8:00 am

Good Morning!

SPX futures have challenged the mid-Cycle (Intermediate-term) resistance at 3852.74 this morning. This bounce may be Minute Wave (c) of Minor Wave 2. The 50% Fibonacci retracement of Wave 1 is at 3859.09. The 61.8% Fib retracement is at 3875.51. Should this bounce meet or exceed Friday’s retracement high at 3861.08, the countdown for the crash scenario starts here. As mentioned last week, a crash scenario takes at least 4.3 days. The trigger for that scenario appears to be the Lip of the Cup with Handle formation.

ZeroHedge reports, “After last week’s global bond rout, central banks weren’t taking any chances, and as soon as the overnight session started yields plunged first in Australia and then everywhere else after the RBA doubled the amount of daily QE to enforces its YCC, sending 10Y Australian bond yields plunging by as much as 32bps, the biggest drop since last March. Other joined in verbally, with the ECB saying said it will not tolerate higher yields even though the Fed has for now said it sees little cause for concern in the rapid run up (BofA disagrees and expects Powell to calm markets as soon as this week). Meanwhile, a barrage of sellside reports over the weekend, sought to reassure investors about the risk of a breakout in inflation, with the likes of JPM and Goldman all saying that fears of a rapid increase in consumer prices are overblown (although in case they aren’t, Goldman conveniently provided a list of companies that will be hammered if yields continue to rise).

In any case, S&P500 futures jumped more than 1% on Monday thanks to the stabilization in bond yields and as Johnson & Johnson’s newly approved COVID-19 vaccine and progress in a new $1.9 trillion coronavirus relief package fueled optimism over a swift economic recovery. At 07:30 a.m. ET, Dow E-minis were up 297 points, or 0.954% and S&P 500 E-minis were up 40.00 points, or 1.05%. Nasdaq 100 E-minis were up 167.50 points, or 1.29%

The risk advance was broad, with stocks tied to economic reopenings and faster growth notching some of the biggest gains. Futures on the small-cap Russell 2000 Index outperformed the Nasdaq 100 Index.”

NDX futures are coming off a high of 13132.38 this morning and have fallen beneath the 50-day Moving Average. Don’t let this bounce fool you. The only support left is the neckline/Lip of the Cup with Handle formation with dire consequences when the NDX declines beneath them.

ZeroHedge observes, “In today’s equity update we are following up on our analysis of the Tesla-Bitcoin-Ark risk cluster showing an updated positions analysis, cross-correlations in the flagship Ark Innovation ETF, and an drawdown analysis. Yesterday, was another bad session for this risk cluster and Ark Invest had a day with outflows across all their ETFs highlighting that risk sentiment has changed. With the founder’s bold move to increase the position in Tesla during the week the risk has gone up that this risk cluster could turn into an ugly forced selling dynamic causing pain in not only Tesla, Bitcoin, and Ark funds, but also US biotechnology stocks where Ark Invest is a major holder with high ownership in selected names.

A little over a month ago we first flagged the Tesla-Bitcoin-Ark risk cluster as something to take note off as short-term correlation between Tesla and Bitcoin was shooting up. A survey from Charles Schwab also confirmed our suspicion that there is a big overlap as these two instruments are among the top five holdings by millennials. Our analysis quickly led us to Ark Invest with its famous Ark Innovation ETF which had a big position in Tesla and its charismatic founder Cathie Wood is a big believer in the so-called disruptive innovation culture of Silicon Valley. This class of people believe firmly in technology as mainly good for society in all its aspects and that Bitcoin is a protection against future wealth confiscation which is most likely inevitable due to historically high wealth inequality.”

VIX futures made an overnight low of 24.74, making a 58% retracement of its Wave (1) off the Master Cycle low. his would be expected, as Intermediate Wave (3) of Primary Wave [C] of Cycle Wave III portends a crash may be developing. Cycle trending strength appears to be highest on Friday, which supports the 4.3-day crash scenario starting today.

TNX is lower this morning, but while today is day 269 in the Master Cycle (suggesting last week’s high may have been the top), the Wave structure may be deficient, leaving room for another probe higher this week. The outside limits of the Master Cycle is plus or minus 17.2 days (241 to 275). There are multiple reasons for this:

- The first is that, contrary to my expectation of a 10-year Treasury auction last week, the next scheduled auction is on March 4. Remember, last week’s 7-year auction was a disaster, causing the rate spike on Thursday.

- The FOMC meets this week, leaving a news blackout until Wednesday.

- CTAs and hedge funds are still liquidating their bonds while foreign investors have been staying away.

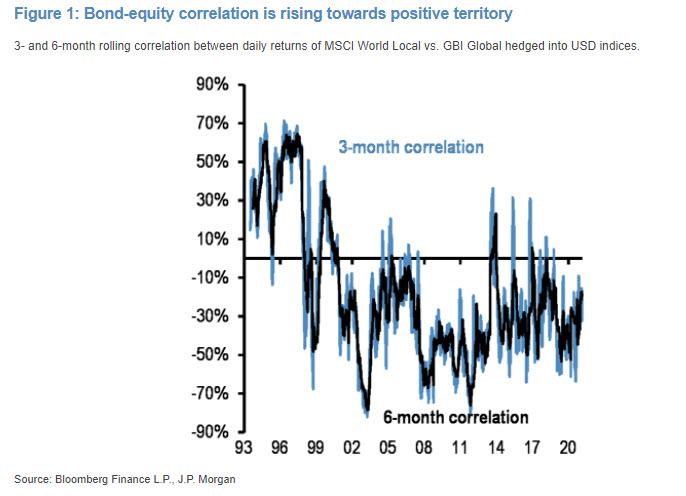

ZeroHedge observes, “It was just last Tuesday when he presented our readers with the latest observations from JPM quant Nicholas Panaigrtzoglou, who warned that the rapid rise in bond-equity correlations…

… was bringing memories of previous violent bond tantrum episodes, including Bernanke’s famous Taper Tantrum from May-June 2013, the Bill Gross-inspired Bund tantrum of May-June 2015, the period into the US election Oct-Nov 2016, Feb 2018 and Q4 2018. All of those ended with pain for both bond and equity longs, and certainly risk parity and 60/40 balanced funds who were crushed on both long legs.

Well, just two days later this warning was realized as we saw a surge in bond volatility as global bond prices plunged and yields soared as the latest inflation scare finally came to the fore (catalyzed by the catastrophic 7Y auction which sparked massive liquidation volumes across the curve).”

USD futures have hit a new high from its Master Cycle low at 89.68. Most investors are apparently ignoring this move and may not recognize a (short-term) change in trend until the USD rises above 91.61. The Cycles Model suggests the rally may extend until mid-April. Thus, the normal target at mid-Cycle resistance at 92.94 may be exceeded. A possibility may be a rally to the Cycle Top resistance, currently at 97.39.

After a brief rebound from Friday’s surprise reversal, WTI futures have turned back down. The decline should be no surprise, as Friday was day 256 in the Master Cycle. The Cycles Model indicates that, should the decline get underway, we may see it continue up to six weeks through early April. After weeks of declarations of a new Super Cycle bull market in oil, the hedgies and CTSs are jumping in with both feet.

ZeroHedge remarks, “Two weeks ago when the world was still transfixed by the rolling squeezes of the most shorted stocks triggered by the WallStreetBets subreddit, we reported that JPMorgan said to ignore the spectacle du jour in the illiquid, left-for-dead smallcaps, and instead focus on what was coming: a coming massive, marketwide squeeze as quant, momentum and other systematic investors soon start covering what is a historic short across the energy sector. Importantly, JPM also gave us the timing of said squeeze: early March.

Fast forward to today when various funds have naturally frontrun what is expected to be a massive market move. Yes, the systematic short squeeze that JPM’s Kolanovic wrote about two weeks ago, has started and as Rabobank’s Ryan Fitzmaurice wrote, “the one-year rolling momentum signal for Brent flipped from bearish to bullish this week, effectively leaving systematic traders “all-in” with respect to their directional oil market bias.”