11:54 am

NDX appears to be slipping beneath the Neckline/Lip at 13735.00 which may end the surge from yesterday’s closing low. While the Lip of a Cup with Handle formation is somewhat permeable, the Neckline of a Head & Shoulders formation generally is not. This appears to be the case. So, despite the PPT injection, the NDX is still behaving in a bearish fashion.

ZeroHedge observes, “With a little nudge from China’s plunge protection team, growth/momo traders are panic-buying big-tech this morning, lifting Nasdaq up a stunning 3.5% from last night’s close…dramatically outperforming The Dow (in a total mirror of yesterday’s price action)…

Nasdaq bounced hard off its 100DMA…

But now faces some resistance at recent peaks…”

RealInvestmentAdvice comments, “Last week’s sell-off left the “bull market” on shaky ground.

The big question for investors at the moment is whether the 11-year old bull market is ending or is this just a “pause that refreshes?”

While the optimistic “hope” is that this is just a pause within a continuing “bull market” advance, from a money management standpoint getting the answer “right” is vastly more important to long-term investing outcomes.

The easiest way to approach this analysis is to start with the following basic premise:

“Bull markets are born on pessimism, grow on skepticism, and die on euphoria.” -Sir John Templeton”

Ed. Note: I have been privileged to know Sir John from 1981 to his death. I have some fond memories of interactions with Sir John that I may pass on to my grandchildren.

11:05 am

SPX has morphed into a [1]-[2] formation since the rally is now a 5-Wave affair. It is also now testing the right shoulder target at 3900.00 and completing an expanding Leading Diagonal formation. What a series of whiplashes! The implications are enormous. I had first discussed a crash formation starting at 3928.65, then at 3914.50 and now 3900.00. This may be where the panic decline officially begins. After 15.5 days of going virtually nowhere, the decline may now produce 90% of the damage in the next 4.3-6.45 days.

ZeroHedge observes, “The set up for late March: a lot of selling. We are going from the “best inflow” picture in like forever to what seems to be some heavy equity selling in the second half of March.

1. Pension Rebalance: numbers still unclear but rest assure that there will be large $ equities for sale vs. bonds

2. 60-40 rebalance quarterly will also be a massive number. Given the increase in AUM of 60-40 strategies, the rebalancing back to bonds, which now looks like a 61%/39% or 62%/38% could be big.

3. Systematic de-leveraging. Systematic supply aka de-leveraging is in process given the breakdown from key technical levels. It’s also important to note, that systematic strategies are not buying from here. GS has -21B for sale over the next 1-month. More important, “up big” we have -$8B for sale, but “down big” we have -$180B for sale.

4. Momentum. 12m momentum changes at the end of the quarter is bad for the S&P 500 Index composition. (this is selling large cap and largest weights vs. buying the smallest index weights). There is heavy length in long momentum strategies.

5. Issue with issuance. Issuance remains strong, perhaps too strong. YTD US equity and equity-linked issuance (traditional IPOs, SPACs, follow-ons) is off to the hottest start on record ($139bn raised). Previous YTD record was in 2000 ($70bn raised by this point in the year).

6. Taxes. April 15th tax payments. -$1.64T worth of realized capital gains in 2020.

All this is happening into a poor liquidity tape (S&P500 futures liquidity at 6 month low) which will be further exasperated by Easter Holiday vacation (April 2nd is Good Friday. Quarter-end is on Wednesday). Remember that on February Month-end, ES1 sold off -60 handles in the last 10 minutes when it was posted -$2.5B for sale. This one has the potential to get much bigger.”

7:45 am

Good Morning!

NDX futures made an overnight high at 12610.00, but pulled back beneath Cycle Bottom resistance at 12563.28. These swings are unusually large, but necessary to allow the volatility to break down supports. Should selling resume at the open, we may see a test of the 200-day Moving Average at 11387.84.

ZeroHedge reports, “Sometime trading really is this easy. Literally minutes after we predicted last night that it was just a matter of time before central banks step in to halt the rout…

… Beijing did just that when shortly after China’s markets reopened on Tuesday (a little after 9pm ET), Bloomberg reported that state-backed funds – i.e., China’s Plunge Protection Team – had intervened to shore up the market in morning trading. The funds, known as China’s “national team,” had stepped in order to ensure stability during the National People’s Congress in Beijing, Bloomberg reported citing “according to people familiar with the matter” with a Hong Kong-based trader saying entities linked to mainland funds were actively buying shares through stock links with Hong Kong Tuesday morning.”

The Shanghai Composite is closed for the day after declining to 3328.21 before closing at 3359.29. I have no explanation for tis anomaly, other than the Chinese PPT had stepped in near or after the close. In any case, it was due for a bounce at or near the mid-Cycle support at 3344.19.

SPX futures rallied to 3865.12, challenging the mid-Cycle resistance at 3859.92, but has slipped back beneath it. Key support is at the 50-day Moving Average at 3819.53. The horrible whipsaw that we have been experiencing may be resolved soon. There is another week of decline ahead of us with bearish implications.

VIX futures are also being whipsawed, but the 50-day support line at 24.04 was not violated. The Cycles Model suggests the next surge in trend strength may occur by this weekend.

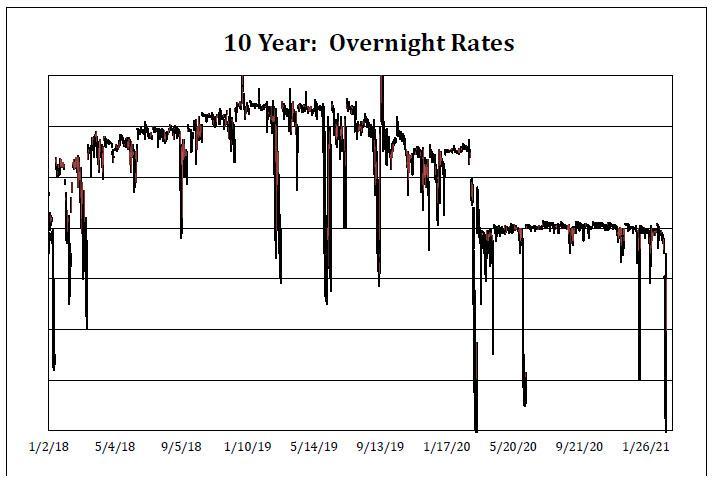

TNX has pulled back from its high, but the surge to a higher price may not be over. The Cycles Model suggests that today and Thursday may show trending strength. Today is day 277 in the Master Cycle, which is unusually long. While the Head & Shoulders target has been exceeded, the Elliott Wave structure calls for yet another surge higher.

ZeroHedge reports, “The Federal Reserve and Jay Powell want to pretend that all is well with the repo market, but nothing could be further from the truth.

Last Thursday, we presented to our readers the latest repo market data showing just how broken and inverted the traditional fund flows surrounding the world’s “most liquid” and important security had become in “Historic Repo Market Insanity: 10Y Treasury Trades At -4% In Repo Ahead Of Monster Short Squeeze.” One day later, the chaos got even worse as discussed in “10Y Treasury Hits A Stunning -4.25% In Repo As Yields Blow Out.” Very simply, this meant that an investor in the repo market lending money so others could short the 10Y would end up paying rather than getting paid. As we explained said “this is a clear breach of one of the most fundamental relationships in the repo market, where lenders of cash always get paid – however little – in order to make a more liquid and efficient market.”

The repo rate sliding far below the “fails charge” of 3.00% which is viewed as the lowest theoretical level where dealers are punished for not delivering a 10Y Treasury i.e., there is a delivery “fail”, was striking but what was even more striking is that the recent repo crunch has been surpassed just once in history: when the 10Y hit a record low repo print of -5.75% during the fear and loathing of the covid crash chaos on 3/13/20, when the Treasury bond market essentially broke down for several hours.”

USD futures pulled back to a low of 91.91 this morning in a consolidation. The Cycles Model shows another week of rally before the USD resumes its decline, enough to cause pain among the short sellers.