8:00 pm

SPX nearly reached the Wave relationship where [v] equals [i] at 4291.00. The topping formation is clearly an ending Diagonal, with overlapping Waves of (a)-(b)-(c). It is interesting that the positive gamma generated by this week’s options expiration brought the final Wave up to the very last hour on Friday. The market is very fragile as the influence of options expiration wears off. As it turns out, next week’s options are heavily weighted toward the puts at 4240.00 and below, barely 1% beneath tonight’s close, keeping a tight “collar” on the SPX movements.

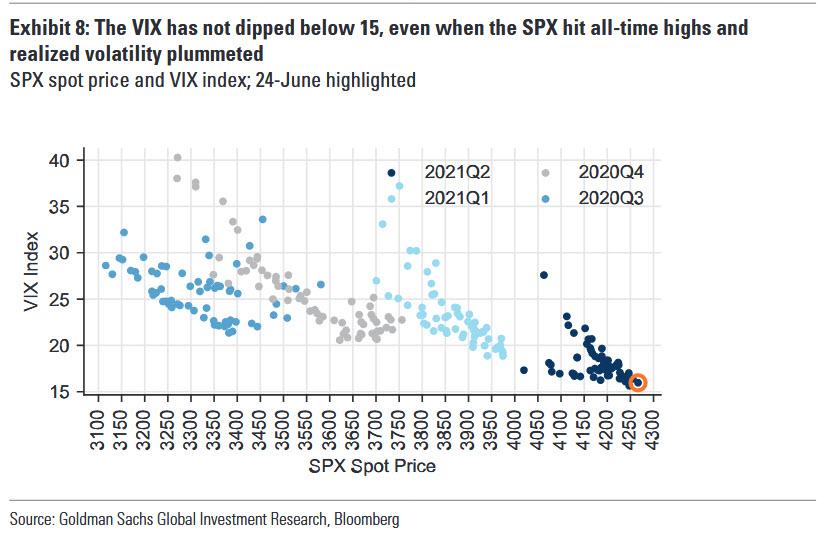

ZeroHedge observes, “With last week’s post-Fed tantrum seemingly a distant memory, spoos just hit a new all time high at 4,275 as low realized volatility helped push the VIX near new Covid-era lows…

… if not the lowest level. Indeed, with the VIX at 16.0, and volatility risk premium elevated, Goldman notes that short-dated hedges are not cheap – especially relative to historically low implied volatility for other key markets (1M SPX implied vol is 43rd percentile vs. the last 5 years, vs. HYG, EEM, and HSCEI all below 15th percentile). As a result, Goldman also sees “heightened potential for realized volatility to approach June’s lows, leaving the VIX with moderate downside.”

The reason why VIX has so far failed to hit new lows despite , as Goldman’s Rocky Fishman explains, is because the skew index just hit a new all time high: this means that put options have been unusually expensive relative to at-the-money options, helping support the put-heavy VIX index. High skew, which compares put option prices with at-the-money option prices, has reached new all-time high, and reflects investor perception that high volatility would return should markets sell off.”

8:25 am

Good Morning!

NDX futures reached an overnight high at 14382.00 and has eased down, leaving yesterday’s 12:00 noon high as the top. I have pointed out that the NDX often leads the rest of the market and this puts us on the alert for the rest of the market to follow.

ZeroHedge reports, “S&P futures traded at record highs, tracking strong gains in Asian markets, as investors braced for the Fed’s preferred inflation data following a tentative bipartisan agreement on infrastructure spending, while U.S. lenders rose after clearing stress tests. At 7am ET S&P futures were up 5.75pts or 0.14%, Dow Jones futs were +110 or 0.32% and Nasdaq futs were up 29.25 or +0.2%. Global stocks are poised for their biggest weekly advance since April, extending their fifth monthly gain.”

SPX futures rallied to 4265.12, just beneath yesterday’s cash high at 4271.28 on day 259 of the Master Cycle. 4265.00 is where Primary Wave [5] is 3.75 times the length of Primary Wave [1]. The normal Wave relationship is that Wave [5] equals Wave [1], so you can see how stretched this relationship is…

Charles Hugh Smith opines, “Risk has not been extinguished, it is expanding geometrically beneath the false stability of a monstrously manipulated market.

One of the most under-appreciated investment insights is courtesy of Mike Tyson: “Everybody has a plan until they get punched in the mouth.” At this moment in history, the plan of most market participants is to place their full faith and trust in the status quo’s ability to keep asset prices lofting ever higher, essentially forever.

In other words, the vast majority of punters are convinced they will never suffer the indignity of getting punched in the mouth by a market crash. What makes this confidence so interesting is massively distorted markets always end the same way: crisis, crash and collapse.”

VIX futures rose to 16.17 in the overnight market after yesterday’s low at 14.19. Another stretched Cycle at 281 days thus far. The snap-back may be atrocious.