10:51 am

NDX is approaching its 50-day Moving Average at 13106.17. A cross beneath it would produce a powerful (confirmed) sell signal. The 1987 crash had both a Head & Shoulders and Cup with Handle formations. Both were met in 4.3 days.

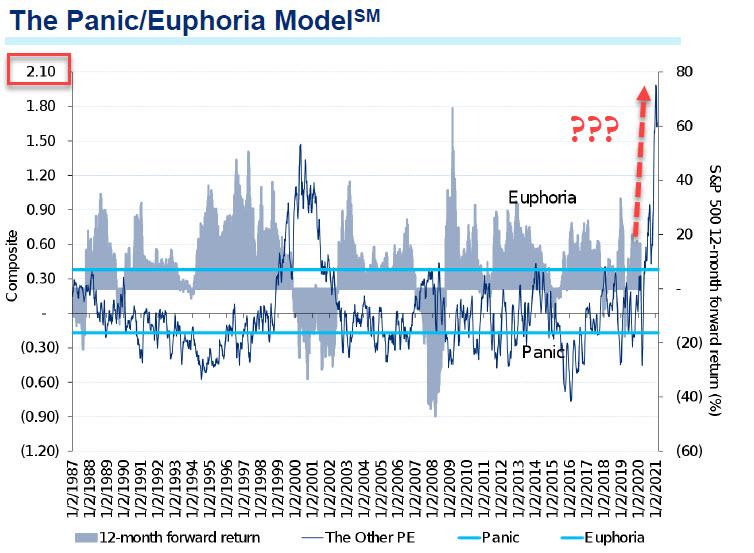

RealInvestmentAdvice observes, “As I worked through this past weekend’s newsletter, I noticed that multiple markets are starting to exhibit topping patterns. It will be crucial for markets to reverse these patterns in the short-term if the bullish advance continues.

As we discussed with our RIAPRO.NET subscribers yesterday:

“The good news is that the S&P 500 held its 50-dma during its recent selloff. With the market getting back to more oversold levels, we are likely to see a counter-trend rally for a few days that could get us back above the 20-dma. It will be necessary for the rally to set new highs to negate the “head and shoulders” pattern. If the market rallies, fails, and breaks the neckline, we could well see a deeper correction ensue.”

10:42 am

SPX has loosed itself from Short-term support at 3896.39 ands is heading for mid-Cycle (intermediate-term) support at3857.01. Options turn bearish beneath that level. This is an aggressive sell for those who have covered. Support at the trendline at 3810.00 and the 50-day Moving Average at 3804.56 may trigger a barrage of selling. Trend strength is starting to build and may peal on Friday.

ZeroHedge remarks, “Back in mid-December, when stocks were melting up furiously daily amid unprecedented retail euphoria, which would only get crazier and crazier until eventually it forced Citi to use a bigger chart two months later to capture the market’s retail euphoria…

… we reported that Bank of America’s first proprietary sell signal since February 2020 was triggered:

According to BofA., equity “barbell” strategies all the rage while (the few remaining) bears note cash levels fall to 4.0%, triggering an FMS Cash Rule “sell signal”; The last time the sell signal was triggered was in February 2020 – everyone knows what happened next.”

9:42 am

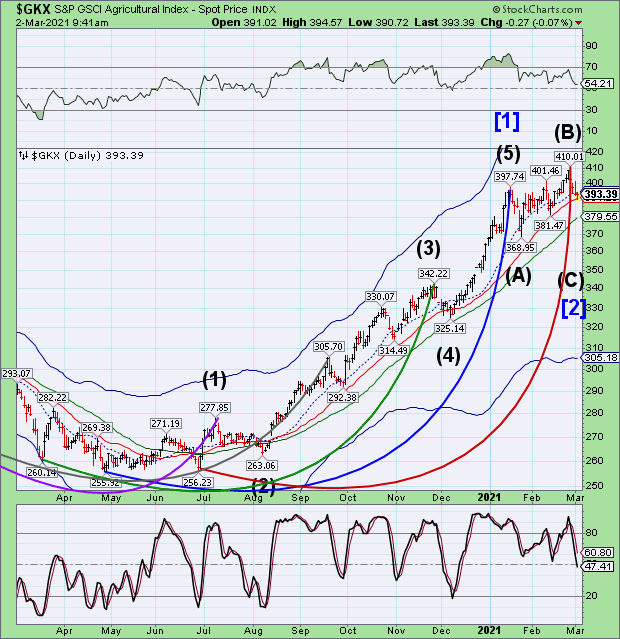

The S&P Ag Index is replacing DBA as there were anomalies in DBA (an ETF) that did not agree with the Index. The Master Cycle (shown in red) may not be complete, and may terminate at the potential low being made in Wave (C). GKX has been on a steady rise since last April with the high at 397.74 being a perfect 8.6 months from the April low. Wave (B) has extended on trending strength, as they are wont in a momentum move. Wave (C) is targeted for the bottom shown at Wave (A). The Current Master Cycle is due to end at the low toward the end of next week.

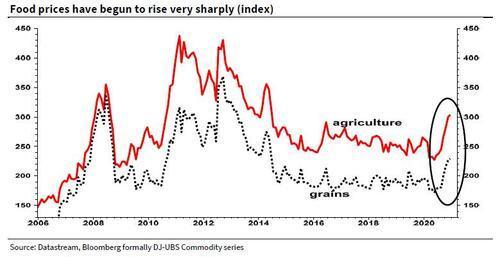

ZeroHedge reports, “Food prices are undeniably soaring faster than inflation and incomes around the world. As everyone’s favorite permabear, SocGen’s Albert Edwards, who, unlike Goldman, has already sounded the alarm on rising food inflation.

As a reminder, the Food and Agriculture Organization’s Food Price Index surged to a seventh consecutive month in December.

With the FAO food index rapidly rising, Edwards noted that “annual inflation in cereals reached 20%, the highest annual rise since mid-2011 when the Arab Spring was in full flow!.”

8:00 am

Good Morning!

As improbable as it seems, what the SPX has demonstrated is a probable expanding Leading Diagonal. The Cup with Handle formation is the dominant formation with a high probability of a massive decline. While there are alternate structures to be considered, the Leading Diagonal is the most bearish and corresponds closely with the structure in the NDX>

SPX futures have weakened, testing Short-term support at 3855.69. Should the Crash scenario be in place, the crash may be starting at the 3:00 pm high. The strongest part of the decline is expected to be on Friday, according to the Cycles Model.

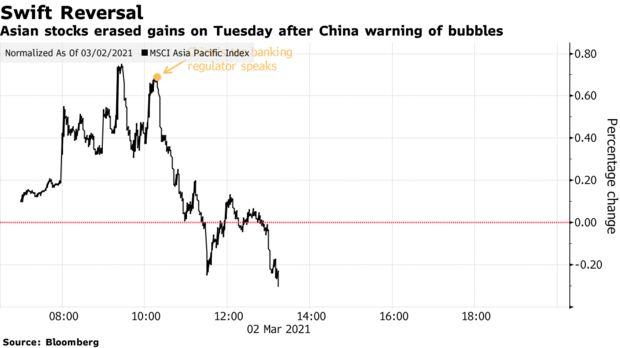

ZeroHedge reports, “Lately not a session seems to pass without some “exciting”, unexpected event forcing momentum to reverse course, and sure enough following the best day for US stocks since June, overnight futures dropped after China’s top banking regulator said he’s “very worried” about risks emerging from bubbles in global financial markets and the nation’s property sector, sparking fresh concerns about further tightening in the world’s second-biggest economy and slamming risk assets.

Asia stocks immediately tumbled on Guo’s comments, with the MSCI Asia Pacific Index erasing earlier gains of as much as 0.8%. The CSI 300 Index in China fell as much as 1.4% and Hong Kong’s main gauge dropped almost 1%….

… while Chinese government bonds gained from a shift toward haven assets, sending yields on benchmark 10-year notes to a nearly three-week low.

US futures also dropped, reversing some of Monday’s gains…

… before recovering much of the loss. In notable premarket moves, Bank of America, Citigroup, JPMorgan, Wells Fargo and Morgan Stanley all dipped between 0.3% and 1.1%. Zoom Video jumped about 10% after the company forecast current-quarter revenue above estimates, as it expects millions of people to continue using its video-conferencing platform. GameStop and other “meme” stocks AMC Entertainment and Koss shed about 1% and 4.4% after a sharp surge on Monday with no apparent news on the shares.

NDX futures slid toward the 50-day Moving Average at 13098.70, but partially recovered. It has formed a perfectly structured Primary Wave [1]-[2] that may have terminated near the top of Wave (4), a normal retracement for a Cycle Wave I of Super Cycle Wave (c).

VIX futures appears to be consolidating within yesterday’s trading range. We look for the VIX to close above its 50-day Moving Average at 23.34 to begin Intermediate Wave (3) of Primary Wave [C]. The probability of matching or exceeding the high of March 2020 is very high.

TNX appears to be steady today, if not slightly higher in the futures. The Cycles Model implies growing strength of trend through early next week. This may be the spark to set off the powder keg in equities.

ZeroHedge observes, “The housing boom unleashed by the Federal Reserve during the pandemic was built on historically low mortgage rates (thanks Powell), low inventory, city-dwellers moving to rural areas, and remote-work phenomenon. In all, housing prices in 20 U.S. cities surged in December at the fastest pace since 2014 as mortgage rates fell to record lows. But a new rate regime is in town, one where bond traders are pricing in inflation as they believe the vaccine rollout and stimulus will lead to a sizzling economic recovery, one that could force the Fed to hike rates earlier (and more aggressively) than expected…

…all of which has resulted in the latest treasury and mortgage bond rout.

If you called up your mortgage lender last week for a 30-year fixed loan, the rate was around 2.81% – this week, the rate jumped to 3.06% on Friday, the highest since August. Rates have been increasing since hitting a record low of 2.65% in early January.”

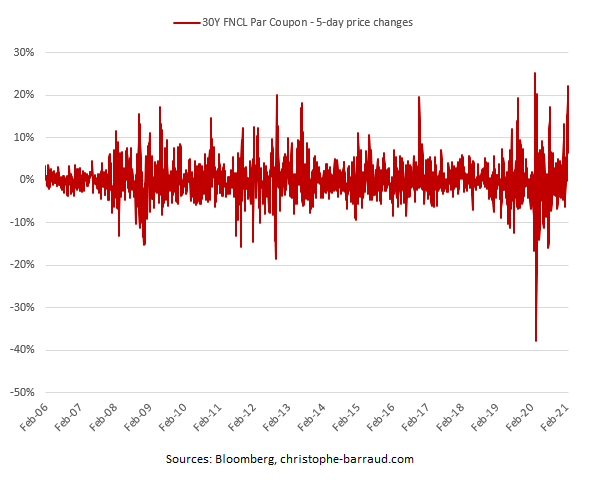

This morning ZeroHedge further comments, “U.S. 30-year mortgage rates have rebounded sharply since two weeks with the 30-year treasury yields spiking above 2.25% on Thursday (highest since January 2020). The recent shock to the Fannie Mae 30-year mortgage — used as a benchmark for U.S. home loans — was meaningful. On a 5-day basis, outside of one time during the Covid crisis last spring, it was the biggest percentage rise in mortgage rates on record.

Despite the latest report from Freddie Mac suggests that 30-year mortgage rates were still at 2.97% (highest since August 2020), it seems that reality is a bit different.”

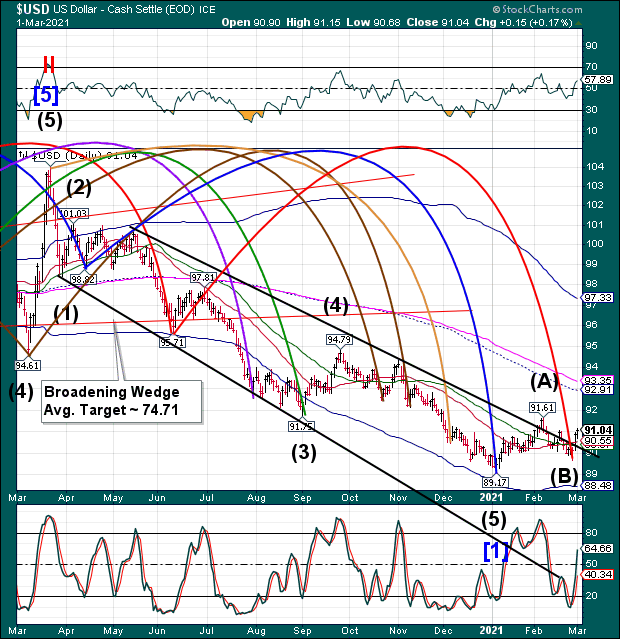

USD futures hit a new high at 91.39, pushed higher by the specter of rising rates. Last Thursday’s Master Cycle low at 89.68 now appears to be locked in, with the USD rising through mid-April. The rising USD has not reached recognition status yet. A breakout above the previous high at 91.61 may finally gain the recognition the rising dollar deserves along with the increasing pain leading to short covering.

Gold futures have bounced off the Cycle Bottom support at 1720.00 to 1734.35 in overnight trading. However, the decline is not due to end until the week following options and futures expiration. This move is the biggest argument against a new super Cycle bull market in commodities. The other commodities may soon follow.