3:06 pm

SPX has broken the uptrend from last March’s low. It has retested the trendline and may resume its decline with greater momentum.

ZeroHedge reports, “Just out from Tradestation:

Valued Futures Clients,

Due to potential market volatility, reduced intraday Futures Margin Rates will be suspended at 3:00pm ET.

All Futures accounts will be required to have full maintenance margin when trading futures products by 3pm ET.

Reduced intraday Futures Margin Rates will be available again at 8:00am ET Friday morning.

The last hour of trading is about to get very chaotic.”

ZeroHedge observes, “No hints at a ‘Twist’, refuses to speculate on repo issues, no pushback against recent bond vol, and no mention of SLR exemption.

This was the closest he came to saying anything of note:

“We monitor a broad range of financial conditions and we think that we are a long way from our goals,” he said.

“I would be concerned by disorderly conditions in markets or persistent tightening in financial conditions that threatens the achievement of our goals.”

Which is just more of the same generic platitudes, and that is not what the market wanted to hear…

Nasdaq is now down over 10% from its highs and the S&P has joined Nasdaq in the red for the year…”

7:50 am

Good Morning!

I thought I’d share a long view chart of the SPX that I keep for reference. You may recall that I had mentioned 3950.00 as a possible target in the past month. Here it is in all its glory.

SPX futures dropped to an overnight low of 3778.50 before rising to test the 50-day Moving Average at 3813.79 tis morning. Others see a possible Head & Shoulders formation, but I disagree because the Head & Shoulders is much more rigid in its structure, while the Cup with Handle formation allows anomalies to occur. This is a very bearish formation.

In reviewing the Cycles, I find an alternate to my original thinking that may explain the slow development of the decline. The original Cycle layout called for the Master Cycle to be complete by Friday. That does not appear likely with the bearish formation just being triggered. The alternate calls for the Master Cycle to decline into options expiration week. That would be in agreement with the destructively bearish targets in both the SPX and NDX.

ZeroHedge reports, “U.S. futures slumped alongside tumbling European and Asian stocks on Thursday, but have since rebounded and were back near unchanged levels as traders awaited remarks from Jerome Powell following a recent bout of bond market turmoil. Treasuries and bitcoin were steady, while the dollar and oil were slightly higher. Nasdaq futures rebounded after falling to a two-month low, wiping out all 2021 gains.

At 6:45 a.m. ET, Dow E-minis were down 48 points, or 0.15% and S&P 500 E-minis were down 10 points, or 0.26%. Nasdaq 100 E-minis were down 36points, or 0.29%.

The S&P 500 is set to open below its 50-day moving average, an indicator of short-term momentum that has proved to be a support line in the recent days.

NDX futures dipped to 12513.38 before bouncing back to breakeven. The neckline is near 12700.00 and may be an attractor until it is tested. You can see how much more structured the Head & Shoulders is in the NDX as opposed to the SPX. However, it also simultaneously has a Cup with Handle formation with a much more bearish outcome. It almost seems as if the market is hell-bent to decline no matter what Powell says.

ZeroHedge remarks, “As the NASDAQ took another drubbing on Wednesday, leading many to think that the turmoil of late isn’t just going to go away on its own, all eyes were on the market’s latest “visionary” investor, Cathie Wood at ARK Invest.

Wood has been in the news over the last 12 to 18 months due to the meteoric rise in ARK’s flagship ETFs, including the ARKK Innovation Fund. But of late, even more eyes have been on Wood because questions loom about how Wood’s fund would handle the tech bubble, that has been building in size and speed since March 2020’s Covid lows, if it burst.

And if this week has been any indication, we may find out soon enough.

Heading into Wednesday night, the NASDAQ had turned red on the year.”

VIX futures rose to a high of 27.78 before receding back to the mid-Cycle support at 25.98. The Cycles Model suggests a possible explosion of strength through the weekend. Further strength may occur during options week.

TNX made a low of 14.50 overnight, then began its probe higher. We have a Powell speech this morning and a 10-year treasury auction, to boot. The market may be on tenderhooks until then. A probable targe for today may be 17.00 or higher, depending on the reaction of the crowd. Once the peak is in, the rush to cover may be astonishing.

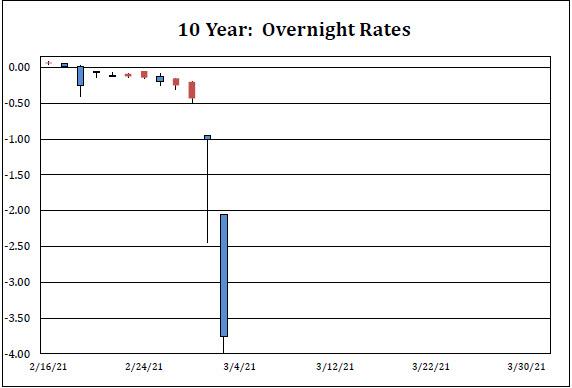

ZeroHedge reports, “Something crazy happened in the repo market today: according to Curvature repo guru Scott Skyrm, the 10Y traded as low as -4.00% in repo, a record low level and an unprecedented dislocation for the world’s most liquid security, one with potentially tremendous consequences for what Jerome Powell may say tomorrow. Incidentally, Skyrm was far more dramatic about this historic move:

It’s all over for the 10 Year Note! Clearly a significant amount of shorts rolled forward and now short-demand has overwhelmed the available supply. The issue traded as low as -4.00% today and already traded at -3.05% for tomorrow. Both of those rates are lower than Fail Charge, which is the equivalent of -3.00%.

What is remarkable is that the 10Y was barely “special” last Thursday when yields exploded higher amid the liquidation panic.

Actually scratch that: last week there were barely any shorts in the 10Y – that’s why the massive stop loss liquidation after last Thursday’s 7Y auction was just longs puking. It was only after that the flood of shorts arrived and hammered the 10Y to “fails” levels in repo.”

ZeroHedge further observes, “One of the biggest buzzwords in finance right now is the three letter acronym SLR, which stands not for a discontinued and particularly expensive Mercedes model, but for Supplemental Liquidity Ratio – a limit on how leveraged US banks can get – and whose fate could mean the difference between a stabilization in the bond market a violent, marketwide crash.

Here’s what’s going on.

Back on April 1, 2020, just as the market was crashing and one week after the Fed unleashed its bazooka to avoid a total systemic collapse, the Fed announces temporary change to its supplementary leverage ratio (SLR) rule “to ease strains in the Treasury market” and “increase banking organizations’ ability to provide credit to households and businesses.” Specifically, the Fed change would exclude U.S. Treasury securities and deposits at Federal Reserve Banks from the calculation of the rule for holding companies. The change would be in effect until March 31, 2021.”

USD futures rose to 91.22 this morning, still consolidating, but ready to move higher.