2:30 pm

The usual 2:00 pm jolt from the FOMC announcement fell short of the morning high. SPX tested the trendline by declining to 4181.79. It has made a weak bounce. Confirmation of a decline may be made at Short-term support , now at 4145.00, just beneath the lower call option level at 4150.00. Nobody sees a decline coming. See ZeroHedge analysis.

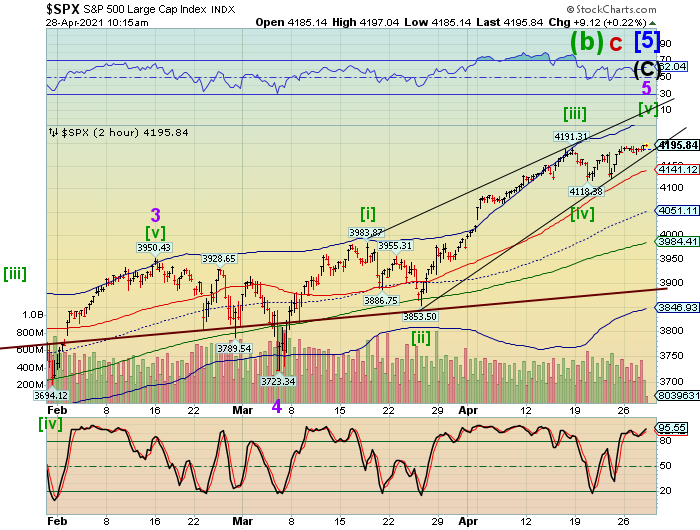

10:15 am

SPX has made a new all-time high at 4197.04and appears to be testing round number resistance at 4200.00. The possibility of a breakout is high, with possible targets at 4240.00-4260.00. Just to give you the magnitude of this bubble, Primary Wave [5] is three times the size of Wave [1] at 4300.00.

Fear of missing out (FOMO) may be the primary driver of tis final probe higher. However, watch out for a decline past 4175.00, which breaks the Ending Diagonal formation.

7:30 am

NDX missed the all time high yesterday by 2 ticks. This morning NDX futures declined to 13907.25, nearing Short-term support at 13840.45. The DJIA futures are also in decline, after failing to make a ne all-time high yesterday. Both are left with tops on April 16, 12.9 months from the March 23, 2020 low. The threat of a new all-time high still exists, but the weakness appears to be profound. The promise of stock buybacks may not deliver the way investors expect.

ZeroHedge reports, “Judging by the just released Q1 blowout earnings from Google, the one thing that companies just can’t do without during the biggest government recession stimmy handout in history, is advertising.

Moments ago, Google parent Alphabet reported Q1 earnings (at the abc.xyz URL) that blew expectations out of the water powered by an increase in digital ad spending by businesses looking to expand during the pandemic reopening:”

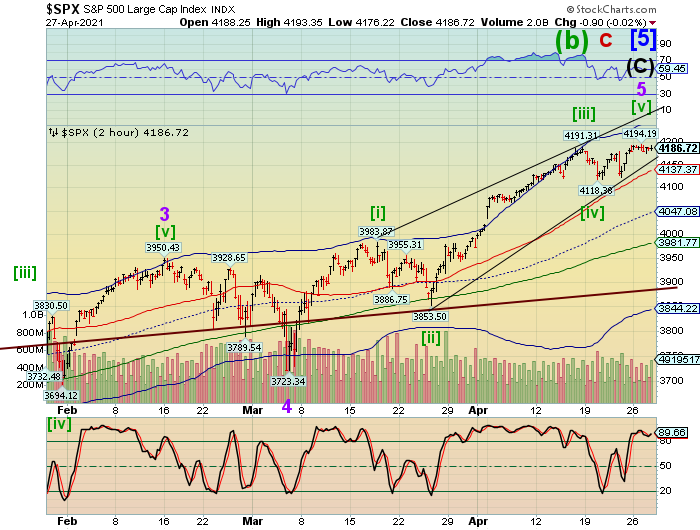

SPX futures made a shallow low a 4175.88, testing the underlying trendline just beneath it. The threat of a new all-time high remains, but may be cancelled by a decline beneath that trendline. Short-term support is at 4137.37, which may confirm the reversal.

ZeroHedge reports, “For the third day in a row, US equity futures were broadly flat, with the emini trading virtually unchanged from where it was this time on Monday and Tuesday as traders hunkered down ahead of today’s main event: the FOMC announcement at 2pm where Fed Chair Jerome Powell is expected to reaffirm that easy monetary policy will remain in place for a prolonged period and dismiss any suggestions of tapering bond purchases.

S&P 500 e-mini stock futures rose 0.09%. or 5 points, while Dow Jones futures were down 31 points ot 0.09% and the Nasdaq was down 7.75 or -0.06% as investors digested a mixed bag of earnings from Tesla, 3M, Microsoft and Google overnight, with tech heavyweights Apple, Facebook and Amazon due to report in the next 48 hours.

“We expect the Fed’s tone on the economy to be more positive than at the March FOMC meeting, reflecting the ongoing pickup in the data, but we don’t expect any substantive new signal yet on tapering,” TD Securities analysts wrote. “While we do not expect much price action due to the Fed decision, Biden’s remarks could continue to suggest more incoming supply, bear steepening the (Treasury yield) curve.”

VIX futures remained muted, with an overnight low at 17.12. The April 14 Master cycle low, although early, continues to point to the April 16 high in equities as the “official” top, despite the nominal new high in the SPX. The Cycles Model shows increasing strength into the month of May, possibly as far as May 18. Biden’s “tax and spend” plan may prove to be the final straw on the back of the bull market.

ZeroHedge reports, “President Biden will head to Capitol Hill Wednesday night for the first time since Inauguration Day (a casual visit by the president would risk spoiling the narrative that the Capitol remains a battle-scarred wreck since the Jan. 6 “uprising”) to unveil the second part of his “Build Back Better” plan, a $1.8 trillion proposal to expand the American “safety net” that will be financed by hefty tax increases on individuals and businesses, including a nearly 40% tax on short-term capital gains that spooked the market when it was first reported last week.

The scale of the plan, which has been named “the American Families Plan” and is intended to compliment Biden’s “American Jobs Plan” unveiled four weeks ago, has increased in scope since the first details of a preliminary version were leaked to the press earlier this month.”

TNX challenged Intermediate-term resistance at 16.36 this morning as it prepares to break above its prior high and the Cycle Top at 17.64. The initial target appears to be the November 2019 high at 19.71, but it may not stop there. The ensuing rally appears to be gathering strength through early June. The next 10-year auction is on May 5.

ZeroHedge reports, “After two mediocre auctions on Monday, when both the 2Y and 5Y sales saw tepid market interest, some rates traders were worried that today’s 7Y auction would be ugly. Not February 2021 ugly, mind you, which we remind readers was the closest the US has had to a failed auction and sparked the furious dump across the curve which spilled over into stock, but still ugly.

Well, besides the smallest possible tail of 0.1bps, it actually was a pretty solid 7Y auction.

Yes, the high yield of 1.306% was the highest since January 2020, rising just above the 1.300% in March, and yes, it did tail the 1.305% When Issued (just barely), but the other indicators were relatively solid.”

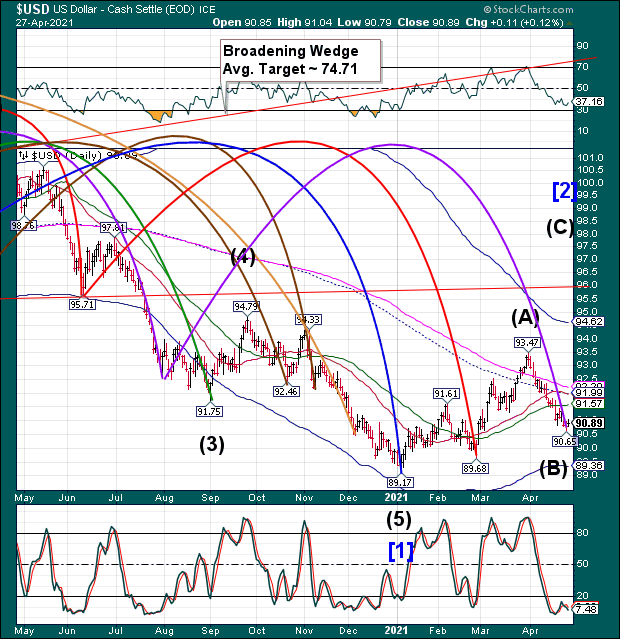

USD futures made a new overnight high at 91.13, confirming Monday’s Master Cycle low. While the USD Cycle is closely aligned with the 10-year rates Cycle, it may be given a boost by the liquidation of equities, as well.

ZeroHedge observes, “The Fed put a lot of effort after the March FOMC meeting into convincing bond investors that it was not thinking of changing its view of low inflation and low policy rates through 2023. There is increased optimism but not additional economic data since, so we think the Fed will try and keep the message as unchanged as possible. The lack of bond yield reaction to sharp data surprises has led investors to be cautious on the immediate upside to bond yields. Real yields are almost 20bps lower than at the March FOMC (Figure 1). There is no real appetite to fight the Fed now and the Fed has little incentive to rock this boat just yet.”