significant top in the markets. Since 1928, if the S&P 500 is above >10% in 1H, then 2H performance is nearly 2x the median final 6 months for all years.

… but it was his observation on the rate of fund flows that was truly remarkable:

In 18 years of tracking flow of funds I could not imagine typing these large of numbers. I needed to check them twice. This was my busiest weekend and most incoming client questions of 2021 by far.”

On the opposite side of the spectrum DJIA futures remain flat after yesterday’s drubbing. This is the (increasingly former) home of major institutions and hedge funds that insist on liquidity and safety. The peak remains on May 10 and the tires on this buggy are slowly deflating. The wheels may come off sooner than one can imagine as the DJIA crosses beneath the 50-day Moving Average at 34251.50. The final destination in the next 90 days may be beneath 17485.00 .

SPX futures made an overnight high at 4345.00, unable to beat yesterday’s (futures) high of 4347.00. The SPX still appears to be bullish, but the fervor may be gone after last week’s blow-off top. Today is day 271 of the current Master Cycle, making it a very stretched affair should a new high be made.

ZeroHedge reports, “One day after the S&P broke its near-record winning streak of 7 consecutive all time highs, futures resumed their grind higher as world stocks steadied below recent record peaks, while the Nasdaq jumped to a fresh all time high as the continued drop in Treasury yields supported tech-heavy growth stocks, with investors eyeing today’s June FOMC minutes for clues on policy support going forward. At 730 a.m. ET, Dow e-minis were up 21 points, or 0.06%, S&P 500 e-minis were up 8.25 points, or 0.19%, and Nasdaq 100 e-minis were up 89.25 points, or 0.59%. 10Y yields slipped for the seventh straight session, amid concerns about the economic outlook and coronavirus variants, helping Nasdaq futures rise premarket.

The NYSE Hi-Lo Index tells us more about the waning confidence in the markets. The majority of June was spent beneath the 50-day Moving Average at 215.38. While not enough for a sell signal, it shows a quiet liquidation/distribution since the high on May 10. I had mentioned that a close beneath 50.00 may be a sell signal. Under the current outlook, a close beneath the June low at 0.00 may be a better indicator of a sell signal.

VIX futures are flat this morning after testing the 50-day Moving Average at 18.08 yesterday. The VIX appears calm, but its declining wedge (pennant) formation suggests a rally at least as large as the one in 2020 from a higher base.

TNX may have (finally) made its Master Cycle low at an incredibly stretched 281 days this morning. Treasury shorts are being pummeled.

ZeroHedge remarks, “After a modest stabilization overnight, the collapse in 10Y yields has resumed this morning tracking the latest drop in oil, which is down following a WSJ report that the UAE plans to “sell as much crude as possible before demand dries up” and aims to boost production and market share unilaterally amid high demand in threat to OPEC stability.

As a result of the latest deflationary gust, 10Y yields have dropped below 1.30%, sliding to the lowest since February 19…

… as the short squeeze discussed yesterday – as a reminder the latest JPM Treasury Client Survey found a near record number of shorts – accelerates.”

USD futures made an overnight high at 92.60 as it lingers near its Master Cycle high. The Cycles Model calls for an approximate two week decline to the 50-day Moving Average at 90.87 before resuming its rally to 96.00.