2:32 pm

SPX tested the upper trendline of its trading Channel shortly after 1:30 pm. While it may retest it by the end of the day, the Cycles Model infers that this may be the top at 275 days. Investors may be noticing the mere 1.1% gain in the last 45 days with rising volatility and lower liquidity. There are likely to be some skeletons still hidden in the Archegos failure. In addition, massive tax hikes are being proposed by the Biden administration that are taking some of the excitement out of investing.

Look for a cross beneath Short-term support at 3936.89 for an aggressive short signal. Oddly enough, the DJIA did not make a new high today.

12:28 pm

TNX has pulled back since this morning. However, it appears poised for a surge higher by the end of the week.

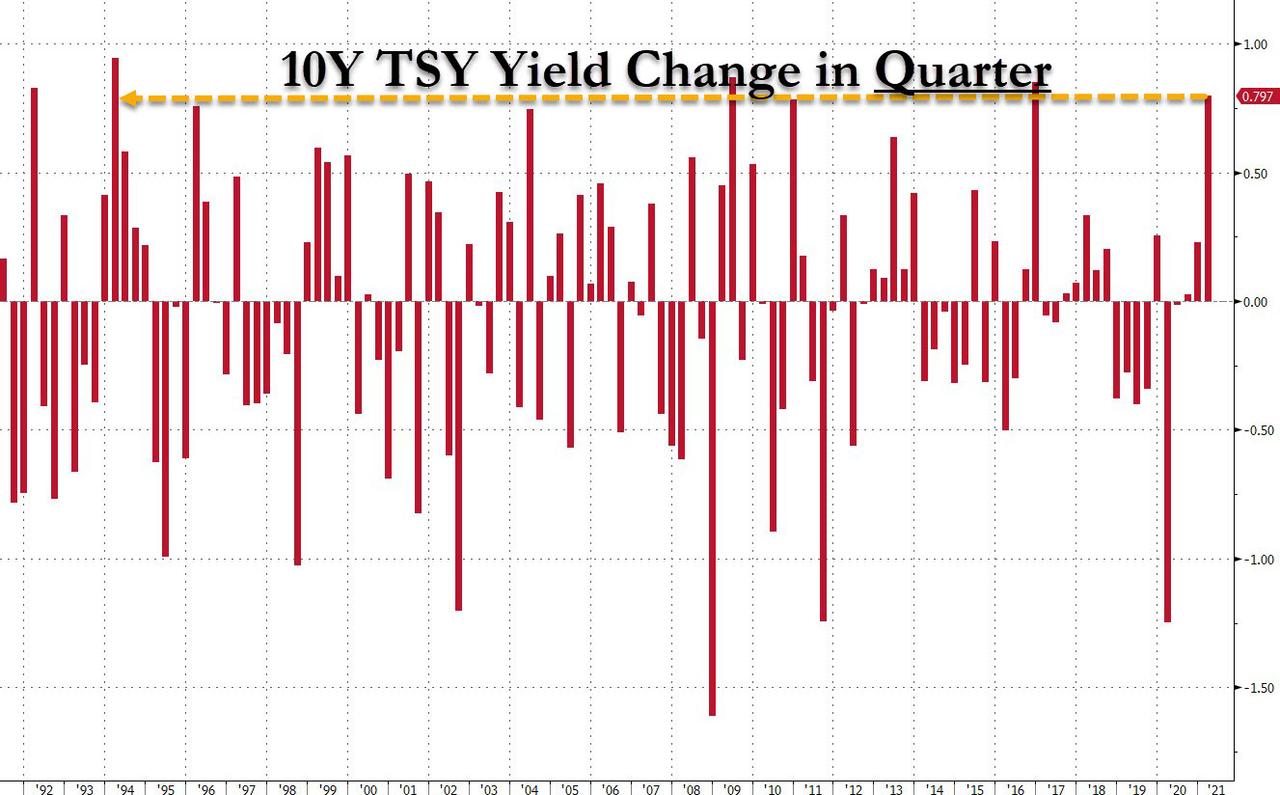

ZeroHedge remarks, “On the last day of Q1, the quarter seems to be ending very much how it began, with Treasury yields rising to fresh highs as investors await the announcement of further spending proposals in President Biden’s infrastructure package while buying stocks first (the S&P just hit a new all time high) and asking questions later.

Indeed, as DB’s Henry Allen writes, the rise in 10yr Treasury yields in Q1 so far had reached a massive +82.7bps (0.797bps at the time of writing), which puts them just shy of the 21st century’s other quarterly records back in Q4 2016 (+85bps) when President Trump won the presidential election, and Q2 2009 (+87bps) as the global economy was climbing out of the financial crisis. Of note: even the 2013 taper tantrum was a far more modest, and slow move compared to what we have seen now.

And while everyone is waiting for Biden to reveal further details from his infrastructure package on Wednesday, should today’s Biden speech spark a further climb in yields, that could then leave this as the biggest quarterly rise going all the way back to the Great Bond Massacre of Q1 1994, when yields blew out +94.4bps.”

10:05 am

NDX shot up to test its mid-Cycle resistance at 13081.33, while stomping the VIX down to 18.90. This is the strongest surge of all the stock indices. None have made new highs. Note the bearish cross of the mid-Cycle with the 50-day Moving Average. Big money is ramping the indices (especially the NDX) to: 1. See if new highs may be made. And 2. Raise FOMO sentiment among the retail investors.

10:15 am The Dow has gone negative…

12:15 pm NDX is now at the 50-day Moving Average and appears to be overbought with Slow Stochastics at 99.7. The DJIA remains at breakeven.

ZeroHedge proclaims, “Well that just happened… Buy Mortimer, buy!

The Dow, S&P, Russell 2000 all spiked dramatically at the US cash open (Nasdaq did not initially then decided to join the momo party because, well, someone must know something right?)

So much for the massive JPM-predicted forced month-end selling!?

No move in bonds or the dollar at all, but gold did pop a little…”

8:00 am

Good Morning!

SPX futures are flat this morning It appears that the effort to preserve the market gains until the end of the quarter may be successful. However, the inability to make new highs tells us that there may be no more fuel in the tank. today may be the last day for an all-out effort to make a new high. However, should this Wave structure be correct, a decline, the magnitude of which hasn’t been seen before, may commence. The first major low, according to the Cycles Model may be at options expiration, or shortly thereafter.

The DJIA also failed to make new highs, suggesting that the indices may now be in sync.

ZeroHedge observes, “US index futures were little changed and global stocks treaded water on Wednesday as Treasury yields resumed their upward march ahead of Joe Biden’s Pittsburgh event where he will announce a $2.25 trillion dollar plan – one which the administration says will be the most sweeping since investments in the 1960s space program and 1950s interstate-highway system – to rebuild America’s infrastructure, with traders weighing the inflation and tax impact of the stimulus.

At 07:30 a.m. ET, Dow E-minis were down 27 points, or 0.06%, and S&P 500 E-minis were up 3.5 points, or 0.09%.

Nasdaq 100 E-minis were up 75 points, or 0.56%, as Apple Inc rose 1.6% after UBS upgraded the stock to Buy on stable long-term demand for iPhones with better authorized service providers.”

NDX futures rose to a high of 12975.75, short of Monday’s retracement high at 13013.50. The Cup with Handle formation is still operative and may be triggered with a decline beneath the Lip just beneath 12700.00. There is some indication that the bloodletting may not be over.

ZeroHedge reported yesterday, “Unlike the devastating London Whale debacle in 2012, which was all JPMorgan eventually drawn and quartered quite theatrically before Congress (and was a clear explanation of how banks used Fed reserves to manipulate markets, something most market participants had no idea was possible), this time JPMorgan was nowhere to be found in the aftermath of the historic margin call that destroyed hedge fund Archegos. Which is may explain why JPMorgan bank analyst Kian Abouhossein admits he is quite “puzzled” by the recent fallout from the Archegos implosion (or maybe JPM simply was not a Prime Broker of the notorious Tiger cub), which however does not prevent him from trying to calculate the capital at risk from the Archegos collapse.

In a note published this morning, Kian writes after Nomura yesterday confirmed (at least) a $2Nn potential claim and fellow Japanese bank Mitsubishi UFJ Securities Holdings announcing today of another potential $300MM loss – which as the JPM strategist admits “for a likely non-material PB player is surprising to us” – JPMorgan now expects losses well beyond normal unwinding scenario for the industry: and explains that it now sees “the losses as very material in relation to lending exposure for a business that is mark-to-market and holds liquid collateral” and makes Nomura’s indication of potentially losing $2bn and press speculation of CSG $3-4bn losses “as not an unlikely outcome” according to the JPM strategist.

So why is JPM surprised?

Because as Abouhossein writes, “in normal circumstances… we would have suspected industry losses of $2.5-5bn. We now suspect losses in the range of $5-10bn.” In other words, JPM has doubled its max loss estimate to as much as $10BN, a number which could yet rise.”

VIX futures took another dip to an overnight low of 19.12. This may be due to the effort by the powers-that-be to maintain the SPX at or near its quarterly high. The new Master Cycle may be due to end at the end of April at a high.

TNX appears to be pulling back from its new high. However, it may be brief, due to the oncoming Master cycle high in the latter part of April. The target appears to be the November 2019 high at 19.71. The Treasury Department announced that it will ramp up offerings/auctions in April to $170 billion.

USD futures pulled back after their breakout above the 200-day Moving Average. The pause in the rally may be brief, as USD is due for a Cycle high at the end of April.

Investing reports, “Stronger than expected economic reports drove the U.S. dollar higher against all of the major currencies. There’s no question that of the G3 currencies (USD, EUR and JPY), the U.S. is leading the recovery, and data is beginning to show the benefits of a smooth coronavirus vaccine rollout. Seventy percent of Americans 65 or older have received at least one COVID-19 vaccine dose, with more than a third of the overall adult population receiving their first jab. Businesses are reopening and economic activity is accelerating. As a result, jobless claims fell to 684,000, its lowest level in more than a year. Fourth quarter GDP growth was also revised up to 4.3% from 4.1%. The U.S. economy is still a long way from normal, but the numbers show that it is moving in the right direction. With more Americans getting vaccinated every day, further improvements are likely. Personal income and spending numbers are due for release tomorrow.”

Gold futures bounced off the Broadening Wedge trendline this morning. The bounce may go as high as the Cycle Bottom resistance at 1707.93 and last until Friday, a day of strength. However, it is due to resume its decline through April options expiration. There appears to be two bearish formations that indicate a very deep decline which may proceed from this juncture.

Investing comments, “Gold spot we wrote: outlook negative and holding first resistance at 1715/17 re-targets 1707/05 then 1700/1698. A good chance of further losses eventually to very important strong support at 1685/75.

What a call! gold collapsed straight to very important strong support at 1685/75 and bottomed exactly here.

This was perfect! The break below hit 1705 and even the bounce topped exactly at 1715/17. Outlook now negative.”