7:30 am

I will be out most of the day, so I have given as comprehensive account as I can for what may transpire. Be prepared!

Good Morning!

NDX futures are flat this morning after having bounced off the Head & Shoulders neckline. The probability of a crash scenario is very high, and becomes certain once the NDX declines beneath 12750.00. So let’s review what the Cycles may offer us.

First, a crash takes a minimum of 4.3 days. The time would be measured from the top of Wave 2 at 13312.40, so one day has elapsed thus far. That gives a minimum time to the bottom at Wednesday morning. However, the decline and correction from the top at 13879.80 took exactly 6.45 days, (1.5 Cycles). That suggests a possible 6.45 day decline from the top of Wave 2, indicating a possible bottom at mid-day on Friday. We will have to monitor the situation as it develops.

SPX futures also remain flat. SPX has not (yet) crossed the 50-day Moving Average at 3798.76. It also must decline beneath the massive Orthodox Broadening Top trendline.at 3750.00. Once accomplished, point 6 awaits at 2100.00. Should the Broadening formation be valid, that target appears to be the minimum for this move.

ZeroHedge reports, “Global bond yields slid on Friday following Thursday’s epic meltdown as markets returned to firmer footing at the end of a week that saw the biggest decline in the Nasdaq 100 since the pandemic meltdown. Meanwhile, the quant who predicted this week’s meltdown in both bonds and stocks, turned bullish overnight (more in a separate post) a further indication the liquidation may be ending.

US futures found support around 3,800 and have since rebounded, as global markets stabilized after central banks from Asia to Europe moved to calm a panic that had sent US government bond yields to their highest level in a year and triggered a loss of almost $900 billion in the value of the tech-heavy Nasdaq, the biggest since March.

Contracts on the Nasdaq 100 and S&P 500 fluctuated before turning modestly higher. Thursday’s rout in yields which sent the 10Y as high as 1.61% after a catastrophic 7Y auction, has reversed with broad-based buying across the curve, especially after central bankers stepped in with the usual jawboning to convince markets of their commitment to Yield Curve Control (as the alternative is simply unthinkable). The scale of the sell-off prompted Australia’s central bank to launch a surprise bond buying operation to try and staunch the bleeding. The ECB is monitoring the recent surge in government bond borrowing costs but will not try to control the yield curve, ECB chief economist Philip Lane told a Spanish newspaper.”

VIX futures are lower, but remained above the mid-Cycle support at 25.98. There is no formation that gives a target, other than the prior high from last March. Past experience would suggest the top of Wave (1) may terminate near 85.00.

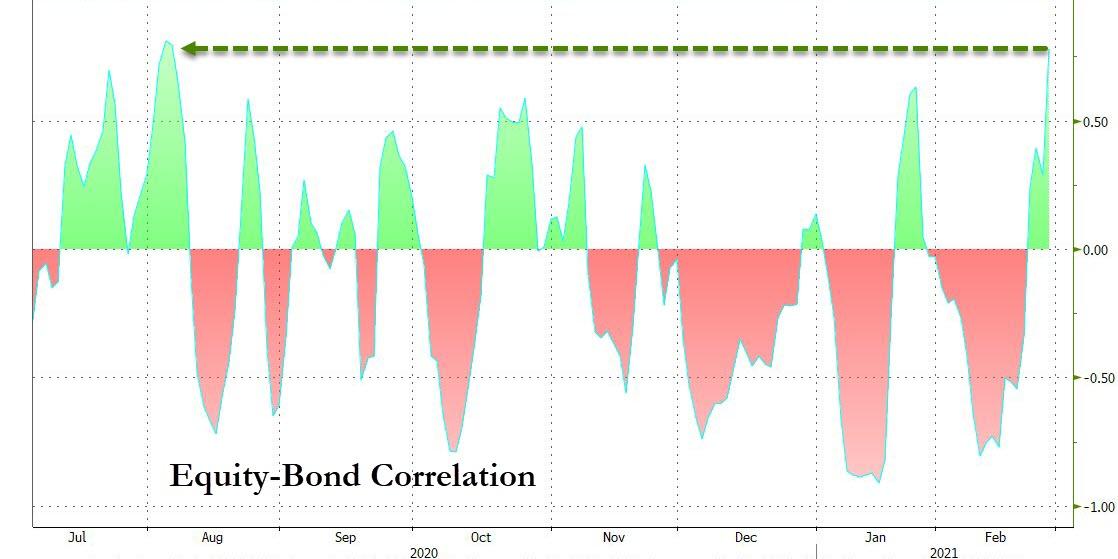

ZeroHedge observes, “Following a series of warnings that risk parity funds may be on the verge of capitulation and deleveraging into the maelstrom of tumbling stocks and bonds…

… yesterday it was JPMorgan’s turn to join the chorus of warnings that the continued selloff in rates, coupled with the accelerating drop in tech/growth stocks would result in very unpleasant consequences for both risk parity and conventional 60/40 balanced funds.

In his report, JPM quant Nick Panigritzoglou looked that the recent surge in the bond-equity correlation (which is usually negative and “helps to contain the volatility of risk parity funds and balanced mutual funds”)…

… which he wrote was “raising concerns about de-risking by multi-asset investors, such as risk parity funds and balanced mutual funds.”

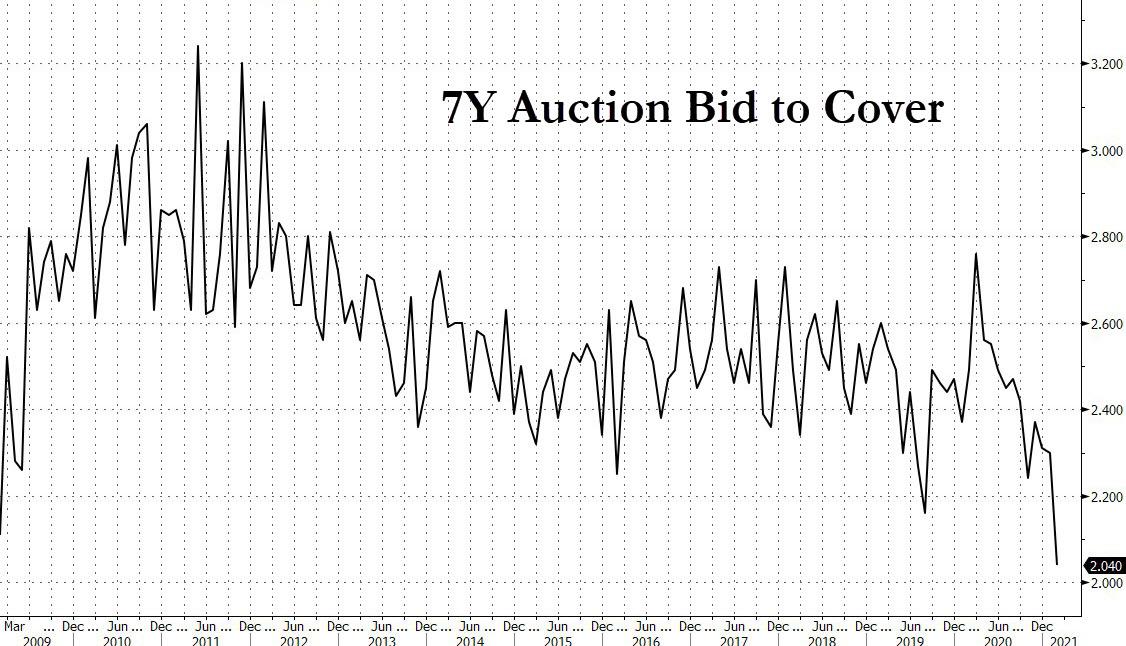

TNX futures are also flat, giving an eerie sense of calm to the markets. However, it is not yet time to breathe easy. I have marked yesterday’s high as the top of the current Master Cycle. However, today the 10-year treasury auction is being held. After yesterday’s disastrous 7-year treasury auction, things don’t look good for today’s outcome.

ZeroHedge reports, “This is as close to a failed auction as we have ever come…

Ahead of today’s closely watched 7Y treasury auction, where the bulk of the recent Treasury rout has been concentrated as traders hammered the belly of the curve, we said that “If the 7Y tails a lot, watch out below” as that would only add insult to today’s furious selloff injury. Well, that’s precisely what happened, because with the 7Y pricing at 1.195%, this was a whopping 4.1bps tail to the 1.151% When Issued.

If the 7Y tails a lot, watch out below

— zerohedge (@zerohedge) February 25, 2021

The auction was, in a word, catastrophic.

Starting at the top, the bid to cover tumbled from 2.305 to 2.045, the lowest on record, and far, far below the 2.35 recent average.

But if that was ugly, the internals were even worse, with the Indirects plunging from 64.10% to just 38.06%, the lowest since 2014, as no foreigner suddenly wants to even smell US debt!”